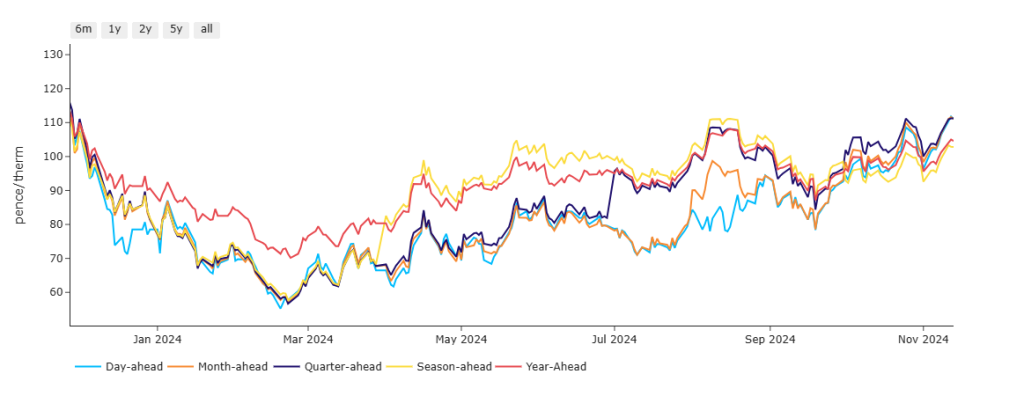

For the first time since Dec ’23, Day-Ahead is topping the Prompt – at parity with Month-Quarter Ahead (please see chart below).

Of course, Day-Ahead being so elevated reflects the increasingly wintry risk-premium being assigned by market participants to very near-term delivery.

Notably, contracts all the way down the curve opened up this morning, with the front month at the highest level since this time last year.

Supportive drivers include concerns over the remaining vestiges of Russian flows into Europe after OMV (an Austrian energy company) was awarded around €230 million by the ICC for “irregular” German gas delivery.

The upshot will likely be a worsening of the contractual relationship resulting in a reduction and/or suspension of Russian exports.

In more bullish news, SPP (the Slovakian gas buyer) has said that whilst it supports the continuation of flows from Russia through Ukraine, it is nonetheless resorting to contingency measures to ensure supply – heightening competition amongst buyers for supply.

The UK is forecast for a cold spell in the coming weeks, with temperatures set to fall 6/7°C below seasonal norms between 20th to 25th Nov.

European storage is now down to 93% (versus the 5-year average of 89%) off the back of increased withdrawal.

As such, LNG arrivals to Europe are more frequent with the JKM spread favouring Europe over Asia.

To counter the growing protectionist storm brewing in the US now that Trump is President Elect, China is ploughing cash into new underground gas storage facilities and LNG terminals – with storage capacity expected to double by the end of the decade.

UK prices will likely remain at a premium versus Europe’s as the winter progresses – otherwise, we’ll be left high and dry where LNG arrivals are concerned!

This premium is always exacerbated by structural problems in the UK’s gas system resulting in high transmission costs and, of course, a lack of storage compared to Europe – meaning the UK needs to offer a much higher price to secure supply.

Monthly Day-Ahead averages so far this month are on target to achieve 104.833p/therm (or approx. 3.577p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, next week is forecast for cold weather.

On the Carbon markets, the Dec ’24 EUA benchmark opened yesterday at €67.12/tn before trading in a €66-67/tn range until the publication of the COT (Commitment of Traders Report) showing that speculators have reduced even further their net short positions.

UKAs have mirrored EUAs’ sideways price action, and have still yet to retest the lows of 8th Oct – currently sitting at £38.12/tn on the mid-price (please see chart below).

Our electricity generation mix is bullish in nature today with renewables contributing 1%, thermal at 54% (gas and coal) and low carbon at 22% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £102.792/mwh (or 10.28p/kwh excluding non-energy).