(Please see Month-Ahead technical chart below) Benchmark month-ahead delivery continues to observe the confirmed ascending trend channel (as has been the case since the bottom of the 2024 market posted on 23rd Feb) – though, at the time of writing, prices are retesting the psychological resistance level of 100p/therm (last challenged on 12th Aug) amid persisting bearish divergence on the RSI (momentum indicator) suggesting the bullish trend which began on 20th Sep is running out of steam as it approaches resistance – we’ll update on how this price-action plays out.

Today, it’s sideways movement off the back of a long system right now (supply outstripping demand forecast) against a backdrop of unscheduled Norwegian outages at Asgard and Troll (resulting in 23 million cubic metres capacity offline).

Down the curve, delivery contracts are marginally higher today off the back of burgeoning supply concerns given Middle East escalations.

Market fundamentals are strong amid historically high European gas storage levels (94% – at the upper extremity of an 8-year range) ) and recovering Norwegian flows following a period of summer-end scheduled maintenance.

Milder weather is forecasted to pass through Europe next week, keeping a lid on heating demand.

Wind outputs are forecast to be in good shape into the second half of the month, also limiting gas-for-power generation demand.

Oil markets remain very susceptible to Middle East discord, particularly as concerns grow over the increasing likelihood of interruptions to shipments via the Strait of Hormuz.

Monthly Day-Ahead averages so far this month are on target to achieve 94p/therm (or approx. 3.207p/kwh excluding non-gas).

ELECTRICITY & CARBON

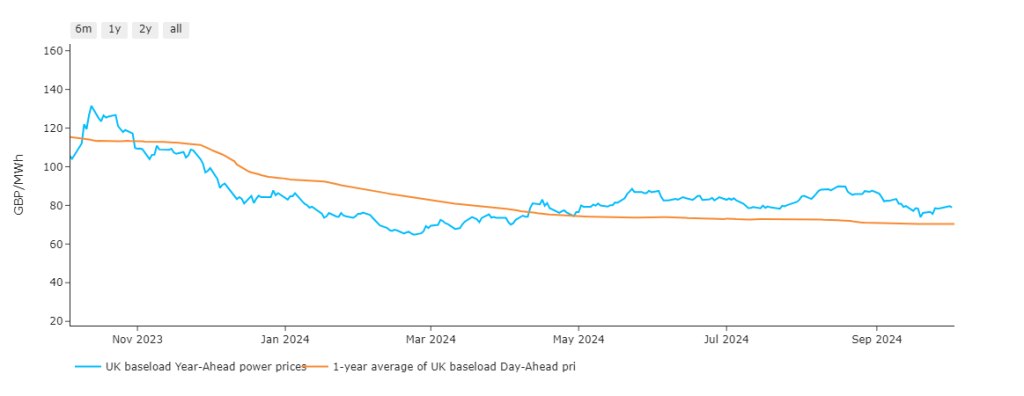

Notably (as per chart below), Year-Ahead electricity rose above the annual average of Day-Ahead prices in mid-April – the significance being a rise in risk-premium over the mid-term versus the short-term (reflective no doubt of global geopolitical disquiet).

Looking to the continent for price signals, carbon (EUA) prices were very volatile yesterday, aggressive buyers in the early morning made the price reach €65/tn, but the rally got sold off as quickly as it rose.

The COT (Commitment of Traders) data came a little bit before 11 A.M. showing a strong decrease in investment funds short position and the auction put another blow to the carbon market, with a cover ratio of 1.24, one of the lowest in 2024 (a cover ratio below one indicates an oversupply of allowances, while a ratio above two indicates strong demand).

The downtrend continued all day, reaching an intraday low of €62.54/tn and closing at €62.6/tn.

UKAs are also very much in a downtrend having dropped below and out of the confirmed triangle pattern, then breaking below the mid-August lows on good bearish volume.

£33.50/tn is now a far-off (but viable target) to the downside marking an area of confluence (historical low plus lower extremity of descending trend channel) – see 30th Sep’s technical chart here.

Fundamentally, the fall in UKAs is being attributed to market participants’ reaction to UK policy review (or the Free Allocation Review).

The outcome being that the expected scarcity of UKAs come 2026 has now been puished back to 2027 – no doubt resulting in speculators reducing long (buy) exposure.

Yesterday’s auction cleared at £34.91/tn.

Our electricity generation mix is bearish in nature today with renewables contributing 35%, thermal at 27% (gas and coal) and low carbon at 19% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £81.949/mwh (or approx. 8.1949p/kwh excluding non-energy).