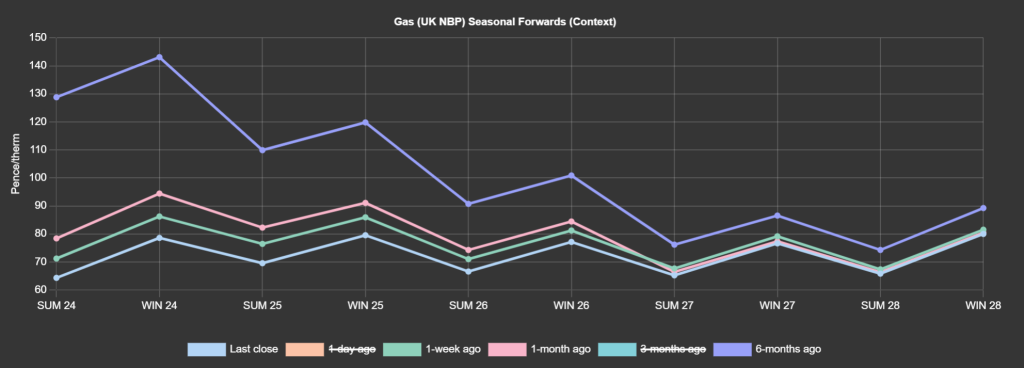

Prices are down versus 1-week/1-month/6-months ago (see chart).

At the time of writing prices are soft with good liquidity – so a retest of the lows printed back in early June ’23 looks increasingly likely.

Key drivers are overwhelmingly bearish – with temperatures above seasonal norms, strong supply, weak demand, limited withdrawals, high European storage (67% versus 5-year average of 61%) and steady LNG arrivals (five more vessels are expected to degasify at UK ports this month).

Whilst geopolitical risk is stopping the markets from falling off a cliff, the impacts of Ukraine and Red Sea LNG transit problems on the supply/demand dynamic are evidently limited.

Monthly Day-Ahead averages are on target this month (so far) to achieve 69p/therm (or circa. 2.35p/kwh).

With Summer-24 only forty-eight days away, a significant portion of clients have already started scaling-in hedges for the front seasons.

ELECTRICITY & CARBON ALLOWANCES

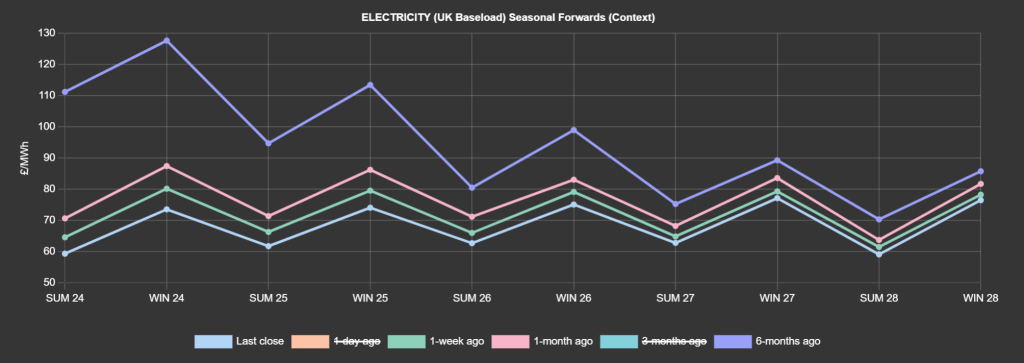

Looking to the continent, European near-term delivery prices edged lower in anticipation of a slight uptick in renewables outputs.

Prices are expected to post further losses today against a backdrop of rising temperatures, improved solar and wind production and French nuclear availability (as of tomorrow).

Down the curve, seasonal forwards are extending their downward trend mirroring the ongoing decline in gas and carbon values.

On the regulation side, the French Energy and Industry Minister plans to delay energy reform law and update the ARENH rate until “the end of the year” (ARENH mechanism will entitle suppliers to purchase electricity generated by nuclear power plants at a regulated price).

EUAs (European carbon allowances) steadily declined over the first session of the week led by coal-to-gas switching and anticipation of weak industrial activity, eclipsing the unplanned outages at two French nuclear reactors.

It remains very difficult to estimate a floor price for carbon at the moment, with both speculators and compliance players (Industrials) waiting for sign of a slowdown in the fall to take profits or start stocking allowances for future surrender whilst the going’s good!

Back in the UK, our generation mix is neutral with renewables contributing 29% and gas-for-power burn at 42%.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £60/mwh (or 6p/kwh).