Minor support came from a one-day extension to the Visund (North Sea field) maintenance and duration remains uncertain.

This morning, the fundamentals are barely changed.

We expect the balance to loosen as gas for power demand is reduced as the interplay with wind power generation forecasts continue to cause some variation in gas for power demand forecasts.

LDZ (heating demand) remains on a falling trajectory.

The supply side appears stable for the coming days as maintenances on the UKCS (continental shelf field) will last at least another week.

LNG activity should remain low as only one vessel is on the horizon, expected in a week’s time at South Hook.

Looking at the bigger picture, lingering heat waves in the US, Asia and Italy also likely contributed to some pressure on the global gas markets (additional gas-for-power burn needed for cooling demand).

The European supply side is a mixed bag, as LNG sendout remains weak and is falling for the remainder of the month.

Norwegian flows however should remain at max capacity for the foreseeable future as maintenance impact is low.

In the meantime, EU ambassadors are discussing further sanctions on Russia.

So far, some resistance on stricter rules for re-exports of Russian gas appears to come primarily from Germany.

As of now however, this should not have significant impact on current prices – sideways movement will likely continue.

We’re 81 days into Summer-24 (103 days remaining).

Strong warmth is expected next week – the UK will see temperatures peak at 5 degrees above seasonal norms by Wednesday.

Fundamental drivers have softened from last week allowing for decent storage injections.

Overall, as long as the geo-political landscape remains “quiet” (!), the trajectory will be one of sideways price action into next week.

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices rose yesterday off the back of forecasts of weaker wind output and French nuclear availability along with a substantial rise of fuels and emissions prices.

Down the curve, Forward prices tracked the increase of gas and emissions prices.

The bullish momentum was attributed mostly to strengthening competition on the LNG market from an expected heatwave in the US and Europe, and French parliamentary committee advising an end of Russian LNG imports.

On the Carbon markets, the Dec ’24 EUA benchmark contract climbed back above the 70€/t mark.

Prices are pursuing their rebound this morning despite relatively steady gas prices, although resistance in the form of the 50-day moving average is unlikley to break to the topside given fundamentals remain mostly benign.

Yesterday saw the release of the COT (Commitment of Traders Report) showing a rise in speculators’ net short positions.

These newly built short positions might be getting squeezed by this week’s significant price rebound – a reflection of prices at equilibrium (with bulls and bears battling to make a trend happen).

Our electricity generation mix is neutral in nature today with renewables contributing 20%, thermal at 32% (gas and coal) and low carbon at 30% (nuclear and imports).

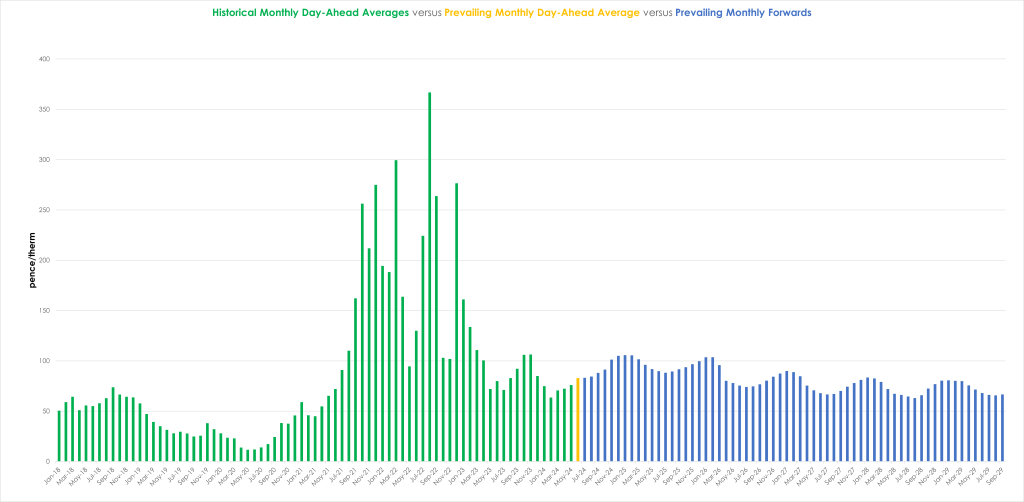

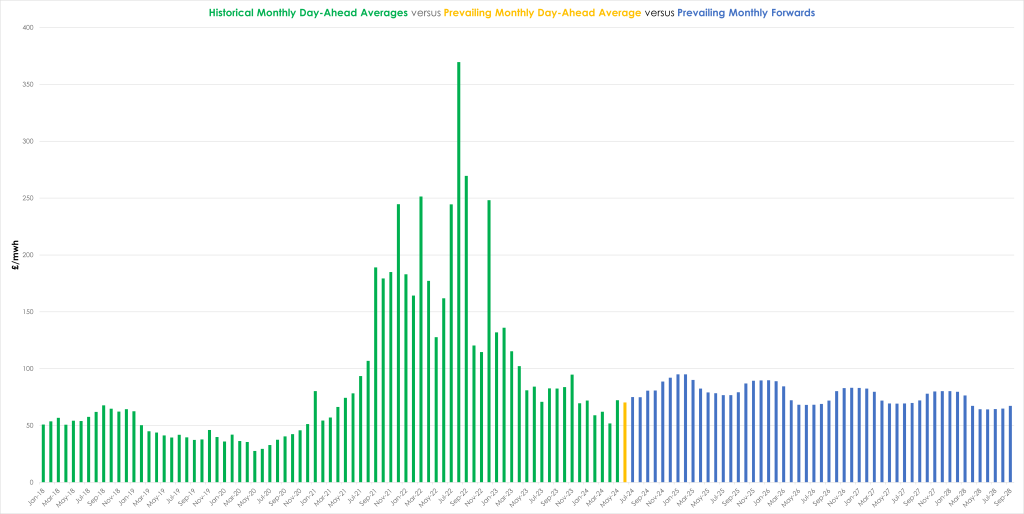

Monthly Day-Ahead averages are on target this month to achieve £70/mwh (or 7p/kwh excluding non-energy).