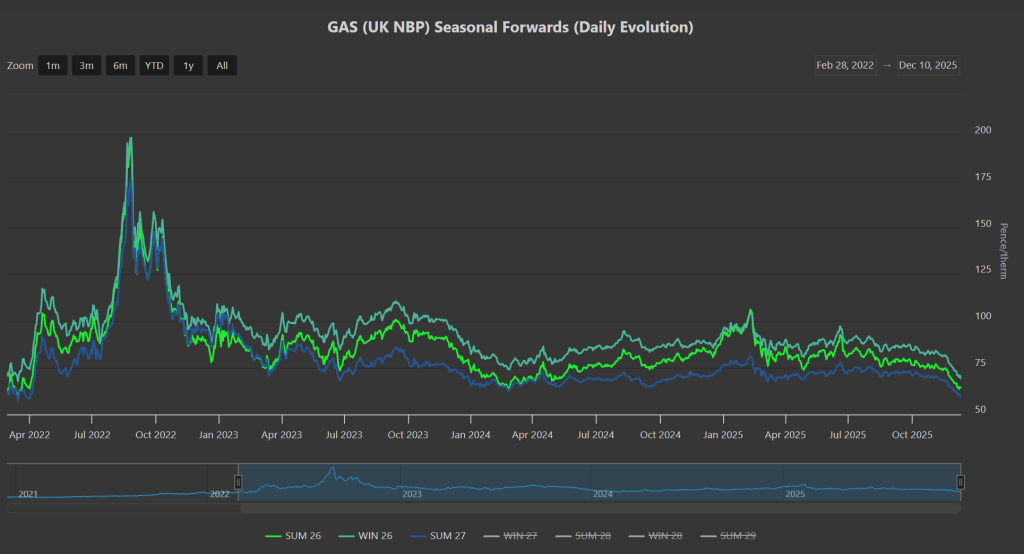

Notably, delivery prices for the front 3-Seasons (Summer-27/Winter-27/Summer-28) have drifted to levels not seen since March ’22 (please see ‘Daily Evolution’ chart below).

This despite, LNG gas imports into North West Europe having decreased month-on-month.

Whilst heating demand is down off the back of unseasonably mild temperatures, Europe/the UK still need to draw consistent fuel flows, which is keeping the market from falling through the floor.

The market’s bearish underlying sentiment is seemingly shrugging off any fears of supply tightness despite forecasts of falling wind outputs into next week.

Whilst UK LNG imports/send-out feels a bit sluggish compared to European activity, we’ve nonetheless seen a redirection of Norwegian flows (with Franpipe having been re-routed through Vesterled).

The combination of strong Norwegian pipeline flows versus lower wind (contributing to higher gas-for-power burn) signals that UK prices will likely remain neutral to bearish over the coming sessions.

European net gas storage withdrawals are incrementally increasing with the very gradual onset of winter conditioning – today, European inventories are at 72% versus the 5-year average of 86%.

Traders continue to eye the bearish impact of the return of Russian gas flows if/when peace talks bring about an end to Russian sanctions.

Monthly Day-Ahead averages for December so far have fallen to 69p/therm (or 2.35p/kwh exc. non-gas).

ELECTRICITY & CARBON

Notably, Seasonal delivery prices all the way down the curve are lower versus 1-week/1-month/3-months/6-months ago (please see ‘Context’ chart below).

On the Carbon side of things, UKAs went as low as £55.10 yesterday on the mid-price – their lowest level since late-Oct ’25.

Rumours abound amongst Carbon traders that the EUA/UKA linkage talks are not going as well as hoped (a bearish driver for UKAs).

Today’s UK electricity generation mix is neutral in nature, neither bullish not bearish – specifically, renewables are contributing 39%, thermal at 30% (gas and coal) and low carbon at 16% (nuclear and imports).

Monthly Day-Ahead averages for December so far have fallen to £73/mwh (or 7.3p/kwh exc. non-energy).