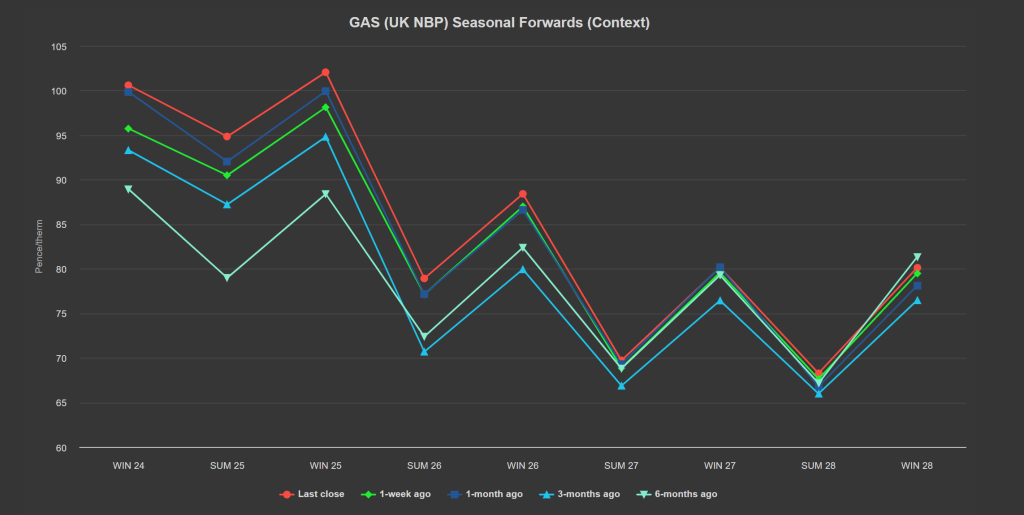

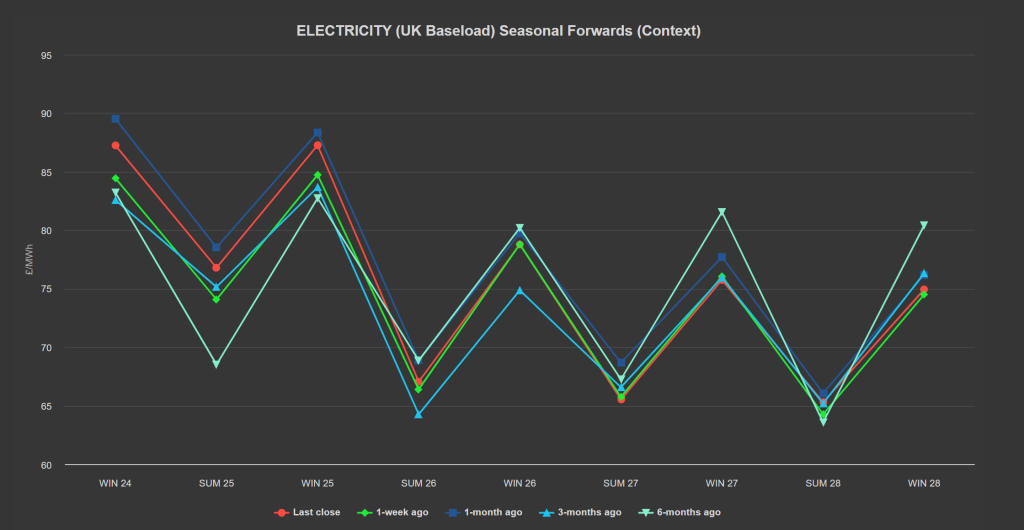

As evidenced in the charts below, the front 3 Seasons of gas delivery are now up on the month, whereas the front 3 Seasons of electricity remain down on the month – reflective surely of the heightened risk-premium now being built-in to gas off the back of fears of supply tightness should Middle East tensions contribute further to global geopolitical uncertainty.

Frustratingly for buyers who’ve opted to allow summer conditions to deepen before pulling the trigger on hedging the front seasons, markets have picked up some bullish momentum today, with Winter-24 up by approx. 5p/therm versus the start of the week.

The stories remain the same against a backdrop of relatively benign summer conditions – however, the strike on the Hamas leader in Tehran increases the risk of direct confrontation between Israel and Iran.

With Iran expected to respond to the latest air attacks, market participants assign a potentially higher value to the transportation of gas globally.

Our UK system was long at this morning’s open (supply outstripping demand forecast) – allowing for injections and exports.

Norwegian flows remain strong – though the conclusion of scheduled summer maintenance is diarised to happen at month-end which is likely to reduce flows out of the continent into the UK.

Also, our summer temperatures continue to disappoint and are expected to fall at the end of the week to below seasonal norms (which will see some increased LDZ heating demand).

Thankfully, increased wind outputs are forecast for the same period which should mitigate gas-for-power burn.

Extreme global temperatures continue to sustain cooling demand across Asia, heightening competition (and prices) for LNG cargos.

Our partner, the USA, is choosing to ship less LNG to Europe, instead opting for the higher prices available in Asia – meaning of course that Europe remains bound to the remnants of Russian gas imports.

Despite common misconceptions, Russia has maintained a consistent supply of LNG to Western Europe since the Ukraine invasion – were this to end now, markets would spike further – a prospect/opportunity that will not be lost on President Putin…

Over the course of Summer-24 so far, demand has remained low against a backdrop of comfortable supply – as such, replenishing gas stocks has not posed any problems.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24).

European storage is at 85% fullness versus the 5-year average of 78%.

On the hedging side, we’re now on the other side of Summer-24 – with 123 days having elapsed, and 61 remaining.

Clients with open volumes for Winter-24 are now in the minority – with most having opted to close-out Positions given the ongoing geopolitical uncertainties and winter conditions now on the horizon.

Monthly Day-Ahead averages so far this month are on target to achieve 85p/therm (or circa. 2.9p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices increased again yesterday as the supply/demand balance remained tight.

But the upside potential is now limited, and a downward correction cannot be ruled out assuming the heat goes out of market participants’ over-reaction to geopolitical worries.

On the Carbon markets, EUA continue their bullish rally (correlating with recent gas price rises).

Back in the UK (and despite EUA’s bullish tone), UKAs (UK Carbon Allowances) have been slow to react – instead almost retesting £38/tn to the downside before being dragged back up by EUAs’ bullish fervour – now trading at circa. £40/tn.

At the time of writing, our electricity generation mix is neutral in nature today with renewables contributing 31%, thermal at 30% (gas and coal) and low carbon at 26% (nuclear and imports).