And just like that, prices are back below pre-Israel/Iran skirmish levels.

As soon as it became clear on Monday that Iran’s retaliatory attack on the US air base in Qatar was designed to save face (not cause any real damage), oil and gas markets dropped sharply – clearly, the heat had gone out of the situation and Iran had accepted that escalating the conflict would most likely result in the regime’s demise.

Iran even warned the Trump administration in advance of their attack so that the site could be made safe for US personnel/equipment.

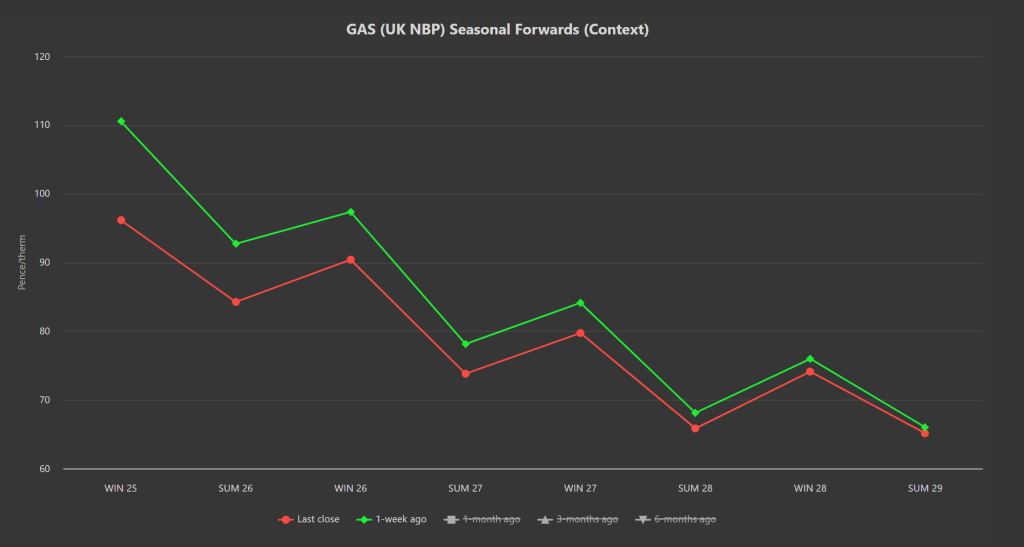

At the time of writing, Winter-25 has dropped 15% versus 1-week ago (please see chart below detailing Seasonal Forwards versus 1-week ago).

All prices down the curve are back below the psychological level of 100p/therm.

Amid solid renewables outputs and low gas-for-power burn, injections into storage are in good shape (further easing pressure on prices) – European storage is at 57% versus the 5-year average of 66%.

China’s demand for LNG remains subdued with their oversized economy looking increasingly shaky (against a backdrop of US tariffs which threaten to further weaken Chinese output).

Of course, risk remains given geopolitical tensions – though the US and Iran will be meeting next week to no doubt reach some sort of accommodation that will ensure the regime survives if/when they do as Trump wishes.

Interestingly, research has found that global gas consumption rose by more than 2% in 2024 (having fallen in 2023).

The rebound in global gas consumption makes clear that despite 16% growth in renewable energy sources over the same period, the pace of renewables adoption fell short of replacing the need for gas to power grids and industry.

On the trading side, clients running flexible capability are encouraged to consider scaling-in partial hedges over the coming days/weeks (now that price stability has returned).

This month’s UK gas Day-Ahead averages are at 88p/therm (or approx. 3p/kwh excluding non-gas) – though we should see this soften over the coming days.

ELECTRICITY & CARBON

Electricity prices remain tethered to gas movements.

Winter-25 is back down to £85.05/mwh – so down 12% versus 1-week ago.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

As such, prices have dropped steeply in line with European/UK gas falls.

At the time of writing, Dec ’25 UKA benchmark prices are at £48.46/tn on the mid-price (a drop of 12% versus 12th May) – next stop looks likely to be £47/tn (lower extremity of rising trend channel) but if the bears get hold of things, the next meaningful support level is down at £44/tn (please see chart below).

Today’s UK electricity generation mix is bearish in nature reflecting benign ‘summery’ weather conditions, limiting gas-for-power burn – specifically, renewables are contributing 45%, thermal at 13% (gas and coal) and low carbon at 30% (nuclear and imports).

Electricity Day-Ahead averages are at £67/mwh (or approx. 6.7p/kwh excluding non-energy).

On the trading side, clients running flexible capability are encouraged to consider scaling-in partial hedges over the coming days/weeks (now that price stability has returned).