It’s been another quiet week in the markets with the holiday season subduing liquidity.

Nonetheless, prices look to end the week on a bearish note amid solid supply, seasonally low demand, very low storage withdrawals, and steady/sustained storage injections.

European inventories are now at 69% versus the 7-year average of 73% – so fears of missing minimum storage requirements in time for the heating season have all but disappeared (along with the alarmists/bullish speculators/industry charlatans who spent the last 6 months trying to spread panic/talk the price up…)

Asian demand for LNG remains subdued, and vessels continue to enjoy higher profits delivering to European shores (which remains the primary supportive driver in this market – as our prices need to stay high enough so as to continue to attract arrivals to our shores).

If prices fall too far, our ability to replenish storage would be hampered, and prices would then spike accordingly to reflect potential scarcity/supply tightness.

And so, prices continue to meander along in a tight range at the market bottom – with Winter-25 (which has traded within a 20% range since the onset of summer) now retesting the lows we saw at the end of May, and the end of June (90p/therm) – having been as high as 110p/therm at the end of March, and 19th June.

For buyers, this summer has been about hedging on the right side of the trading range – but with 54 days remaining of Summer-25, the trading window grows ever tighter.

Temperatures look set to be above seasonal norms for most of August, wind outputs look ok too – so several more weeks of warm, windy conditions would mean low gas-for-power burn and solid storage injections.

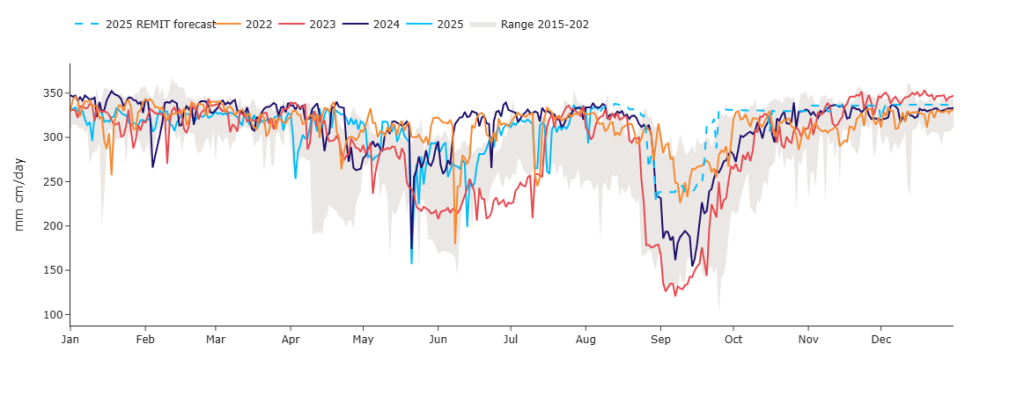

However, we’re about to embark upon Norway’s major annual scheduled outage season which usually lasts for most of September – please see chart below detailing recent history of Norwegian exports to Europe.

And so, pipeline flows to Europe/the UK will drop off significantly for several weeks – as such, prior to September, clients with flexible capability (who still have open volumes for Winter-25) would be wise to implement trading strategies over the coming days/weeks (before conditions tighten at the end of August).

To put Norway’s contribution into context, in 2024, Norwegian exports made up 30% of Europe’s gas imports (for the UK, it was 76%!)

Market participants (those few that aren’t on holiday) continue to keep one eye on the heavily-trailed meeting between Trump and Putin with a view to ending the Ukraine conflict – according to the Kremlin, this will happen in the coming days.

Increasingly, Trump is threatening major trading partners of the US with higher tariffs (primarily India and China) if they continue to do business with Russia – might this pressure finally be forcing Putin to the table?

Suffice as to say if any accord brings about increased Russian gas flows, prices will ‘fall off a cliff’…

Monthly Day-Ahead averages for the month so far are at 80p/therm or 2.7p/kwh (and have been since the start of the month, so very steady near-term risk).

ELECTRICITY & CARBON

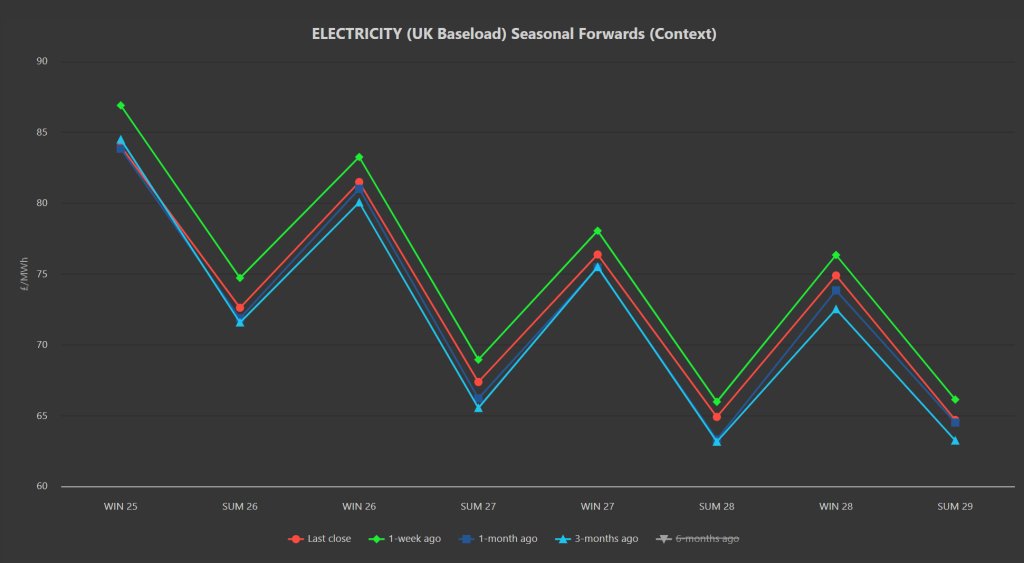

Seasonal Forwards are down on the week, but remain up on 1-month/3-months ago – but only very marginally!

The tightness of the context chart below reflects nicely just how little Seasonal Forwards have shifted since the onset of Summer-25 began (back on 1st April).

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are at £50.18/tn on the mid-price.

Today’s UK electricity generation mix is very bearish in nature – specifically, renewables are contributing 58%, thermal at 7% (gas and coal) and low carbon at 22% (nuclear and imports).

Monthly Day-Ahead averages for the month so far are at £56/mwh or 5.6p/kwh (so, on target to be the lowest month so far this summer, reflecting overhelmingly bearish fundamentals and very low short-term risk).