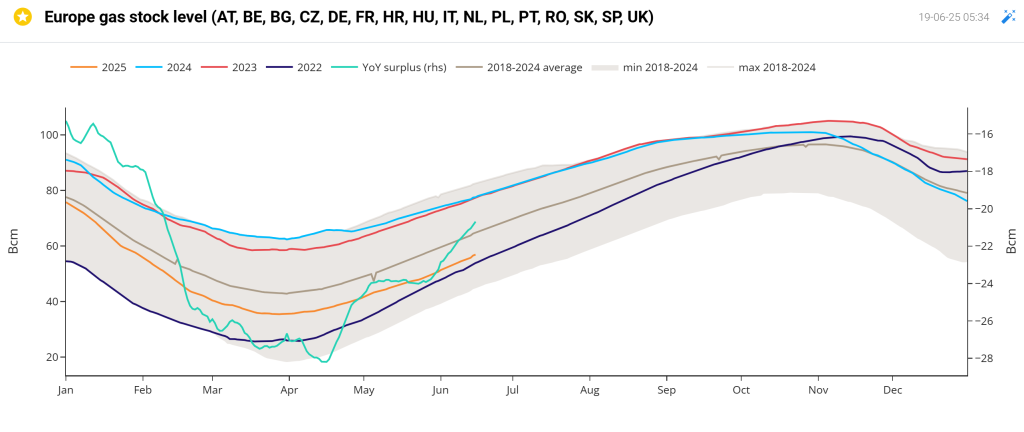

European storage is on the right track, though the injection recovery is rising at a marginally shallower incline than previous years – please see chart below detailing European storage fullness 2018 to date.

Nonetheless, consensus predicts we’ll just about make it to 83% in time for the heating season (1st Nov onwards).

Near-term delivery prices remain well supported, with Winter-25 holding its ground above 100p/therm (108.2p/therm at the time of writing).

Though prices further down the curve have been little altered by the Iran-Israel flare-up – reflecting (surely) market participant’s belief that future gas values will be lower subject to improved global LNG production in the coming months/years.

Rumours abound that Canada could produce its first ever LNG this weekend, from the export facility in Kitimat, British Columbia.

The facility represents just the first of a handful of Canadian LNG projects to begin production this year – significantly reducing sail time to Asian markets (reducing price support across the global LNG market).

But for now, summer buyers are being forced to sit on the sidelines as the Middle East flare-up unwinds.

The risk is very much front loaded, with traders most concerned about safe transit for LNG through the Strait of Hormuz (SoH).

Were there to be a closure of the waterway, 20% of global LNG trade would be impacted, and the associated supply shortages would of course drive the market higher.

European storage is at 54% versus the 5-year average of 64% – so not too far off the pace.

On the trading side, clients running flexible capability are mostly watching from the sidelines as the Israel-Iran conflict develops – in the near term, talk of Iran regime change is pervading the airwaves.

The USS Nimitz has also been redirected from the South China Sea to the Middle East (bringing the total number of US aircraft carriers in the region to two) – will the US engage directly…?

This month’s UK gas Day-Ahead averages are at 87p/therm (or approx. 3p/kwh excluding non-gas) – so benchmark prices are creeping up as the month progresses.

ELECTRICITY & CARBON

Not surprisingly, near-term electricity prices (especially at the front-end) remain well-supported.

Winter-25 is at £95/mwh (so an increase of 19% versus the lows we saw back on 1st May).

Prices all the way down the curve are up (or commensurate) with those offered 1-week/1-month/3-months/6-months ago – please see chart below detailing Winter-25 to Summer-26 Seasonal Forwards.

On the Carbon side of things, UKAs continue to drift toward parity with EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May – UKAs remain well-bid sitting at £53.09 on the mid-price this afternoon.

Today’s UK electricity generation mix is bearish in nature reflecting benign ‘summery’ weather conditions and limiting gas-for-power burn – specifically, renewables are contributing 43%, thermal at 14% (gas and coal) and low carbon at 24% (nuclear and imports).

Electricity Day-Ahead averages for the month are creeping up in response to Iran-Israel risks – currently at £69/mwh (or approx. 6.9p/kwh excluding non-energy).

On the trading side, clients running flexible capability are mostly watching from the sidelines as the Israel-Iran conflict develops.