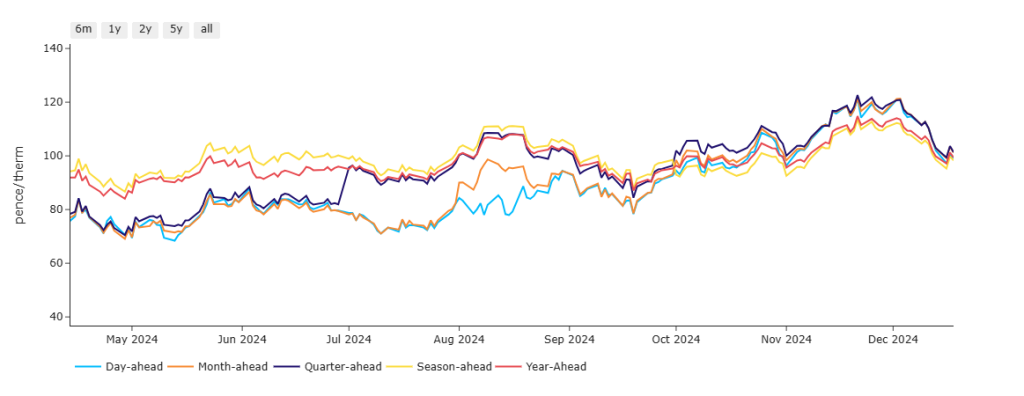

Near-term delivery prices have softened versus 1-week/1-month ago, and are now treading water as we approach the Christmas break (see chart below).

The front month (Jan-25) has spent the last few days hovering at or around 100p/therm (a key pschological support/resistance level) – though is a little higher at the time of writing, trading at 104p/therm.

today’s upside can most likely be attributed to the rumours flip-flopping with regard the Ukraine/Russia transit deal renewal.

Ukraine’s Prime Minister Denys Shmyhal announced on 16th Dec that the deal allowing Russian gas to transit through Ukraine will not in fact be extended beyond the end of the year – despite whispers amongst market participants that a deal was on the verge of being reached.

Putin is expected to speak about the matter in the next few days (which, on the face of it, sounds optimistic).

Given the uncertainty (and likely brinkmanship between the two warring factions), several European countries are being forced to intensify efforts to secure alternative energy supplies.

Solid wind outputs continue to limit gas-for-power burn.

European/UK LNG arrivals remain in good shape, relieving pressure on near-term delivery (and limiting withdrawals).

10 more arrivals are expected into Europe before month-end, including 2 to degasify at UK ports.

In short, prevailing conditions are now being reflected in more reasonable prices for both near- and far-term delivery.

Temperatures are up, wind is up, gas-for-power burn is down, European LNG arrivals are up, China’s LNG imports are down – so the bias retains enough berish momentum to keep a lid on the upside.

The Russian central bank is expected to hike its key interest rate by another 200 basis points this week to 23% – evidently, Putin faces internal pressures heading into 2025 (which might be one of the reasons the Ukraine transit deal is back on the table – can the Kremlin afford to walk away from revenues?)

Monthly Day-Ahead averages are on the slide and on target to achieve 110.098p/therm (or approx. 3.757p/kwh excluding non-gas).

ELECTRICITY & CARBON

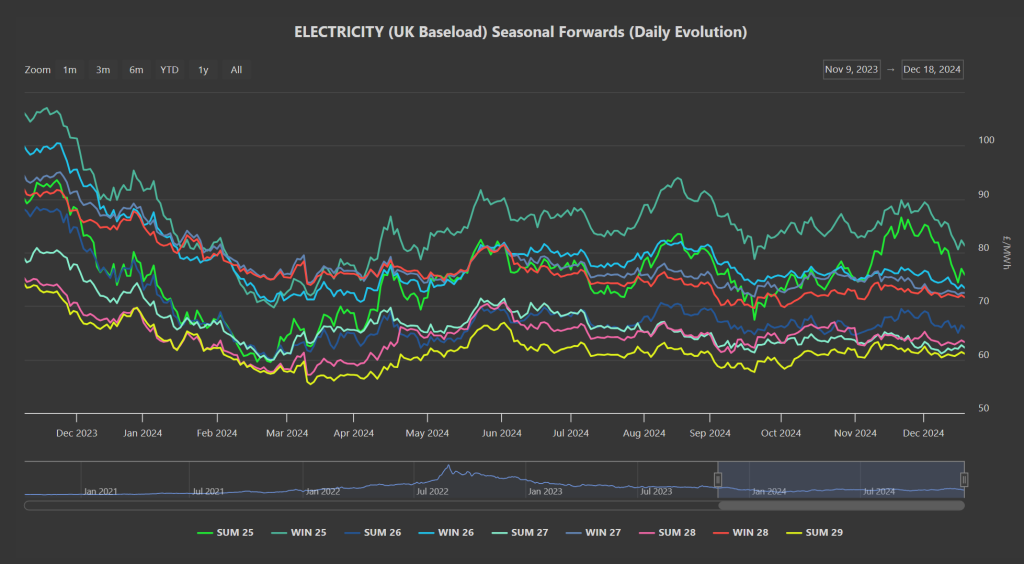

As was the case this time last year, front-season prices (Season-Ahead/2-Seasons-Ahead) are falling in December (see chart below) – reflecting expectations of relatively warm,windy conditions over the Christmas break.

Looking to the continent, French nuclear availability has climbed this week, further attributing to near-term price drops.

On the Carbon markets, prices for both European and UK Allowances saw a mild bullish correction yesterday which has found some modest legs today (on thin volume) – more a lack of selling interest than a meaningful trend reversal.

However, the EUA (European Allowances) COT (Commitment of Trader’s Report) published yesterday did show that the overall net long position remains stable, if reduced (down 10% w-o-w) – so the bulls are still there, but tempered by more bears having added positions.

Though it’s likely if the net long position remains, the bears will be squeezed out, adding momentum to the bullish move in the coming days/weeks.

Back in the UK, UKAs are at £34.29 on the mid (so late 34s on the buy price) – a retest of the all-time lows of £31.30/tn printed on 29th Jan-24 is still a possibility in early ’25.

The UK’s electricity generation mix is bearish in nature today with renewables contributing 59%, thermal at 10% (gas and coal) and low carbon at 21% (nuclear and imports).

Monthly Day-Ahead averages for the month so far are back on the slide and back below £100/mwh at £99.078 (or 9.91p/kwh excluding non-energy).