Markets remain supported by geopolitical impacts as Ukraine’s incursion into Russian territory continues into a 6th day.

Yesterday saw Winter-24 intraday prices up at 117p/therm off the back of fears that Sudzha gas transit via Ukraine into Western Europe could be halted (further diminishing European supply security with Winter-24 now only 50 days away).

Both sides have now confirmed they have no intentions to halt gas flows via the Sudzha pipeline, which has thankfully taken the heat out the bullish reaction to front-end prices.

Tensions in the Middle East remain heightened prompting a flurry of international diplomacy encouraging Iran to exercise restraint.

For their part, Iran’s response has been to reject Western calls not to carry-out a retaliatory strike against Israel (as such, fears of supply disruption persist).

The long-touted hot spell in the UK is upon us with temperatures reaching 35 degrees in some parts yesterday.

Accordingly, total demand is at 153million cubic metres today, 47mcm below seasonal normal, with the system 9mcm long at this morning’s open (supply outstripping demand forecast).

Week-on-week, the number of LNG tankers on European waters waiting for available terminals at which to degasify has climbed to just under 10% reflecting sluggish “summery” demand.

Whilst Norwegian pipeline flows remain at the upper extremity of a 10-year range, the Kollsnes plant is undergoing unscheduled maintenance (which is temporarily reducing delivery to the UK/NW Europe).

Over the course of Summer-24 so far, demand has remained low against a backdrop of comfortable supply/storage – as such, replenishing gas stocks has not posed any problems.

Europe remains on track to achieve 100% storage fullness levels by Winter-24 (early Oct ’24) with inventories currently at 88% versus the 5-year average of 78%.

On the hedging side, we’re now on the other side of Summer-24 – with 134 days having elapsed, and 50 remaining.

Clients with open volumes for Winter-24 are now in the minority – with most having opted to close-out Positions given the ongoing geopolitical uncertainties and with winter conditions now on the horizon.

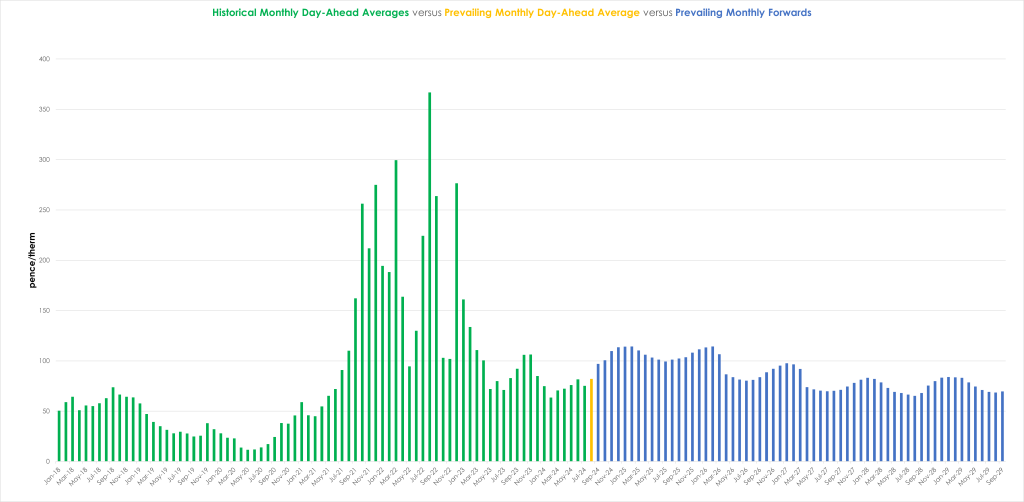

Monthly Day-Ahead averages so far this month are on target to achieve 82p/therm (or circa. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

Whilst Day-Ahead remained fairly steady yesterday (reflecting benign near-term conditions, notwithstanding Ukraine’s incursion into Russia), all other Forward periods of delivery are mirroring the bullish gas rally.

On the Carbon markets, EUA prices remain at a premium to UKAs, with EUAs now consolidating in a tight range at the top of last week’s bullish rally.

UKAs continue to fall (as indicated by the daily timeframe RSI divergence and confirmed descending trend channels) – now trading at circa. £38/tn (see chart).

At the time of writing, our electricity generation mix is very bearish (and “summery”) in nature today with renewables contributing 52%, thermal at 7% (gas and coal) and low carbon at 27% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £63/mwh (or circa. 6.3p/kwh excluding non-energy).