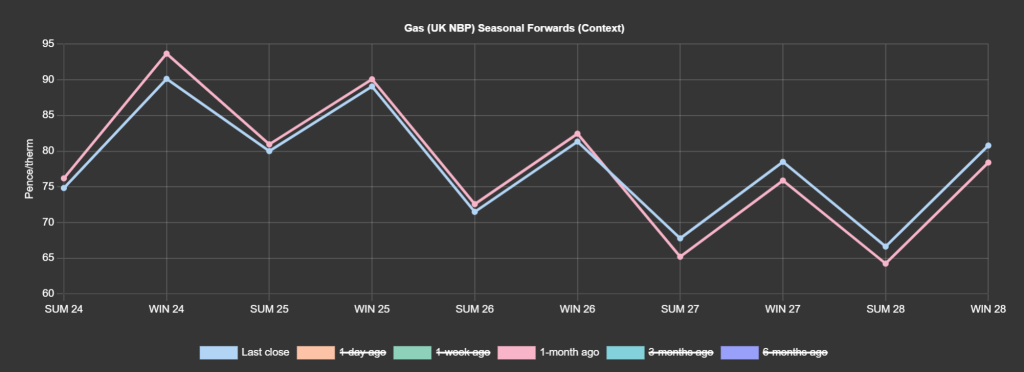

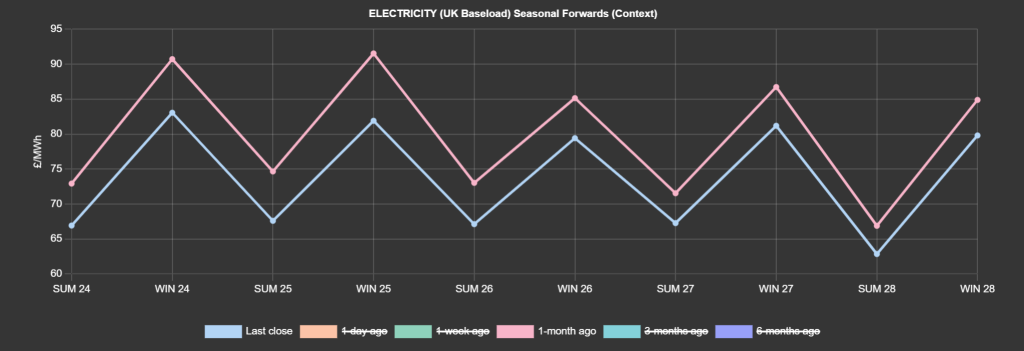

Looking down the curve, the divergence between gas and electricity risk-premiums grows increasingly evident m-o-m (with only 59 days of Winter-23 remaining) – see charts.

Prices have spent the last few days unwinding/correcting following a sustained bear rally over the preceding weeks.

At the time of writing, near-term delivery prices are marginally down on the day despite a short UK system at this morning’s open (demand outstripping supply).

European Industrial demand destruction persists with consumption predicted to be about 22% lower than seasonal averages – coupled with a circa. 10% decrease in European gas production y-o-y.

European storage is at 71% versus the 5-year average of 55%, reflecting limited withdrawals over the past few weeks.

All in all, a quiet day on the markets with prices consolidating sideways.

Confidence in storage levels pervades underlying sentiment with consensus building that European storage will end Winter-23 with more than 50% still left in the tank.

The Freeport LNG terminal in Texas expects Train 3 to be out of service for about a month due to an electrical fault.

Geo-political risk persists in the form of Middle East escalations and lingering worries over supply disruption in the Red Sea/Suez Canal (limiting downside).

Favourable weather conditions into early February are expected to keep a lid on any sustained bull-run.

Monthly Day-Ahead averages are on target this month (so far) to achieve 74p/therm (or circa. 2.5p/kwh).

ELECTRICITY & CARBON ALLOWANCES

Looking to the continent, near-term delivery prices are down on the day.

Temperatures are high this week – between 3°C and 6°C above seasonal averages, suppressing demand.

Wind outputs look high for the weekend, with chances of negative prices intraday on 4th November with residual loads (total load minus renewables generation) expected to be nigh-on zero.

Down the curve, the bear rally has lost steam and market participants are likely looking to fuels for direction.

On the carbon market, the situation appears similar as on the power side – a risk off (reducing exposure to protect capital) is still a possibility, though technical momentum indicators are pointing northwards reflecting an unwinding of oversold conditions – so further downside still looks likely in due course.

Back in the UK, our generation mix is bearish – 43% renewables and 25% gas-for-power burn.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £62/mwh (or 6.2p/kwh).