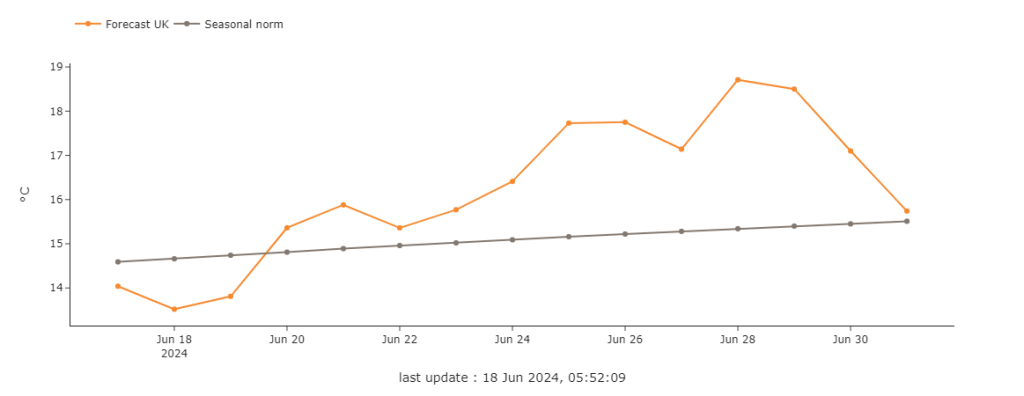

Markets have dropped off last week’s mini bull-rally, and temperatures next week are forecast to rise above seasonal norms (see chart).

The LNG outlook is also marginally improved – weirdly, Russia has overtaken the US as Europe’s leading gas supplier (notwithstanding several EU nations lobbying for sanctions).

Following Russia’s invasion of Ukraine back in Feb ’22, Europe became significantly dependent on US LNG, which then supplied 20% of the region in 2023.

According to the most recent figures, LNG from the US has now fallen to 14% of Europe’s overall supply, whilst Russian exports (gas and LNG) made up 15%.

W-o-w, global LNG supply is little changed.

Notably however, we’ve seen a 15% weekly increase of LNG cargoes at sea for 20 days or longer – due primarily to vessels being forced to navigate around the Cape of Good Hope to avoid Houthi rebels in the Red Sea area.

Whilst India LNG imports remain at historic highs, China LNG imports thankfully slowed significantly compared to May – mitigating global supply tightness (and keeping a lid on the commodity price).

Back in the UK, our system was long at this morning’s open (supply outstripping demand forecast).

Supply/demand dynamics are stable with exports to Europe reducing d-o-d.

We’re 79 days into Summer-24 (105 days remaining).

Fundamental drivers have softened from last week allowing for decent storage injections.

Norwegian flows are increasingly stable, and the single-day maintenance at Skarv today should see flows rise again tomorrow.

Overall, bullish drivers look weak, and as long as the geo-political landscape remains “quiet” (!), the trajectory will be one of sideways/bearish price action.

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices remained at equilibrium yesterday with prospects of soaring French nuclear availability and hydro generation at odds with forecasts of weakening wind output.

Down the curve, prices dropped sharply to start the week – pressured by weaker EUAs (European Carbon Allowances) and falling gas prices against a backdrop of steady Norwegian gas flows and slowing LNG imports into Asia.

But again (as has been the case for weeks now), the benchmark TTF month-ahead contract (European gas) appeared to find support at its 1-year moving average, potentially indicating market caution in committing to a more meaningful retracement (or trend reversal).

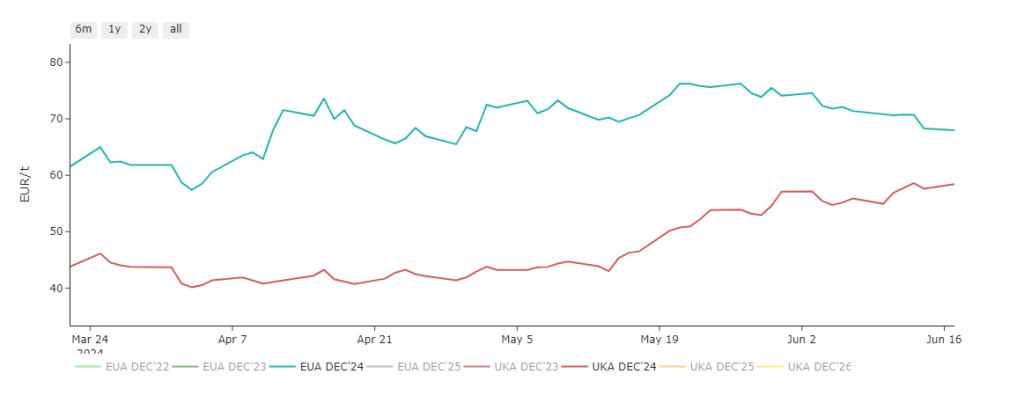

On the Carbon markets, the EAU downtrend took a breather yesterday – though with UKAs (UK Allowances) still drifting northwards headed seemingly to test £50/tonne, the two markets grow ever closer to parity (see chart).

Our electricity generation mix is neutral in nature today with renewables contributing 27%, thermal at 31% (gas and coal) and low carbon at 29% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £69/mwh (or 6.9p/kwh excluding non-energy).