Whilst prevailing Forwards are as much as 88% below those printed back in ’22, markets remain traumatised at the prospect of supply tightness.

Despite overwhelmingly bearish fundamentals, and the impacts of summer conditioning to look forward to, an appetite still exists amongst market participants/speculators to take the market higher at the first hint of supply disruption.

Increased LNG imports have gone a long way toward shoring-up the holes left in European/UK supply (since Russia turned off the taps).

Nonetheless, this shift in dynamic doesn’t change the fact that we have less gas available to us than we did up to and including mid ’21.

As such, markets are increasingly inclined it would seem to react disproportionately bullishly off the back of news which MIGHT reduce supply further down the line.

This week has seen sharp increases specifically for Winter-24 and Winter-25 delivery – with Seasonal Forwards now back above the psychological level of 100p/therm.

UK prices lifted significantly this morning – from front to back – with Month-Ahead having risen 4p/therm on the day (up 5%).

An Austrian oil and gas group (OMV), stated yesterday that pipeline gas supplies from Russia’s Gazprom may be suspended through a ruling obtained by a major European energy company from a foreign court – this will likely mean Russian gas supply disruptions to Austria.

Given expectations that this volume would continue throughout 2024, the fear of reduced flows has left the market short.

In addition, a lead contractor for the U.S. Golden Pass LNG export plant filed for bankruptcy on Tuesday raising concerns over further delays regarding the plant startup date (illustrating clearly the limitations of our increased reliance on LNG now that Russia’s pipeline flows have been lost).

Norwegian gas flows to the UK and NW Europe are still below the 5-day moving average despite a recent increase in Norwegian gas production levels.

This morning, the UK’s Norwegian nominations are down by 26mcm/d, with exports being rerouted to Continental Europe.

Clients floating on the Day-Ahead are increasingly eyeing-up Winter-24 Seasonal Forwards wondering if the lows we saw back at the end of Feb ’24 will even be resested over the coming summer months!

Looking at TTF (European benchmark) for an indication of what might happen next, Month-Ahead prices rose above the 12-month moving average yesterday – however, a singular occurrence of the daily price above the 1-year average does not in itself signify an uptrend (or trend reversal) – yet.

For the reversal to be confirmed, prices would need to consolidate ABOVE the 1-year average.

This could be challenging against a backdrop of European gas stocks at 68% versus a 5-year average of 54% and Norwegian supplies headed in the right direction – as such, a bullish trend reversal remains unconfirmed.

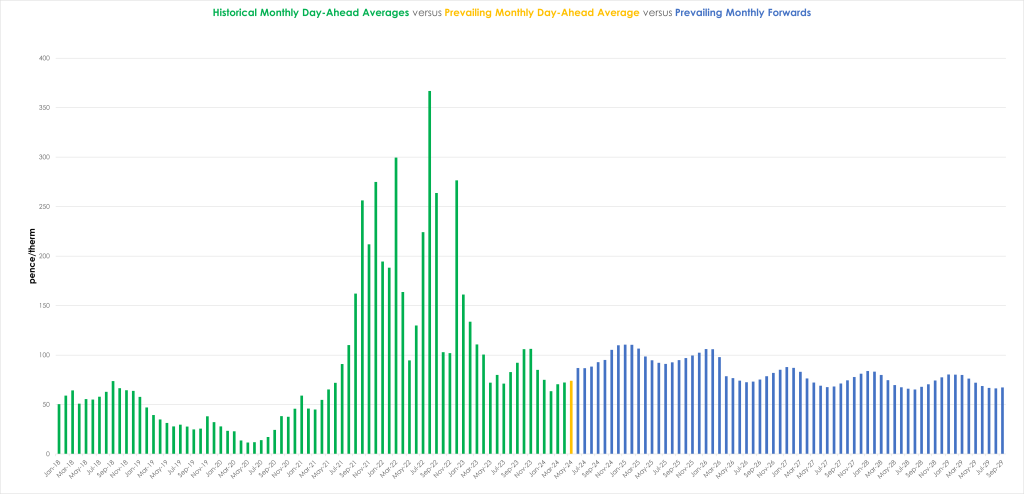

Back in the UK, Monthly Day-Ahead averages are on target this month to achieve 73p/therm (or circa. 2.5p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices continued to rise yesterday amid anticipation of plummeting wind output and weaker French nuclear availability, with additional support from the soaring gas prices.

On the Carbon markets, prices diverged from the so-far correlated gas market on Wednesday.

The EUA (European Allowances) benchmark contract indeed reached a four-month high in the first hour of trading but quickly reversed to fade throughout the remainder of the day, despite the gas prices pursuing their steep ascent

The weekly COT (Commitment of Traders report) published yesterday showed that investment funds surprisingly raised back their net short position by 2.6mt (million tonnes) last week.

This change in position could explain the sharp volatility to the upside of the carbon market earlier this week as speculators might have been forced to shut their newly built shorts (sell positions) when gas prices started to soar again.

Back in the UK, UKAs (UK Allowances) are trading at circa. £44/tn (Dec-24 benchmark) – having broken above the highs printed on 25th Mar ’24 and now breaching overhanging trend lines (see chart below).

Our electricity generation mix is bearish in nature today with renewables contributing 52%, thermal at 8% (gas and coal) and low carbon at 27% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £72/mwh (or 7.2p/kwh excluding non-energy).