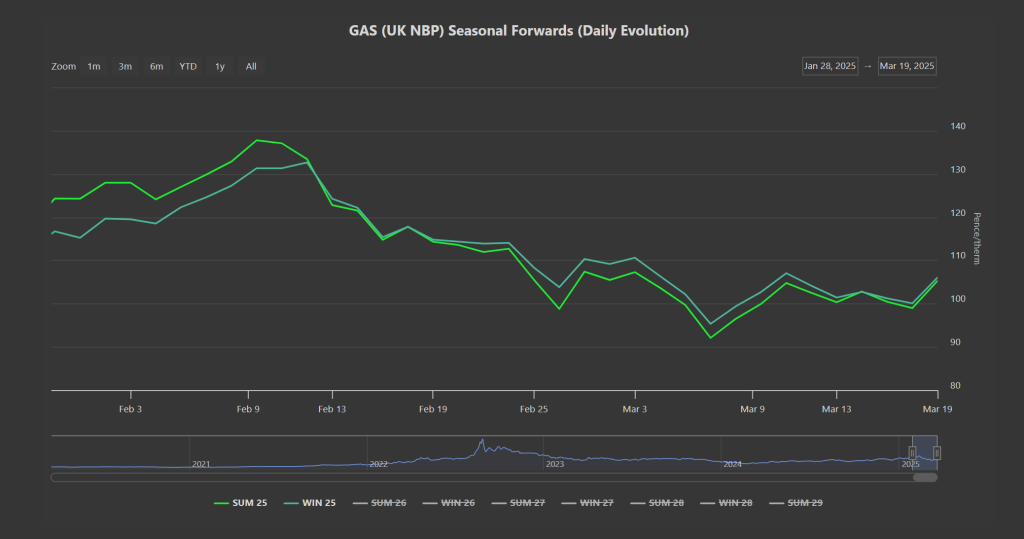

Beginning 13th Feb, Summer-25 re-established it’s discount versus Winter-25 (please see chart below) – reflecting participants’ improving confidence in Europe’s ability to replenish stocks in advance of the mandated 90% by 1st Nov.

Whilst this discount is holding (just about), Trump’s failure to convince Putin as to the merits of a full 30-day ceasefire has put some heat back in the market.

Participants evidently regard this latest development as a setback and a delay in the return of Russian gas flows into the European system (at least before the summer-rush) – which of course leaves us competing with Asia for LNG across the summer months.

For now, LNG netbacks favour cargoes heading to Europe (netbacks are the price earned by a producer of LNG, and is calculated using the market price minus delivery charges).

Trumponomics is having a more favourable impact on LNG exports into Europe/the UK, with more than 30 arrivals (mostly from the US) expected before month-end.

In addition, Trump’s determination to increase fossil fuel outputs has resulted in Venture Global’s proposed $28 billion LNG export project (based out of Louisiana) being given the green light.

European storage is at 34% versus the 5-year average of 57% (and the 6-year average at 44%).

Monthly Day-Ahead averages for this month so far are on track to improve on last month’s final number (124p/therm), with averages holding steady at 103p/therm at the time of writing (or approx. 3.5p/kwh excluding non-gas).

ELECTRICITY & CARBON

Near-term delivery contracts tracked gas markets northwards yesterday.

Today’s UK electricity generation mix is marginally bearish in nature, with renewables contributing 35%, thermal at 27% (gas and coal) and low carbon at 33% (nuclear and imports).

On the Carbon markets, EUAs nd UKAs (European and UK mandatory allowances for heavy emitters) had reversed all last month’s gains off the back of multiple bearish drivers including milder temperatures, slowly improving renewables outputs, rumours of a potential Ukraine-Russia peace deal, increased tariffs and soft macroeconomic data.

However, with the partial resurgence in near-term gas prices this week, Carbon is following suit.

At the time of writing, the UKA mid-price is at £46.53/tn and testing resistance of a shallow bearish trend channel (please see chart below).

However, the RSI (relative strength index, a momentum indicator) has developed bearish divergence signalling a potential period of consolidation or trend reversal.

Monthly Day-Ahead averages so far for this month are holding steady below £100/mwh at £92/mwh (or approx. 9.2p/kwh excluding non-energy).