Geopolitical developments over the last few days coupled with lower temperatures across the UK/Europe have meant both near- and far-term delivery contracts have recovered some of last weeks losses.

At yesterday’s meeting in Saudi Arabia, the US agreed to resume security support for Ukraine (in return for Kyiv confirming a willingness to accept a ceasefire proposal).

Unfortunately, Russia’s response today has been to criticise the offer, stating it would give Ukrainian forces a reprieve (just when Putin feels his forces are close to regaining Kursk).

On the Trump tariff side of things, the EU has responded to to the imposition of 25% tariffs (on European steel and aluminium) with €26bn of ‘countermeasures’ including on such US favourites as bourbon, jeans, and Harley-Davidson motorbikes.

Thankfully, Europe is not threatening to impose tariffs on imports of US LNG…

Despite the cold spell, the UK system opened long this morning (supply outstripping demand forecast).

Nonetheless, heating demand and gas-for-power burn is rising d-o-d in line with temperatures falling.

On the supply side, Norwegian flows are on the up following Asgard coming back online.

Withdrawals are ongoing despite very solid LNG send-out – reflecting high demand, poor renewable outputs.

European storage is at 40% versus the 6-year average of 49%.

Rumours abound that a resumption of the Ukrainian gas transit agreement is still in the offing (assuming Putin comes to the table over the ceasefire).

It seems unthinkable that Putin will resist Trump’s efforts to broker a peace deal in the long-term – otherwise, Trump will be left with egg on his face and Putin’s opportunity to exit the mess (that is the Ukraine invasion) will have passed him by.

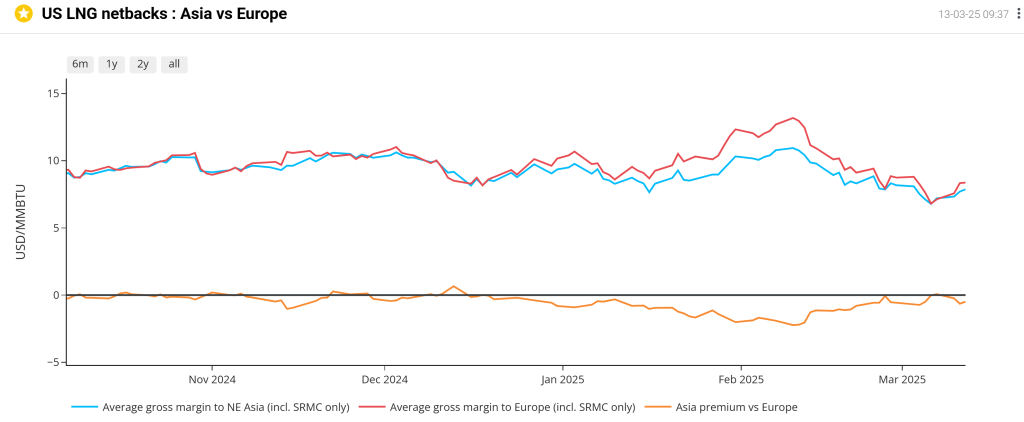

For US LNG cargoes at least, Europe retains its attractiveness over Asia – please see chart below.

Monthly Day-Ahead averages for this month so far are on track to improve on last month’s final number (124p/therm), with averages at 103p/therm at the time of writing (or approx. 3.5p/kwh excluding non-gas).

ELECTRICITY & CARBON

Mirroring gas prices, Seasonal Forwards have risen at the front of the curve, but are relatively unchanged beyond Winter-26.

On the Carbon markets, prices remain range-bound, caught between geopolitical uncertainties (Trump’s tariffs and Ukraine) — whilst the recent declines (and improved value) may start attracting compliance buyers (driving the market up).

Nonetheless, speculators still hold a significant long (buy) position, in the belief of course that Carbon MUST rise in the long term if global sustainability goals are to be met.

Looking at UK mandatory Carbon allowances for heavy emitters (UKAs), the Dec-25 benchmark has rejected upside resistance at £44/tn – please see chart below.

A new bullish trend channel is forming, and if resistance at £44/tn holds, a retest of the lower extremity of the bullish trend channel (at £40/tn) looks likely.

UK electricity Monthly Day-Ahead averages so far for this month are back below £100/mwh and sliding – now at £93/mwh (or approx. 9.3p/kwh excluding non-energy).