Trump’s escalating war on Iran is breaking global markets.

Inevitably, the US/Israel attack on the Iranian South Pars gas field yesterday (the world’s largest) resulted in a retaliatory strike on Qatari LNG production (Ras Laffan Industrial City) as well as key infrastructure along the Persian Gulf.

In the UAE, authorities are responding to incidents at the Habshan gas facilities (one of the world’s largest gas processing facilities) and at the Bab oil field caused by falling debris from intercepted missiles – the gas facilities have been shut down.

Near-term delivery spiked as much as 35% before pulling back in the last hour or so, as traders weigh up not only the closure of the Strait of Hormuz, but also the impacts of damaged LNG production/distribution infrastructure.

Meanwhile, in the US, the Trump Administration’s Intelligence personnel continue to seemgly distance themselves from Trump’s argument that Iran posed an imminent threat.

Hot on the heels of Joe Kent’s resignation this week (high ranking intel official), the Director of National Intelligence, Tulsi Gabbard, stunned the Senate Committee yesterday by stating that it wasn’t her job to determine what is an imminent threat to the US.

She went on to say that “the only person who can determine what is and is not an imminent threat is the president…”

Increasingly, analysts are pointing towards Trump’s disregard where Europe and historical allies are concerned – as a net exporter, America’s exposure to this meltdown is limited to ‘gas’ prices at the pump (which are at their highest levels since ’23).

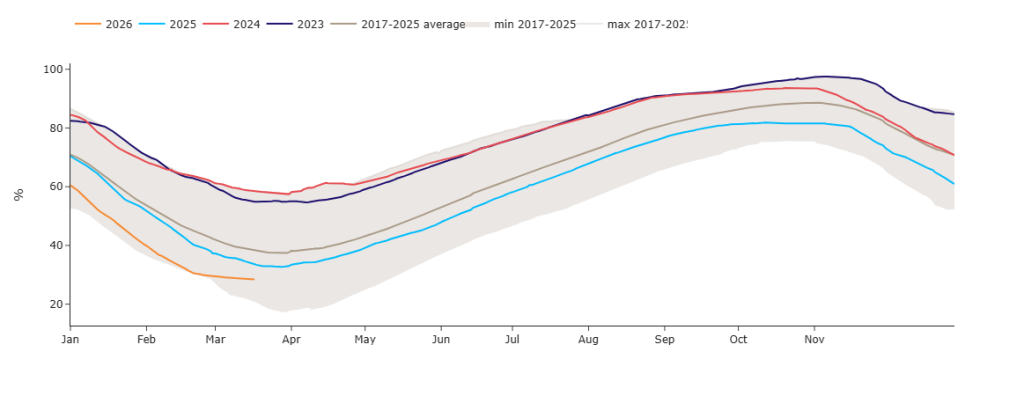

Europe/the UK’s achilles heel remains summer replenishment of storage fullness (now at 29% versus the 5-year average of 42%, please see chart below) – Trump’s chosen war (as it’s increasingly being referred to across the airwaves) is intensifying global competition for LNG cargoes just when Europe was looking forward to a steady glut of LNG depressing prices all the way down the curve.

For their part, European leaders are once again being called upon to come up with ways for consumers to survive the coming weeks/months.

Italy’s government has approved a temporary cut to fuel taxes, as well as considering a windfall tax on profiterring energy companies.

As is often the case with Trump-related attacks, the bad news happens whilst Western markets are closed (overnight and/or weekends) – so, markets ‘gap-up’ the instant the bell rings due to the sheer volume of orders-at-market.

Trump is claiming that the US had no knowledge of the planned Israeli strikes on the gas fields – though has conceded that if Iran were to make further strikes on Qatar that they would ‘blow up’ the South Pars gas field.

Monthly Day-Ahead averages for the month remain high – currently at 125p/therm (or 4.2p/kwh).

ELECTRICITY & CARBON

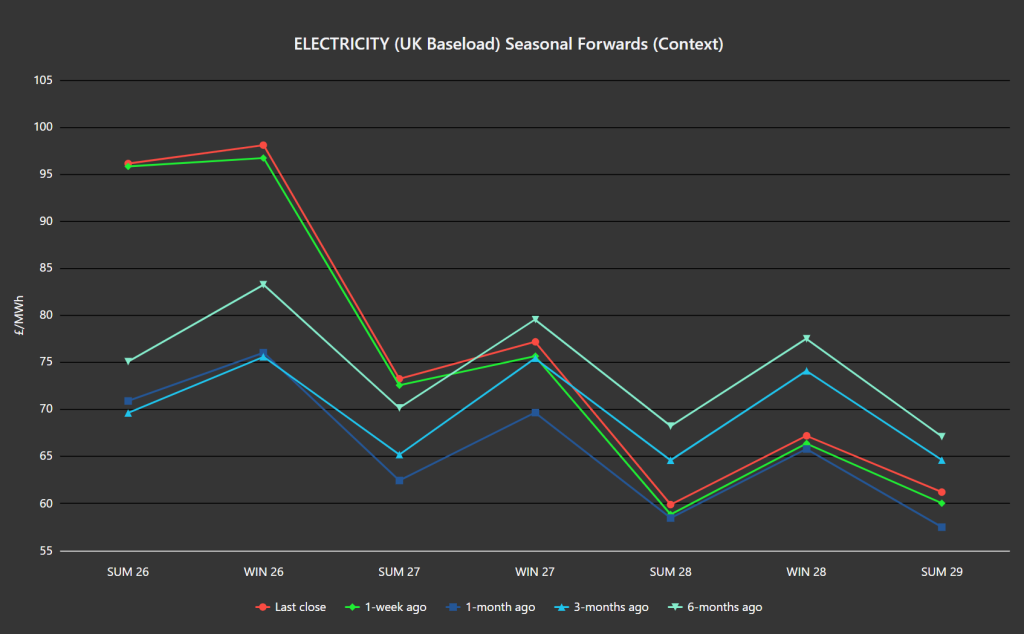

As per the Seasonal Forward Context chart below (showing how prices are changing over time), electricity Seasonal Forwards for the front 3-Seasons are up versus 1-week/1-month/1-Quarter/6-Months ago.

Conversely, on the Carbon side of things, Dec-26 UKA delivery remains uncoupled from gas volatility with prices touching levels that are 46% below those printed in mid-Jan amid fears that Trump’s war on Iran is slowing global economies (and, in so doing, Industrial outputs).

At the time of writing, UKA mid-price Dec ’26 delivery is at £34.60/tn (and the spot is at mid-32s).

Monthly Day-Ahead averages for the month so far are mirroring near-term gas prices – currently at £115/mwh (or 11.5 p/kwh).