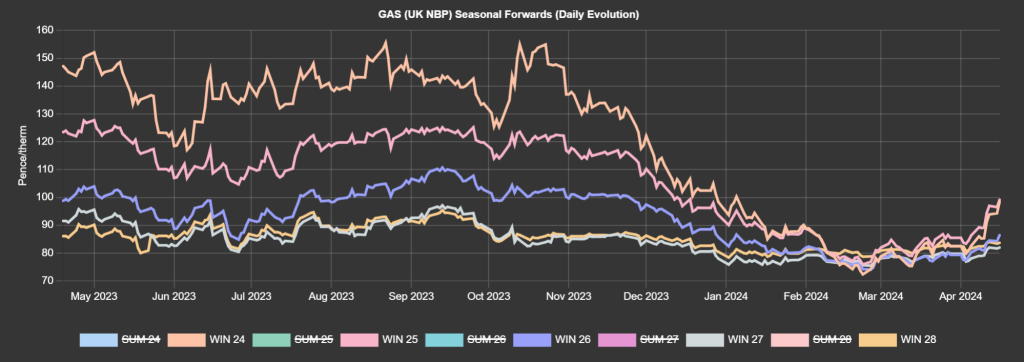

Notably, Winter-24 delivery prices were at a significant premium versus Seasonal delivery thereafter until Mar ’24 when Winter-24 delivery was very briefly offered at a discount to subsequent Seasons (see chart).

At the time of writing however, Winter-24 has lifted once again and only Winter-25 is more expensive versus the rest of the curve.

This shift, of course, is an impact of recent geopolitical tensions in the Middle East (further exacerbated by short-term supply issues at Freeport, Texas and Nyhamna, Norway).

This morning prompt (near-term delivery) contracts were down at open off the back of a long system (supply outrstripping demand forecast).

Curve (far-term delivery) contracts also opened lower this morning, continuing yesterday’s more bearish tone.

Notwithstanding geopolitical risk, key drivers remain mostly bearish with European storage at 62% versus the 5-year average of 43%.

The extended Norwegian outage at Nyhamna has now come to an end (ramping up Langeled pipeline nominations).

Storage withdrawals have slowed with temperatures forecast to rise back above seasonal norms come the weekend.

Market participants are still weighing-up next steps in the Middle East after Israeli officials confirmed that Israel would be responding to Iran’s drone attacks.

All in all, a bearish/corrective tone to the market today.

Monthly Day-Ahead averages are on target this month to achieve 70p/therm (or 2.4p/kwh).

ELECTRICITY & CARBON

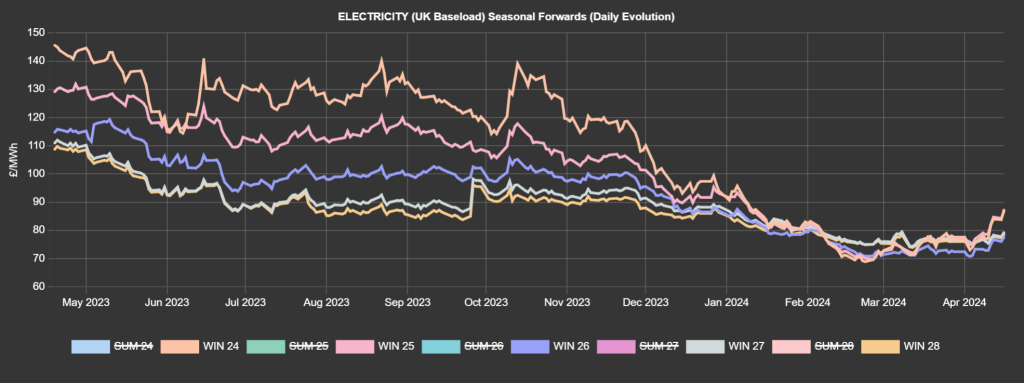

Looking to the continent, European near-term delivery prices cleared mixed yesterday – though prices are expected to drop today off the back of reduced geopolitical hysteria and improved renewables outputs.

Down the curve, prices dropped off alongside the gas and carbon markets yesterday, pressured by increased Norwegian supply and a long-awaited correction of EUAs (European mandatory carbon allowances for big emitters).

The carbon slide was likely fuelled by some profit taking given the overcooked increases we’ve seen over the past few sessions (against a backdrop of contrarian fundamentals).

The COT (Commitment of Traders report) published yesterday was surprisingly unchanged versus that which was published before this week’s bull run.

Speculators saw their net short position reduced only very marginally compared to the previous week – an unexpected result given the large increase of carbon prices (which are now being attributed mainly to short-covering).

Back in the UK, Dec-24 contracts for UKAs are circa. £36/tn.

Our electricity generation mix is very bearish in nature today with renewables contributing 54%, thermal at 7% (gas and coal) and low carbon at 25% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £41/mwh (or 4.1p/kwh).