Markets are holding on to yesterday’s losses amid an uneasy hiatus in the conflict.

Prices have steadied this morning, with front-month GAS just above the psychological level of 100p/therm, and ELECTRICITY well-below the pyschological level of £100/mwh (reflecting the fact that GAS is carrying the weight of the risk-premium).

Rumours abound that the US and Iran are expected to extend the ceasefire by a fortnight with a view to further negotiations.

Nonetheless, Israel’s offensive in Lebanon persists, and the Strait of Hormuz (noise aside) is still closed to LNG cargoes.

Strangely, a number of vessels appear to have broken through the US blockade to reach Iranian ports – though none are then leaving.

Iran’s bargaining power would seem greater than the US is prepared to let-on – not only are they successfully weaponising the Strait of Hormuz, but their brothers-in-arms (the Houthi rebels), are also poised to block the Saudi’s oil cargoes transiting via the Bab el-Mandeb Strait on the Red Sea.

Were this waterway also to become a risky passage, ships would be forced to re-route via The Cape of Good Hope (a 2-week detour).

In unrelated macroeconomic news, China’s GDP growth was back over 5% for Q126 – in less tumultuous times, this would have been big news.

But another reason why Europe/the UK’s gas prices have stayed relatively low throughout this conflict is because China has very quickly pivoted toward coal, and away from LNG – and so, competition for cargoes has been artificially subdued.

Whilst China’s Q126 performance is surprising, it’s worth noting that it’s off the back of exports and industrial outputs – domestic demand shows no signs of picking up, and the housing sector is still in dire straits.

Looking at open interest, for the week ending 10th Apr ’26, investment funds have again reduced their net long positions across European benchmarks by up to 12% – so the smart money is slowly, but surely, losing interest in natural gas as a one-way bet.

As we’ve stated repeatedly over the last few weeks, investment funds are still heavily ‘long’ gas – if they exit en masse in the event the Strait of Hormuz re-opens, prices will fall off a cliff.

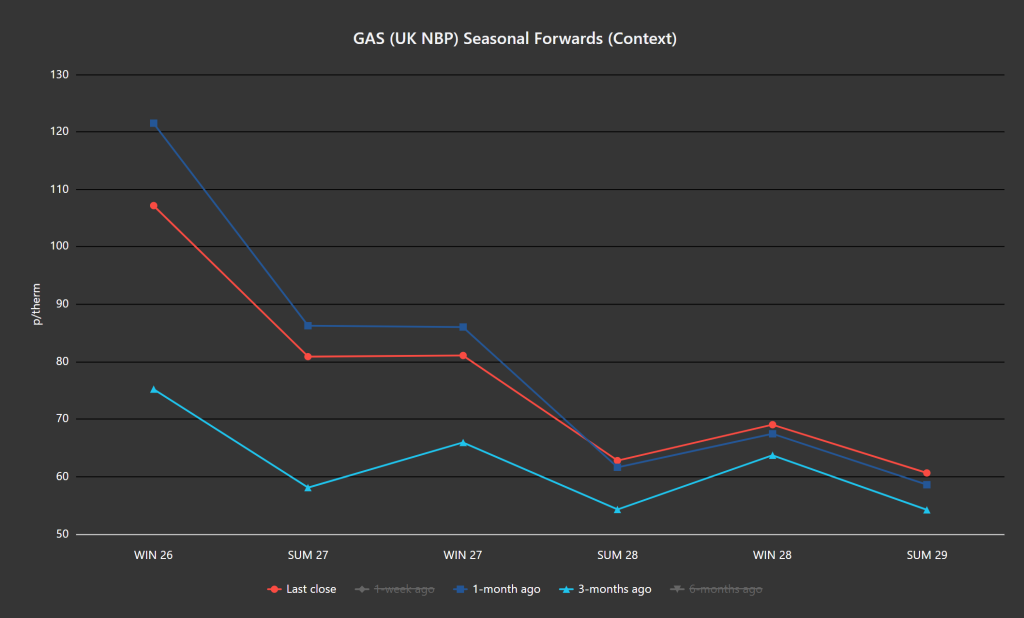

As per the chart below, Seasonal Forwards are down on the month for the front-3 seasons, but still way up versus 3-months ago.

Monthly Day-Ahead Averages for the month so far are lower at 118 p/therm (or 4 p/kwh exc. non-gas).

ELECTRICITY & CARBON

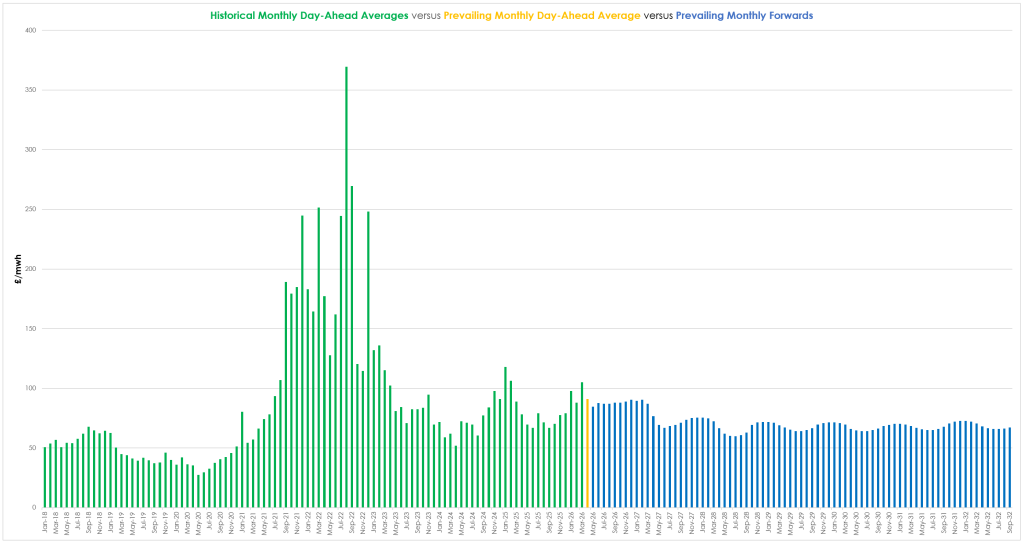

The chart below details UK electricity Historical Monthly Day-Ahead Averages (green), versus the prevailing Monthly Day-Ahead Average so far (orange) versus yesterday’s closing Monthly Forwards (blue).

Clearly, markets remain backwardated (future delivery prices discounted versus near-term delivery prices) – reflecting an underlying sentiment amongst market participants that conditions are expected to improve further down the ‘curve’.

On the Carbon side of things, Dec-26 UKA delivery remains inversely correlated to gas markets – when gas prices fall, UKAs rise (and vice versa).

At the time of writing, UKA mid-price Dec ’26 delivery is at £47.85/tn (and the spot is at late-46s).

Monthly Day-Ahead Averages for UK electricity for the month have fallen slightly to £91/mwh (or 9.1p/kwh exc. non-energy).