Warmer, windier conditions are keeping a lid on any bullish momentum – with the onset of Summer-25 now only 13 days away.

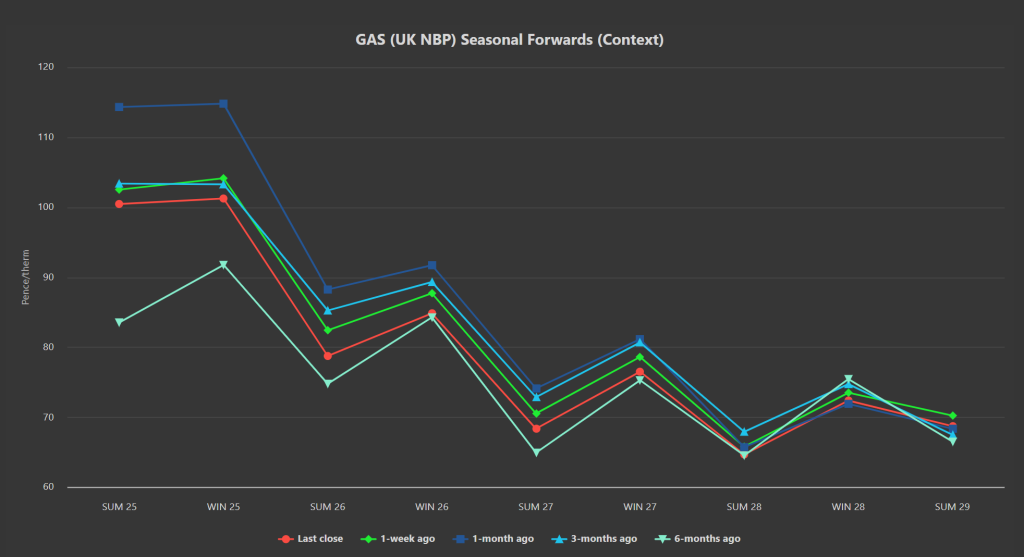

Seasonal Forwards are down on the week, month, and 3-months ago – but still up versus 6-months ago (please see chart below and at https://icdenergymanagers.com/charts/).

Summer-25 remains at a discount to Winter-25 (just!), reflecting a sustained confidence amongst participants that replenishing stocks over the course of Summer-25 is do-able.

The UK system opened short this morning (demand forecast outstripping supply) amid unscheduled outages at Asgard (taking some Norwegian pipeline capacity offline).

LNG arrivals are steady, mitigating the impacts of storage still being on the low side (35% versus the 5-year average of 44%).

Markets are consolidating ahead of today’s (much publicised) phone call between Trump and Putin – though Trump has indicated his intention to discuss “land and assets” with his Russian counterpart…

Germany continues to reject any suggestion that Russian gas may soon be heading their way via Nordstream (lending support to European prices so as to continue to attract LNG cargoes away from Asia).

Resurgent tensions are taking hold in the Middle East with Israel resuming its bombardment of an already flattened Gaza – as such, concerns over Red Sea gas transit are resurfacing (following last week’s US attacks on Houthi rebels).

All in all, markets are balanced and rangebound pending further geopolitical developments – if Russia’s flows resume, prices will inevitably fall.

Talk of a minerals deal between the US and Ukraine has dropped out of the headlines for the time being – it seems likely Trump will want to make a deal with Putin before US companies establish mining operations across Ukraine.

It seems very unlikely that neither Trump nor Putin would risk publicising their talks were it not their intention to announce an agreement at the end of it – whatever form that may take.

Otherwise, Trump will be left with egg on his face and Putin’s opportunity to exit the mess (that is the Ukraine invasion) will have passed him by (with the Russian economy looking increasingly shaky).

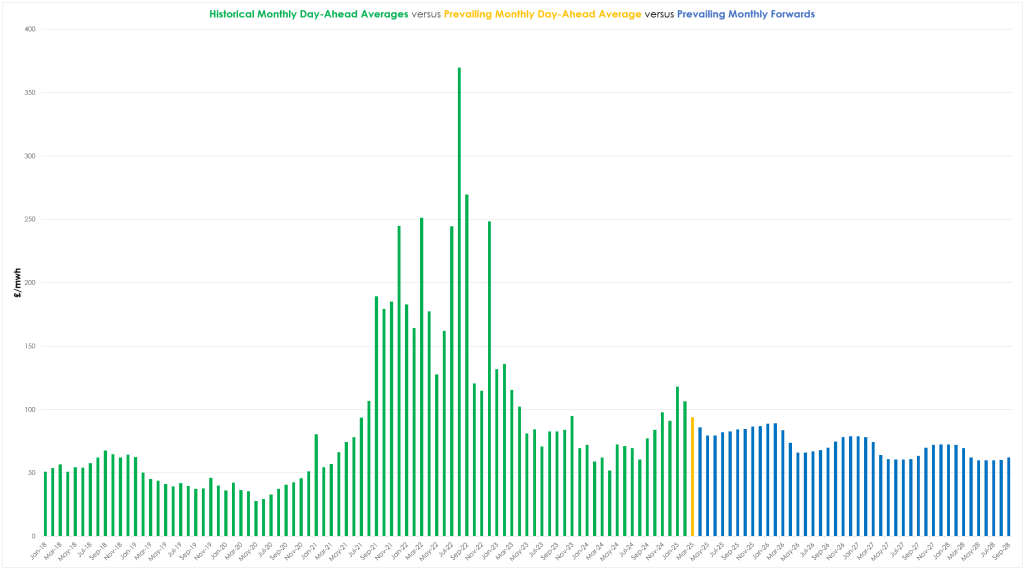

Monthly Day-Ahead averages for this month so far are on track to improve on last month’s final number (124p/therm), with averages at 103p/therm at the time of writing (or approx. 3.5p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity is tracking gas south, with some increasingly attractive prices on offer for summers down the curve.

This month’s prevailing Day-Ahead Average is at a premium versus Monthly Forwards – reflecting lower mid-term risk with summer approaching (please see chart below).

Looking at UK mandatory Carbon allowances for heavy emitters (UKAs), the Dec-25 benchmark is observing a rising trend channel with mid-prices now at £45.71/tn.

Technically speaking, bearish RSI divergence is pointing toward limited upside momentum amid low volume (and overbought stochastics) – so not a lot of conviction in the drift northwards.

UK electricity Monthly Day-Ahead averages so far for this month are back below £100/mwh and sliding – now at £94/mwh (or approx. 9.4p/kwh excluding non-energy).