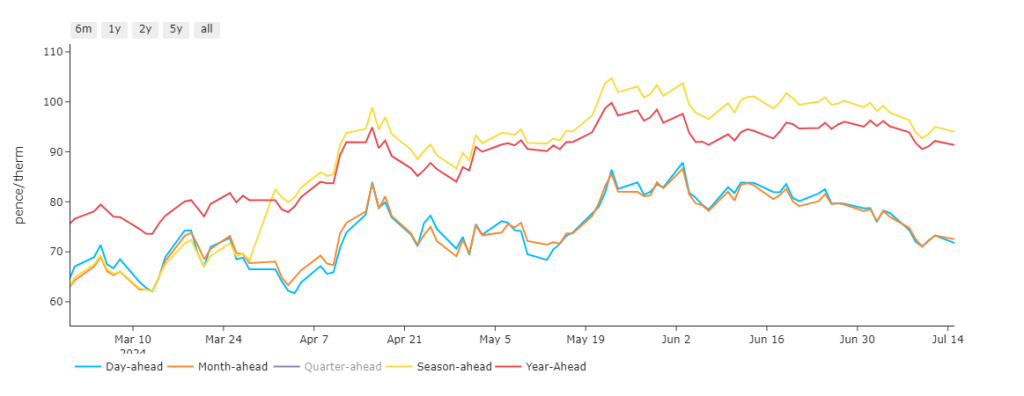

As Summer-24 deepens, beginning mid-June, Day/Month-Ahead prices have fallen away from Season/Year-Ahead – reflecting a “summery” discount to near-term delivery (see chart).

Nonetheless, prices opened slightly up on yesterdays close off the back of flip-flopping, mixed weather forecasts for the coming fortnight – with temperatures now expected to climb above the seasonal norms this weekend but then falling back below seasonal norms thereafter.

Of course, lower temperatures will likely increase gas-for-power burn to accommodate heating demand.

However, wind outputs whilst expected to remain below seasonal norms this week will likely climb above seasonal norms into next week – mitigating the impact of temperature falls (and the associated reliance on thermal generation).

The UK opened long this morning (supply outstripping demand forecast).

Prevailing demand remains below seasonal norms.

Prices down the curve are a little higher this morning, with cooling demand rising in response to the heatwave being enjoyed/endured across large swathes of Europe – will the UK be next?

Well, the South of England is forecast to hit high temperatures in the next couple of days.

Freeport terminal (Texas) continues to export reduced volumes of LNG, as repairs on the facility continue apace following damage caused by Hurricane Beryl.

All in all, solid injections and high European storage (81% versus the 5-year average of 70%) coupled with steady Norwegian flows continues to apply bearish pressure to a market exhibiting mild summery qualities.

With demand low, and supply comfortable, replenishing gas stocks is not posing any problems.

On the hedging side, we’re now on the other side of Summer-24 – with 107 days having elapsed, and 77 remaining.

Clients with open volumes for Winter-24 are increasingly scaling-in so as to avoid any loss of prevailing value.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24) – though LNG delivery remains tight against a backdrop of sustained high temperatures across Asia (and the associated cooling demand).

Monthly Day-Ahead averages so far this month are on target to achieve 75p/therm (or circa. 2.55p/kwh excluding non-gas).

ELECTRICITY & CARBON

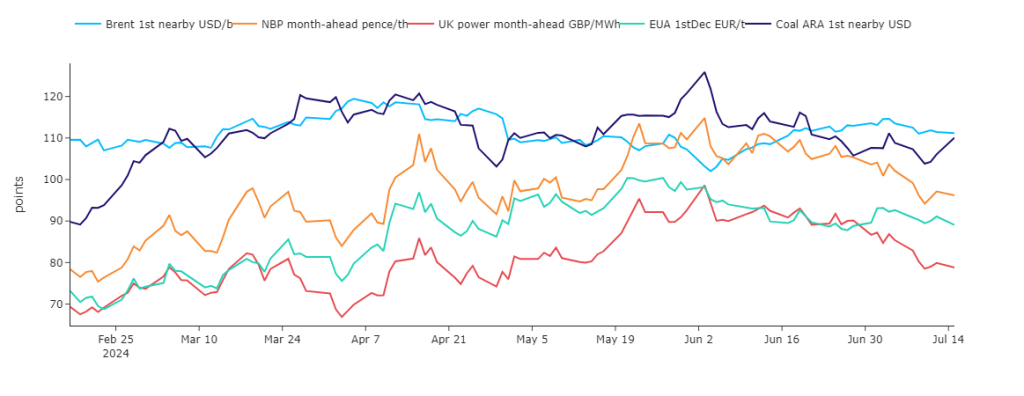

Electricity (and gas) are enjoying comparative summer decreases relative to a basket of other UK commodities (see chart).

Looking to the continent, near-term delivery prices are likely to be pressured by high solar and wind outputs – especially during daytime hours.

Though generators are slowly adapting their bidding behavior to be more price sensitive – by limiting the negative impacts of oversupplying the grid.

The weather outlook indicates an unstable pattern driven by Atlantic ridges and low pressure systems, leading to fluctuating temperatures and wind conditions across Europe, with a brief warming trend expected over the weekend.

Renewable energy generation is likely to be affected by these weather patterns, with wind forecasts showing short-term increases followed by calmer conditions, while solar generation remains unstable and hydro potential is expected to decrease due to limited precipitation in the Alps.

A significant heatwave is being felt across Europe, ranging from the Balkans to the Black Sea.

Demand is therefore sharply up, stimulated by cooling requirement – the consequence is very high prices for the evening ramp (when solar is not producing but the need to cool down the scorching heat is still present).

On the Carbon markets, EUAs (European Carbon Allowances) declined yesterday in line with gas markets – the Dec ’24 benchmark contract closed at €67.64/t after losing -2.24% on the day.

Back in the UK, UKAs (UK Carbon Allowances) followed our prediction that prices were due to fall (as indicated by RSI divergence) – now trading at circa. £41/tonne.

Prices are now in a confirmed ascending trend channel testing the lower extremity – with £40/tn as a strong area of support to the downside, £45/tn as strong area of resistance to the upside.

Our electricity generation mix is neutral in nature today with renewables contributing 29%, thermal at 31% (gas and coal) and low carbon at 28% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £66/mwh (or circa. 6.6p/kwh excluding non-energy).