Whilst prices looked to be stabalising on Friday amid tighter spreads (suggesting decreasing volatility), I’m afraid the weekend’s events have (again) meant a Monday spike to near-term delivery pricing – please see Saesonal Forward chart below.

Most notably, Iran’s establishment has named Ayatollah Ali Khamenei’s son, Mojtaba Khamenei, as the country’s new supreme leader.

The appointment has inevitably added a new layer of tension to the conflict in the Middle East – Trump had previously indicated that Mojtaba Khamenei was the most likely successor but warned he would consider such a choice “unacceptable.”

Speaking earlier on Sunday, Trump said Iran’s next supreme leader “was not going to last long” without US approval – then later in an interview with the Times of Israel, he added that the decision on when the war might end would ultimately be made together with Israel’s Netanyahu.

All of which has sent the near-term delivery markets this morning to levels not seen since Winter-22.

Despite otherwise bearish fundamentals with Summer-26 now only a few weeks away, developments across the Middle East will continue to dominate price action this week.

In other impactful news, attacks on Iran’s neigbour’s energy infrastructure have begun once more, and Trump has made clear that he’s weighing deployment of ground forces – all of which points to geopolitical interference in the energy markets with no end in sight.

In short, whilst Trump’s ill-defined campaign in Iran escalates (conveniently diverting attention away from the Epstein files, some might say), standard fundamental drivers have become irrelevant.

As of this morning, we’ve entered another full-blown energy crisis which could very easily spin out of control and take markets back to the dark days of the heights of Winter-22 – unless the US takes steps soon to de-escalate.

On the strategy side of things, gas FLEX clients are being encouraged to build modest positions further down the curve where steady prices persist (given that far term delivery prices are as much as 45% below those of near-term delivery).

ELECTRICITY & CARBON

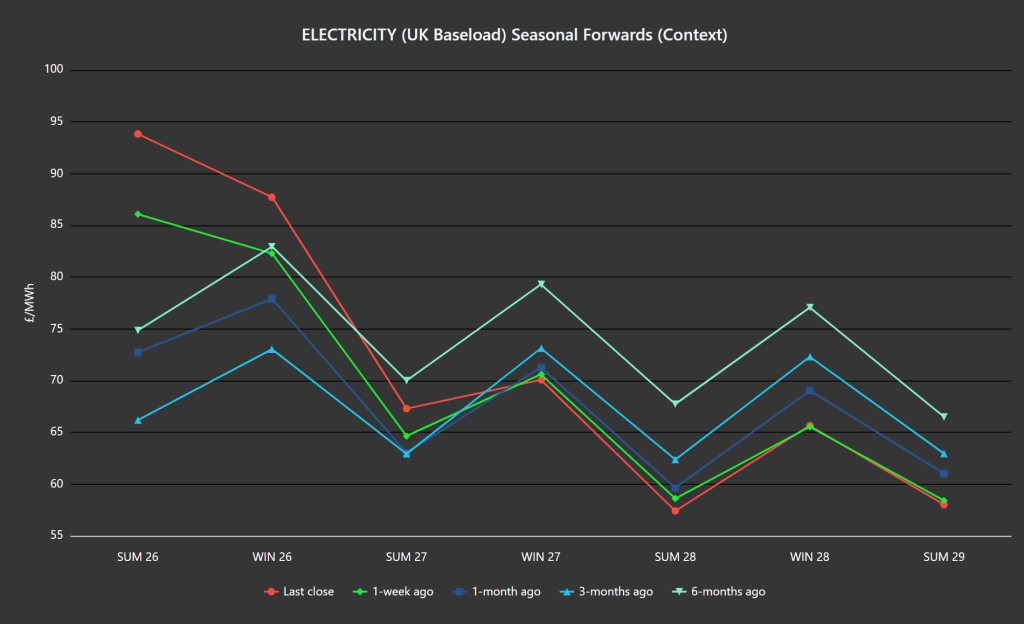

As per the chart below, all the pain is being felt at the front-end.

At the time of writing, looking at very volatile intraday prices, Summer-26 delivery has spiked by 42% since mid-Feb.

Conversely, on the Carbon side of things, Dec-26 UKA delivery has fallen to £39.33/tn this morning, amid fears that Trump’s war on Iran will slow global economies (and Industrial outputs).

Today’s UK electricity generation mix is bullish in nature, but hardly worth reporting on.

The only driver of price this morning is the worsening situation across the Middle East, with Ukraine suggesting over the airwaves that the Iran conflict is in fact no more than extension of Ukraine’s problems (and that Russia and Iran are working to destablise the West together).

On the strategy side of things, electricity FLEX clients are being encouraged to build modest positions further down the curve where steady prices persist (given that far term delivery prices are as much as 35% below those of near-term delivery).