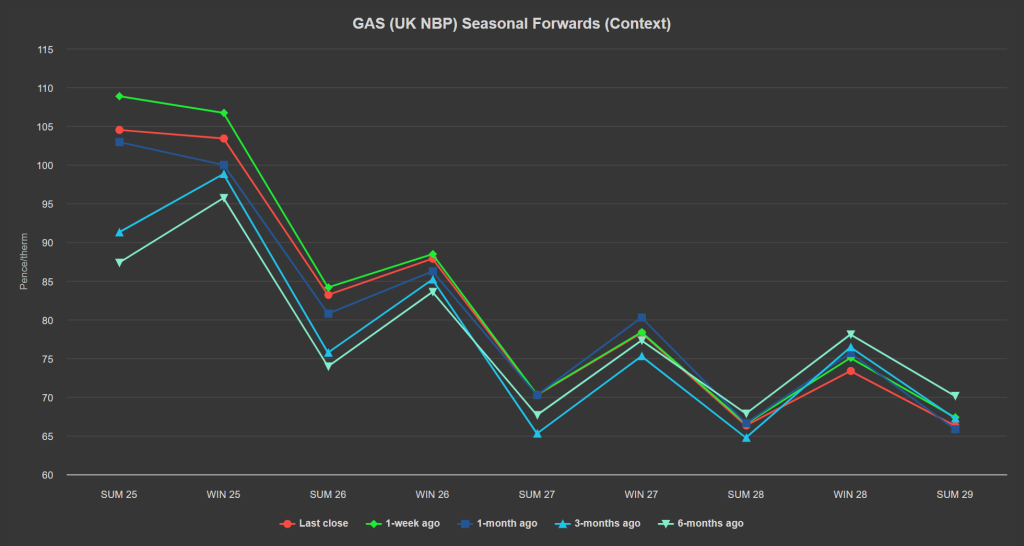

Despite last week’s (arguably overcooked) fears that replenishing European gas storage during Summer-25 (in time for Winter-25) might prove problematic, Summer-25 prices have nonetheless dropped off nicely so far this week.

Whilst Summer-25 remains at a marginal premium to Winter-25 (as it has been for over a month now), the difference has narrowed to 1p/therm (equivalent to 0.03p/kwh) – see chart below.

Notably, in a rare/significant concession last week, President Putin issued a decree dropping the requirement to use Gazprombank for European gas payments.

This triggered a downward correction in gas prices, particularly Summer-25 – as seemingly conciliatory behaviour on the part of Russia can only be a good thing where supply is concerned.

To start the week, bearish momentum continued off the back of milder weather forecasts (which seem to be flip-flopping on a daily basis).

Geopolitical developments in Syria had little or no impact – instead market participants reacted to weaker demand expectations for heating in the second half of December.

Selling interests for some spot LNG cargoes from Chinese importers probably played into bearish sentiment as well – reflecting lowering Chinese demand/preference for coal.

In addition, US LNG netbacks (a measure of the export parity price that a gas supplier can expect to receive for exporting its gas) continue to favour Europe as a premium destination compared to Asia (although the spread is marginal).

Down the curve (longer-term delivery), prices have slipped too – the weak booking at auction for Summer-25 European storage capacity is also likely weighing on market sentiment (as further evidence of low demand forecasts).

In short, as we pointed out last week, it’s not panic stations yet – prevailing conditions, whilst wintry, are not too bad.

European storage fullness is at 82% versus the 5-year average of 81% (so withdrawals have slowed).

So far this month, Monthly Day-Ahead averages are on target to achieve 115.873p/therm (or approx. 3.954p/kwh excluding non-gas).

ELECTRICITY & CARBON

Summer-25 electricity has enjoyed some decent drop off this week – at £81.20/mwh (or 8.12p/kwh), down on the week and the month.

On the Carbon markets, UKAs (UK Allowances) are back on the slide on low volumes (see chart below) – having broken below the lows of 7th Oct-24, with a retest of the all-time lows of £31.30/tn printed on 29th Jan-24 now in the offing.

At the time of writing, UKA mid-price is at £34.59 – so very welcome comparative value back on the table for Compliance buyers.

The UK’s electricity generation mix is bullish in nature today with renewables contributing 23%, thermal at 51% (gas and coal) and low carbon at 18% (nuclear and imports).

Monthly Day-Ahead averages for the month so far are on target to achieve £101.037/mwh (or 10.10p/kwh excluding non-energy).