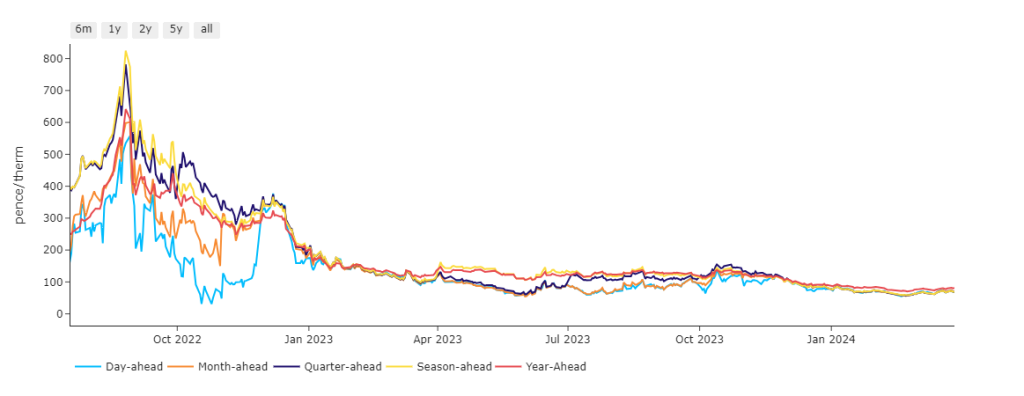

UK gas markets have found equilibrium (versus the highs of 2022) – see chart.

With markets closed tomorrow and Monday, it’s a mixed bag to end the trading week.

From a bearish perspective, demand is weak, temperatures are warming up, and wind outputs look good for the weekend.

From a bullish perspective, French nuclear availability has dropped off with two unscheduled outages and LNG arrivals to Europe/UK all but halted.

Down the curve, contracts are trading sideways with temperatures forecast to be above seasonal norms heading into April and global temperatures continuing to set new highs (reducing heating demand).

Only a few days of Winter-23 remain, and buyers are looking to summer conditioning to further soften Winter-24 offers.

Monthly Day-Ahead averages are on target this month to achieve 68p/therm (or 2.3p/kwh).

ELECTRICITY & CARBON

Looking to the continent, near-term delivery prices declined as expected yesterday, driven down by forecasts of soaring wind output and rising temperatures largely offsetting the higher fuels and emissions prices, and weaker solar generation that was expected for the coming days.

Whilst rising temperatures should keep the market under pressure, prices could find support in prospects of easing renewable production over the last session of the week.

The power curve prices traded sideways on Wednesday, mirroring as usual the gas and carbon markets.

The carbon prices unsurprisingly continue to follow the fuel complex and managed to close yesterday above their 5-day moving average.

The COT (Commitment of Traders report) published yesterday showed that speculators reduced again their net short position for the fourth consecutive week.

Dec-24 contracts for UKAs are sitting at £38/tn.

Our electricity generation mix is bearish in nature this afternoon with renewables contributing 43%, thermal at 15% (gas and coal) and low carbon at 20% (nuclear and imports).

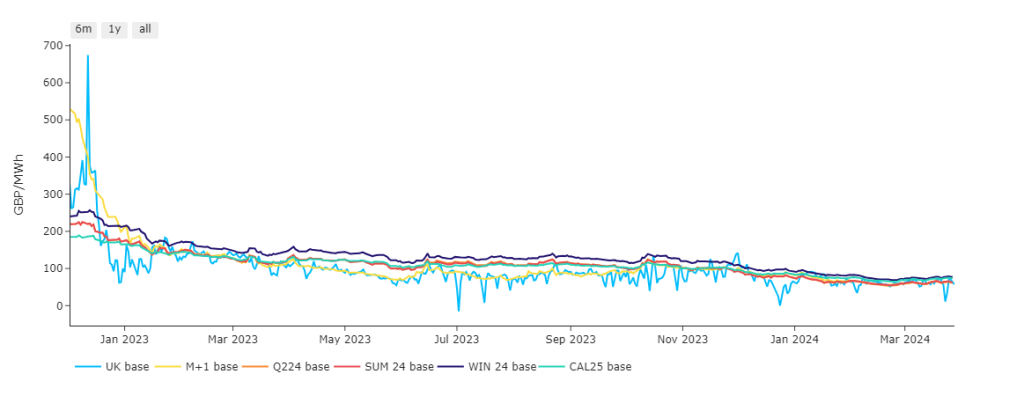

Monthly Day-Ahead averages are on target this month to achieve £62/mwh (or 6.2p/kwh).