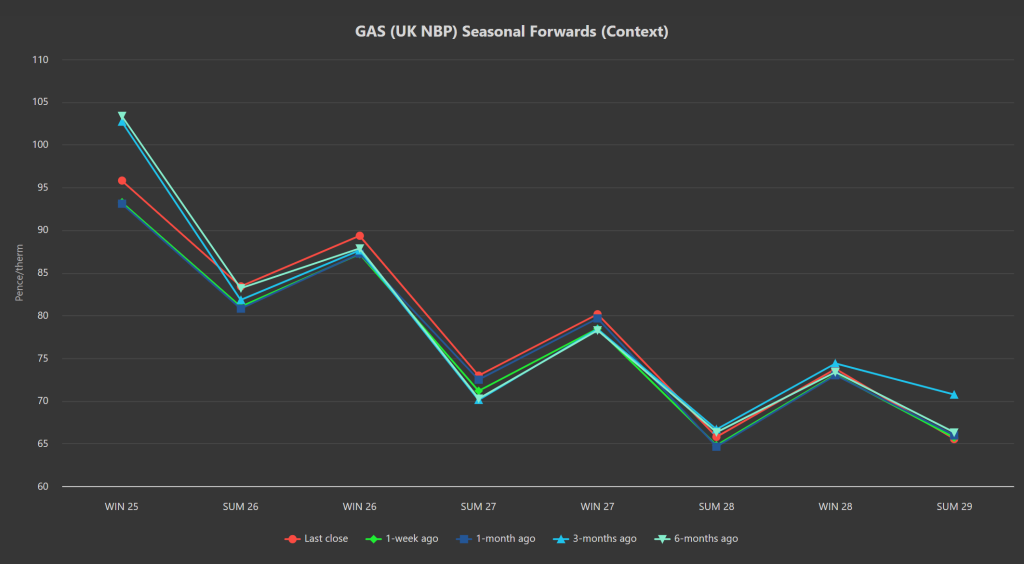

Seasonal Forwards have been trading in a tight range since early April-25 (the onset of Summer-25).

Winter-25 delivery fell below 100p/therm on 4th Apr ’25 – thereafter, prices have traded within a 10% range.

As the chart below further illustrates, Seasonal Forwards have operated within a 10% range as far back as 6-months ago.

As such, it’s fair to assert that prices have found an equilibrium – supported by geopolitical and associated supply risks; pressured by benign weather conditions and a quiet optimism amongst market participants that storage replenishment (in time for the winter heating season) is on track.

So, from a buyer’s POV, why is it that markets remain backwardated? i.e., periods of delivery further down the curve are at a discount to periods of delivery in the nearer term?

Well, market participants evidently believe that prices are set to fall as the years unfold.

But how can that be (given markets still seem so unsettled)?

In short, it all comes down to good old-fashioned supply/demand dynamics.

If we look back to the start of 2025, weakness in Chinese LNG demand coupled with Plaquemines LNG in the US coming online significantly calmed the supply outlook for Europe/the UK.

Nonetheless, with all known variables considered, it looks likely we’ll only just manage to replenish European stocks to the required level in time for Winter-25 – so that very narrow margin for error is propping up front-season prices.

Not to mention all the potential banana-skins that lie in wait for us in the coming months – US hurricanes, liquefaction outages, Norwegian maintenance drifts, heatwaves and the associated cooling demand rush for LNG arrivals across Asia.

In addition, the possibility of the resumption of Russian flows into Europe now looks dead in the water (both LNG and pipeline) – amid fading hopes for a quick peace deal in Ukraine and Europe’s determination to step-up sanctions against Russian energy.

However, when we look a little further out, global LNG outputs are forecast to double throughout 2026 (made possible by capacity additions from the US, Qatar, Canada, Western Africa and Mexico) – this will drive an increase in European/UK LNG imports (further mitigating winter storage risks).

As such, cumulative volumes from new LNG projects look likely to tip the global gas market into a glut/oversupply come 2028/2029 – notwithstanding further disruptive golbal conflict between now and then.

