With only 12 days of Winter-23 remaining, prices have been on a sustained uptick for the last few days.

At the time of writing, near-term delivery (Day/Month/Quarter/Season-Ahead) is up more than 10% versus last Wednesday.

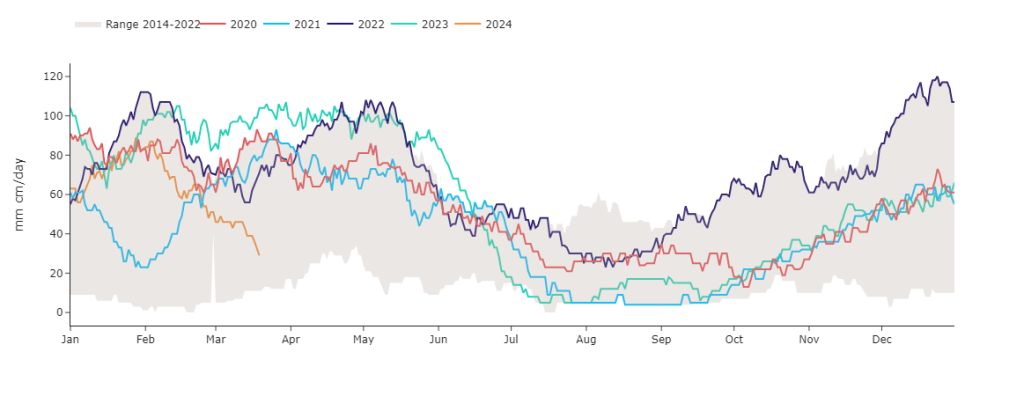

The key drivers contributing to this late winter rally are unscheduled Norwegian outages (reducing flows by circa 7.5mcm/day); revised forecasts of lower temperatures across the UK and Europe for the rest of the week; and ongoing weak LNG arrivals to the UK (and the associated low send-out – see chart).

So, why are LNG imports dropping off?

Well, sendout last week dipped to its lowest level since October 2023 – likely off the back of muted demand and steady pipeline imports.

Gas consumption is significantly down versus this time last year (more than 30%).

And so, low sendout is likely a reflection of this muted demand, coupled with continuous imports along the UK’s interconnector pipelines since early March — the highest number of consecutive importing days since 2022.

Regasification could remain muted over the coming week, as milder temperatures and stronger wind generation continue to weigh on gas demand – as such, only a few LNG carriers have declared for arrival at UK terminals before month-end.

Temperatures are expected to return quickly back above seasonal norms in time for the weekend – reducing heating demand and weakening price support.

In short, notwithstanding the relatively strong volatility we’ve seen over the past days, the upward move feels unsustainable (considering the persisting weak demand and Europe’s historically high gas stocks).

Even the lower temperatures expected in the coming days should be mostly offset by healthy renewables outputs – once again limiting gas withdrawals.

Monthly Day-Ahead averages are on target this month to achieve 68p/therm (or 2.3p/kwh).

ELECTRICITY & CARBON

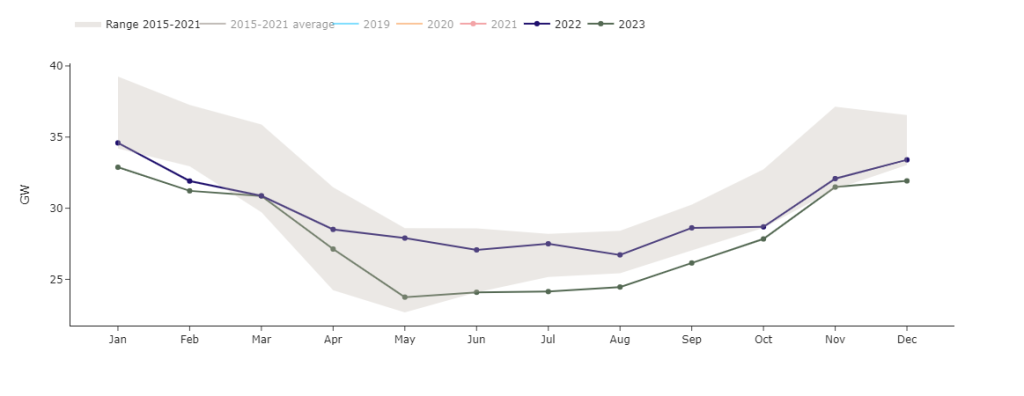

As further evidence of weak demand, monthly UK average power load is printing significant lows versus the last 10 years (see chart).

Looking to the continent, near-term delivery prices remain steady in anticipation of rising solar generation and temperatures (offsetting forecasts of slightly weaker wind output and French nuclear generation combined with higher gas/emissions prices).

On the carbon markets, prices started the week on a bullish note, lifted by the upward momentum of buoyant gas prices amid tighter supply dynamics and forecasts of temporary colder weather for early next week.

Carbon’s rise so far this week is attributable almost entirely to the gas market driving the rest of the energy complex, with higher prices inevitably favoring a higher-emitting coal-based thermal generation.

The fundamental picture is however still unsupportive of a sustained bull run and a correction is expected to materialize with the developing onset of summer conditioning.

Nonetheless, beware of further gains in carbon prices as numerous short positions of investors are seen above 65 €/t and a rise above that level will of course trigger another round of short-squeezing that will be short lived but spiky!

Back in the UK, UKAs are in and around £40/tn – the prevailing range at £45/tn to the topside (and £30/tn to the downside).

Today, our electricity generation mix is bullish in nature with renewables contributing 15%, thermal at 51% (gas and coal) and low carbon at 21% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £65/mwh (or 6.5p/kwh).