Markets are taking a breather following days of Trump’s policy announcements.

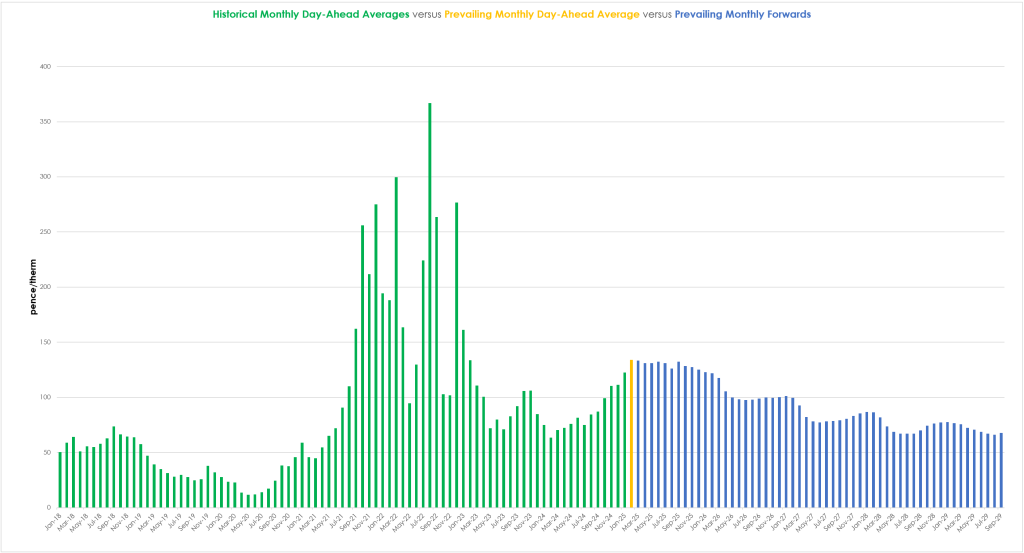

Looking at the big picture, near-term delivery prices rose throughout ‘24 to present, versus prevailing Monthly Forwards which have flattened for Summer-25/Winter-25 delivery, only to die away into ’26 (please see chart below).

This up-and-over price-action reflects the geopolitical disquiet which overshadowed 2024, and the prevailing (wintry) worries over how Europe will successfully replenish gas stocks over the coming months in time for the onset of Winter-25.

But thereafter, prices remain steeply backwardated, with prices at the back of the curve being offered at 50% discount versus the front months – reflecting an underlying market sentiment that risk-premium will abate year-on-year.

Prices closed higher on the day yesterday, driven by flip-flopping weather forecasts reforecasting below seasonal temperatures over the coming week for big swathes of Europe (then remaining that way into the second half of Feb).

Were such a cold snap to actually happen, gas storage withdrawal rates would no doubt increase amid poor renewables output expectations for the same period.

And so today is up too – amid fears over potential supply tightness – such is the bullish inclination of wintry trading/speculating.

Nonetheless, LNG arrivals to Europe/the UK are in good shape and storage is at 51% (just below the middle of the 7-year range).

It’s a little early in the month to say where Monthly Day-Ahead averages are heading – but right now they’re at 133.964p/therm (or approx. 4.571p/kwh excluding non-gas).

ELECTRICITY & CARBON

Not surprisingly, electricity price-action is tracking gas movements.

The forecast of cold, still conditions is pricing-in expectations of increased gas-for-power burn – though wind outputs are expected to improve by the weekend and throughout next week.

However, the back end of February looks to have a significant drop off in the potential for wind powered generation as these drop off well below seasonal norms in most European regions.

On the Carbon markets, the heat has gone out of last week’s UKA rally (fuelled by Starmer’s suggestion that EUAs and UKAs will be merged).

As per our prediction, the bearish divergence on momentum indicators was an early signal for a potential trend reversal.

Prices have dropped away from the upper extremity of the confirmed rising trend channel (please see chart below), but are forming an ascending triangle pattern (a bullish indicator) – let’s see how price deals with another test of triangle support tomorrow.

Today’s UK’s electricity generation mix has been bullish with renewables contributing 23%, thermal at 50% (gas and coal) and low carbon at 12% (nuclear and imports).

Monthly Day-Ahead averages so far for the month are holding steady at £115.123 (or approx. 11.51p/kwh excluding non-energy).