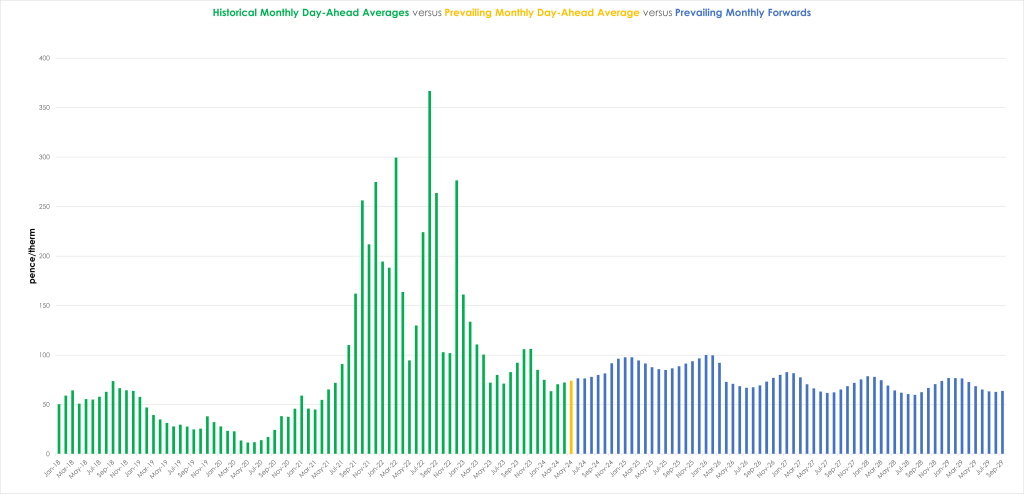

Monthly Forwards for Winter-24/Winter-25 are sitting just below the psychological resistance level of 100p/therm, and are commensurate with achieved Monthly Day-Ahead averages for Winter-23 (see chart).

Markets have been NEUTRAL to BULLISH throughout the week – supported by geopolitical risk (Middle East/Ukraine), pressured by weak demand and increasing temperatures as summer conditions deepen.

Temperatures are above seasonal averages and are expected to stay that way over the weekend.

Whilst demand is weak and below seasonal norms, wind outputs are also weak (increasing reliance on gas-for-power burn) – so there’s not enough in the way of bearish impetus to take the market lower (yet).

Solar outputs are forecast to pick up over the coming days as sunshine looks on the cards.

As such, demand forecast is trailing supply and the UK system is “long” at the time of writing.

On the supply side, the UK is expecting 4 more LNG arrivals to degasify at ports before the end of the month.

Notably, Europe has proposed plans to sanction Russian LNG – further exacerbating supply anxieties.

In short, fundamental developments over the coming days should further relax the market.

Across Europe, several countries have national holidays today – so consumption should be under norms.

Monthly Day-Ahead averages are on target this month to achieve 74p/therm (or circa. 2.4p/kwh).

ELECTRICITY & CARBON

UKAs (UK Mandatory Carbon Allowances) remain in an upward price channel (currently around £38/tn), but have broken above overhanging trend line resitance over the last few days (see chart).

This move is bullish in nature and suggests there’s enough momentum in Carbon to achieve breaks to the topside.

For all heavy emitters, it’s worth noting that falling gas prices ordinarily come with higher emissions values (as gas becomes a more attractive fuel to burn).

Of course, the greater need for thermal generation emits more carbon, so “compliance buyers” are driving the newly found momentum in both European and UK Carbon prices.

Looking to Europe specifically, a continuation next week of cold weather patterns (in certain areas) will likely continue to stimulate price.

Our electricity generation mix is bearish in nature today with renewables contributing 37%, thermal at 17% (gas and coal) and low carbon at 28% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £73/mwh (or 7.3p/kwh).

Notably, Monthly Day-Ahead averages for the month so far are well-above prevailing offers for Month-Ahead (June) at £68/mwh (or 6.8p/kwh).

A confirmation surely that market participants see more risk in Day-Ahead (short-term) than Month/Quarter-Ahead (mid-term).