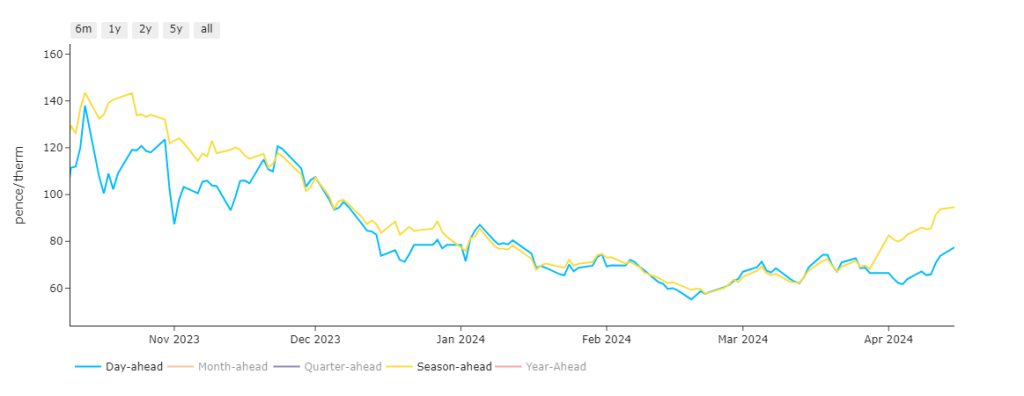

Until the onset of Summer-24 ((beginning 1st April), Day-Ahead and Season-Ahead have been at parity since Nov ’23 (see chart).

However, as of this week, Season-Ahead (Winter-24) is now at a circa. 20% premium to Day-Ahead.

As we’ve been stating for the past few months, the only drivers that will move this market higher are geopolitical.

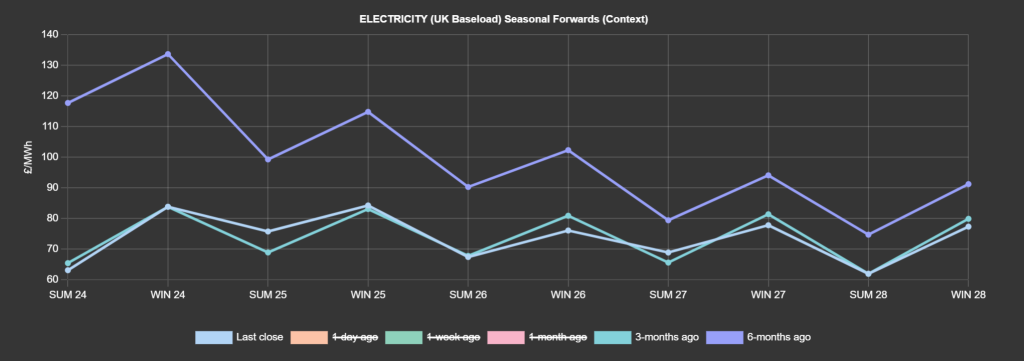

Notwithstanding historically high gas storages and the onset of summer conditioning, fears of supply tightness are driving prices to levels higher than those printed 3-months ago (all the way down the curve).

Starting yesterday morning, prices opened lower than Friday’s close and it seemed for a couple of hours that global energy disruptions were contained to what would happen next with Israel and Iran.

The UK and Europe source very little gas from the region but the gas market is global – and since the impacts of Russia’s reduced gas flows beginning ’22, any reduction of gas availability impacts ALL markets.

Context-wise, in Feb ’24 our gas prices fell to the lowest levels we’ve seen since early ’21 – this in turn has led China and Asia to increase their LNG imports giving rise to higher premiums.

Notably, in Feb/Mar ’24, exports to China climbed by around 16% y-o-y – whereas exports to Europe fell by the same number!

Amid significant escalations in Middle East tensions over the weekend, last week’s Russian attacks threatening the viability of Ukrainian transit routes into Western Europe, unscheduled maintenance at Freeport LNG (Texas), and an unplanned outage at Nyhamna resulting in significant reductions to Norwegian pipeline flows, bullish momentum has found some legs – with momentum indicators all pushing into positive territory.

Geopolitical events look likely to continue to be the main driver of price for the rest of the week – though colder weather (increasing withdrawals for heating demand) and weaker wind generation expected toward the weekend are also fuelling bullish fervour.

Market participants are still weighing-up next steps in the Middle East after Israeli officials confirmed that Israel would be responding to Iran’s drone attacks…

Lest we forget (amid all the fear and avarice), European inventories are at 62% fullness versus the 5-year average of 44%.

For this week however, bullish market signals are undeniably dominant.

Monthly Day-Ahead averages are on target this month to achieve 69p/therm (or 2.35p/kwh).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices are showing marked regional divergence (France is cheap off the back of renewables outputs, Germany is expensive off the back of low temperatures and very poor renewables outputs).

On the carbon markets, prices traded sideways yesterday, starting a correction from their recent bullish run in the first hour of trading but quickly reversed and gave back the losses throughout the remainder of the day.

The early decrease seemed driven by reduced tensions in the Middle East following Iran’s weaker-than-expected attack on Israel.

However, the afternoon’s gains were attributed once again to the soaring gas markets amid recent unplanned outages at US LNG freeport and an extension of the maintenance at Nyhamna.

Despite the still comfortable supply and stock levels, the gas markets are continuing the bullish rally this morning – taking with them the power and emissions prices.

Technically speaking, most contracts are in overbought territory and a downward correction may be on the cards if /when geopolitical sabre-rattling subsides.

Back in the UK, Dec-24 contracts for UKAs are circa. £36/tn.

Our electricity generation mix is very bearish in nature today with renewables contributing 58%, thermal at 5% (gas and coal) and low carbon at 23% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £41/mwh (or 4.1p/kwh).