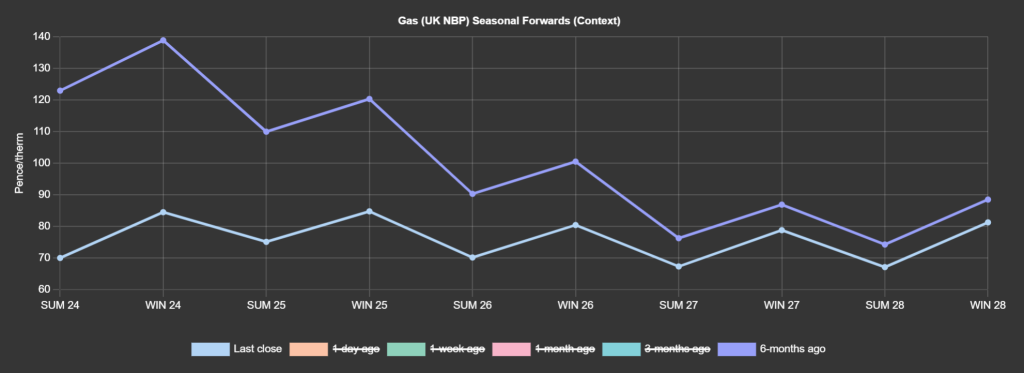

With only 52 days remaining of Winter-23, Summer-24 delivery is now at a 43% reduction versus 6-months ago (see chart).

Markets look poised to finish down on the day.

Key drivers remain unchanged (and overwhelmingly bearish), with European storage at 68% fullness versus the 5-year average of 52%; steady LNG arrivals degasifying at European/UK ports; Norwegian flows back above the 5-day average.

Demand is down d-o-d against a backdrop of improved wind outputs limiting gas-for-power burn.

Near-term temperature forecasts lead us to expect benign conditions over the weekend – thereafter, the long touted February cold spell should hit, and prices will likely be supported accordingly.

Despite ongoing withdrawal from UK reserves, our system opened short this morning – regardless, market participants have shrugged off any bullish momentum in favour of the draw/weight of the overwhelmingly bearish big picture.

Whilst geopolitical risk is stopping the markets from falling off a cliff as summer approaches, the impact of Ukraine and the Red Sea problems on the supply/demand dynamic seem to be limited.

That having been said, consensus anticipates global LNG exports to fall by circa. 10% this month (due to outages at Freeport, Texas and shipping delays caused by vessels avoiding the Red Sea area).

Monthly Day-Ahead averages are on target this month (so far) to achieve 70p/therm (or circa. 2.4p/kwh).

ELECTRICITY & CARBON ALLOWANCES

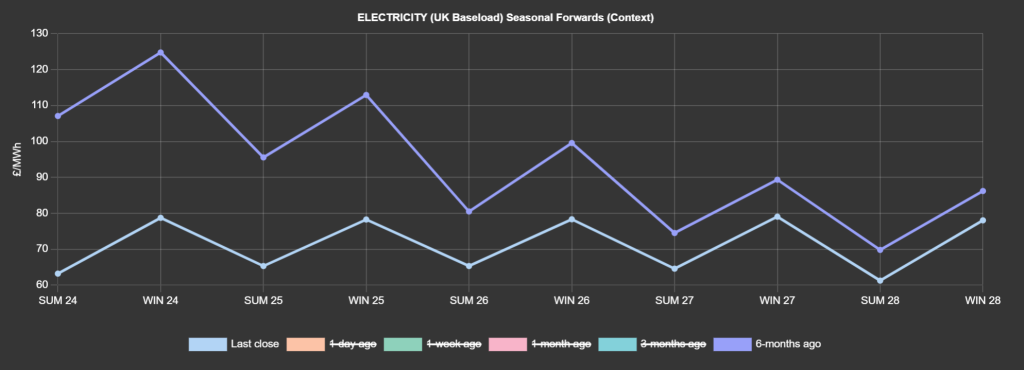

With only 52 days remaining of Winter-23, Summer-24 delivery is now at a 41% reduction versus 6-months ago (see chart).

Looking to the continent, near-term delivery prices were mixed/directionless/balanced yesterday.

Further down the curve, prices were mostly down on the day – tracking the fading gas and carbon markets in an overall retracement of the previous day’s marginal rebound.

The energy market has been trading within a tight range for the past fortnight, driven by daily shifts in weather forecasts.

This morning was no exception, as temperatures for mid-February are once again revised upwards across NW Europe, resulting in a downturn in prices.

The lack of volatility reflects the markets having entered a wait-and-see mode – or a state of equilibrium.

On the carbon markets, the COT (Commitment of Traders Report) did little to move the markets yesterday showing negligible change in speculators’ positions from last week.

Our generation mix today is neutral to bearish again – 40% renewables versus 35% gas-for-power burn.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £56/mwh (or 5.6p/kwh).