Markets are rangebound – supported by ongoing geopolitical tensions, pressured by high storage and the gradual onset of summer conditioning.

For the first time in a fortnight, the UK system opened short this morning (forecasted demand outstripping supply) following weeks of reduced Norwegian flows (with unscheduled outages still ongoing).

Storage withdrawals have been on the up today, off the back of below average seasonal temperatures – increasing heating demand amid subdued renewables outputs (and higher gas-for-power burn).

We’re unlikely to see temperatures climb back above seasonal norms until 1st May.

Prices were marginally up across the board today continuing yesterday’s late rally.

Notably, LNG consumption across the world has risen by more than 40bcm (billion cubic metres) since Russia’s invasion in Feb-22 (and the associated reduction in Russian gas flows into Western Europe).

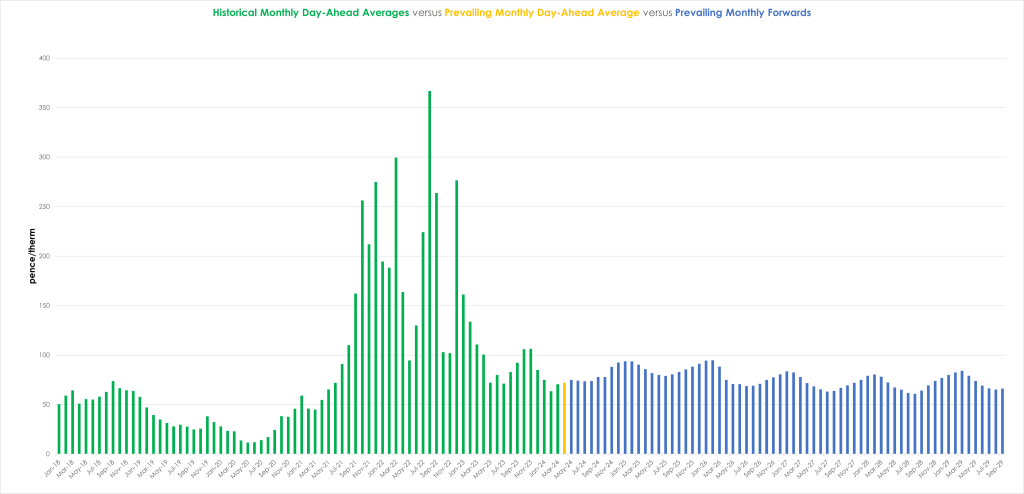

Monthly Day-Ahead averages are on target this month to achieve 72p/therm (or 2.4p/kwh).

ELECTRICITY & CARBON

Looking to the continent, European short-term delivery prices eased yesterday amid anticipation of milder temperatures (although still well below average) and a rebound in wind production, with additional pressure from fading fuels and emissions prices.

The emissions and power curve prices continue to mirror gas movements.

The energy complex indeed attempted a rebound in the morning but sellers took over the markets in the afternoon and most contracts eventually settled below their previous settlements at the end of a pretty uneventful session.

Interestingly, the carbon benchmark contract (Dec’24) displayed a little more resistance to the bullish pressure, which suggests that participants adopted a “wait-and-see” posture ahead of this week’s COT (commitment of traders’s report).

In short, it’s sideways price action amid balanced fundamentals.

Back in the UK, Dec-24 contracts for UK ETS are circa. £37/tn.

Our electricity generation mix is a little bullish in nature today with renewables contributing 21%, thermal at 42% (gas and coal) and low carbon at 25% (nuclear and imports).

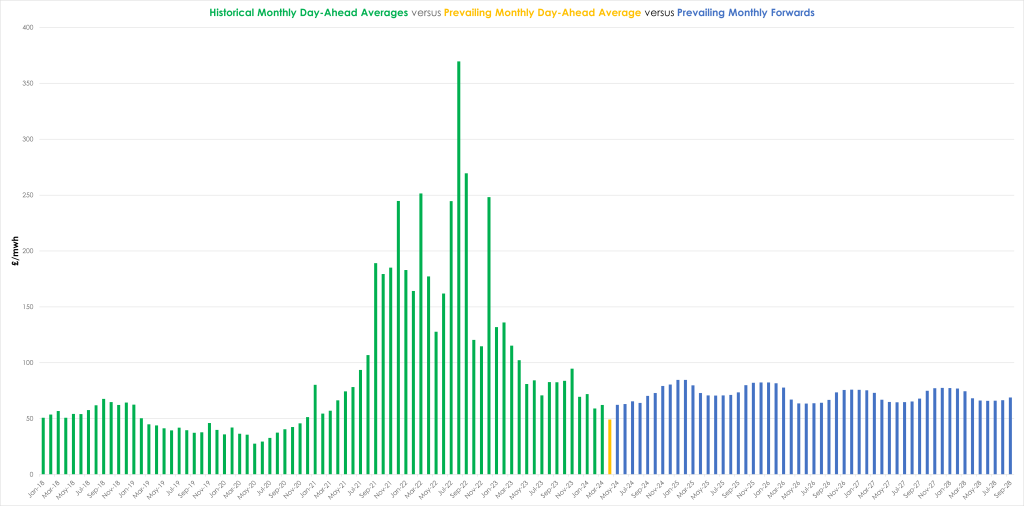

Monthly Day-Ahead averages are on target this month to achieve £50/mwh (or 5p/kwh).