Given the solid comparative value being offered for delivery further down the curve (beginning Summer-27), buyers are encouraged to scale-in Forward hedges so as to build a budget of secured step-down prices y-o-y.

Back to this week (and short-term risk), Norwegian outages (both scheduled and unscheduled) will feature in the coming days forcing significant pipeline volumes offline (tightening supply, adding price support).

Though bullish fervour should be tempered by an improving weather outlook with Europe as a whole enjoying temperatures well above seasonal norms before the weekend.

European storage fullness continues to resemble 2022’s trend – currently at 51% versus the 5-year average of 58%.

The consensus amongst analysts now expects storage to achieve around 87% by the time Winter-25 kicks-in (hopefully making it more difficult for the alarmists to spike the market higher for no discernible reason over the coming months).

This morning, markets are softer than Friday’s closing prices off the back of a long system (supply outstripping demand forecast).

On the trading side, clients running flexible capability are increasingly picking up significant volumes of the attractive Forward Summer prices currently on offer.

It would seem prudent for buyers to continue to scale-in modest hedges over the coming days/weeks whilst the going is good.

This month’s UK gas Day-Ahead averages are holding steady at 84p/therm (or approx. 2.9p/kwh excluding non-gas).

ELECTRICITY & CARBON

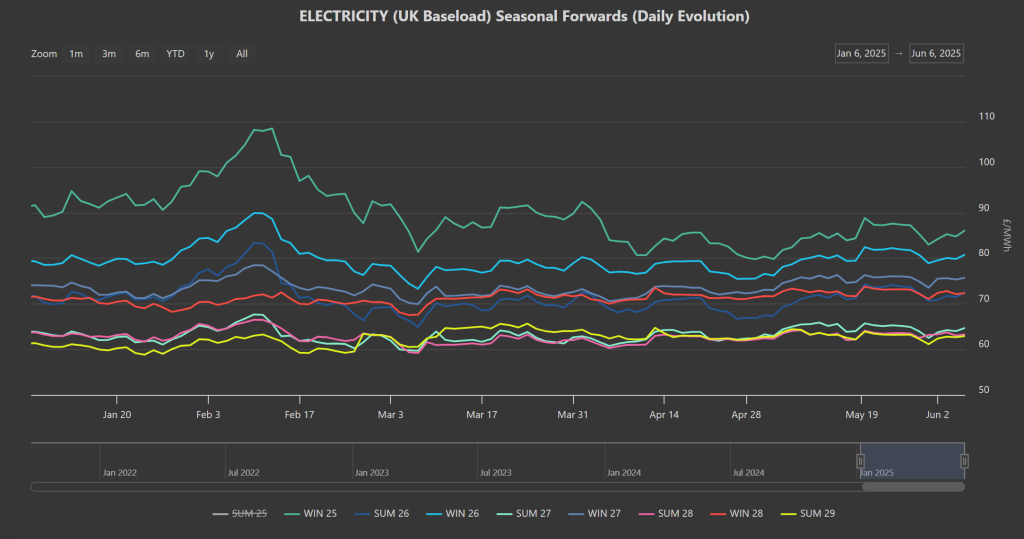

Electricity prices remain closely correlated to gas movements – so, in the main, it’s sideways price action.

Further to the falls in price seen in Feb/Mar ’25, Seasonal Forwards are trading in a tight consolidation (please see chart below).

Today’s public holiday in the majority of EU states is likely to mean illiquid trading conditions (and so not a good day to hedge given the risk of wider bid/offer spreads).

On the Carbon side of things, markets are flat and consolidating in a tight range just above £50/tn on the mid-price.

Today’s UK electricity generation mix is nutral to bearish in nature reflecting essentially benign weather conditions – specifically, renewables are contributing 34%, thermal at 25% (gas and coal) and low carbon at 22% (nuclear and imports).

So far this month, electricity Day-Ahead averages are low and reflect summer-demand – currently at £62/mwh (or approx. 6.2p/kwh excluding non-energy).

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst markets still offer solid comparative value.