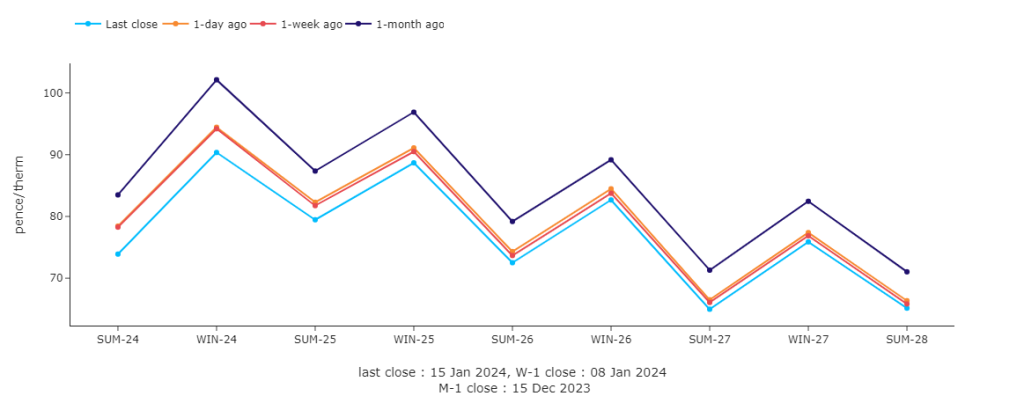

Gas markets are down on the Day/Week/Month (see chart).

The curve remains steeply backwardated (near-term delivery prices at a significant premium to far-term delivery prices).

Prices were soft and down at this morning’s open, notwithstanding the cold snap (and the associated increase in heating demand/gas-for-power burn).

Despite demand being above seasonal norms, the UK system is marginally long at the time of writing (supply outstripping demand).

Whilst it’s undeniably chilly and still right now, the impacts of the weather outlook remain bearish given that Feb is expected to be wet and windy (and the prevailing cold snap should abate by the weekend).

On the supply side, Norwegian flows are strong and volumes of LNG imports into Europe have risen by more than 10% week-on-week.

The risk of escalations in the Middle East continue to temper bearish momentum – though LNG is doggedly making its way toward Europe via the Cape of Good Hope (avoiding the Suez Canal but adding 10 days to voyage durations).

Competition for LNG from Asia remains muted, with Japanese demand on the floor and the disruption of Chinese New Year just around the corner (10th Feb ’24).

Back in the UK, monthly Day-Ahead averages are on target this month to achieve 81p/therm (or 2.75p/kwh).

ELECTRICITY & CARBON ALLOWANCES

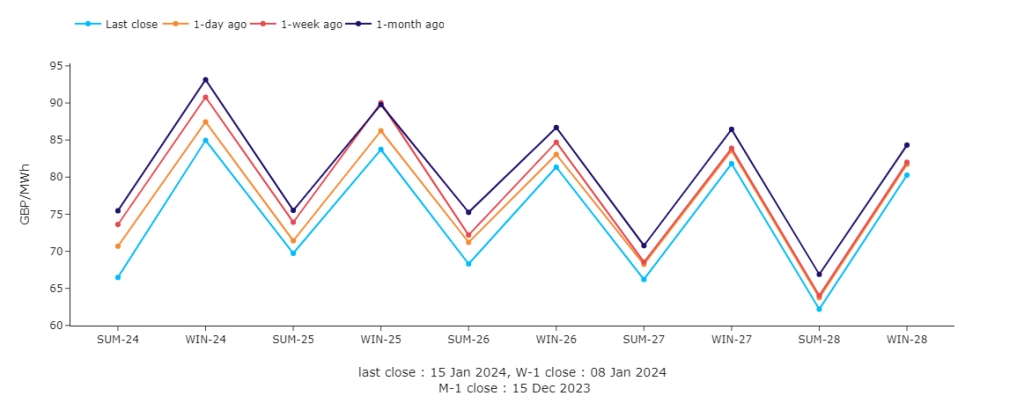

Electricity markets are significantly less backwardated than gas (with only a 4% difference between Winter-24 and Winter-28 delivery prices – see chart).

Looking to the continent for signals, European short-term delivery prices enjoyed support yesterday as expected from lingering cold, still conditions.

Down the curve, Forward prices posted moderate losses pressured by yet another milder revision of temperature forecasts by month end.

Historically high gas/hydro stocks against a backdrop of increasing French nuclear availability is keeping a lid on any upside caused by heightened risks of LNG transit via the Red Sea.

Yesterday marked the resumption of European carbon auctions, with the first sale of the year clearing 2-cents above the secondary market, and UKAs closing at £34/tonne looking set to test the lows of Dec ’23.

Back in the UK, our generation mix at the time of writing is bullish in tone with 58% fossil fuels (including 4% coal); 29% renewables; 5% nuclear.

Monthly Day-Ahead averages are on target this month to achieve £79/mwh (or 7.9p/kwh).