The bears are strengthening their grip on gas prices as we embark upon the other side of Summer-25 (Q3 delivery period begins today).

The absence of bullish geopolitical drivers (for now) against a backdrop of benign weather conditions has brought prices back down to levels last seen prior to the US dropping bombs on Iran’s nuclear facilities.

Month-Ahead prices (now at 79p/therm) have enjoyed seven straight days of consecutive losses.

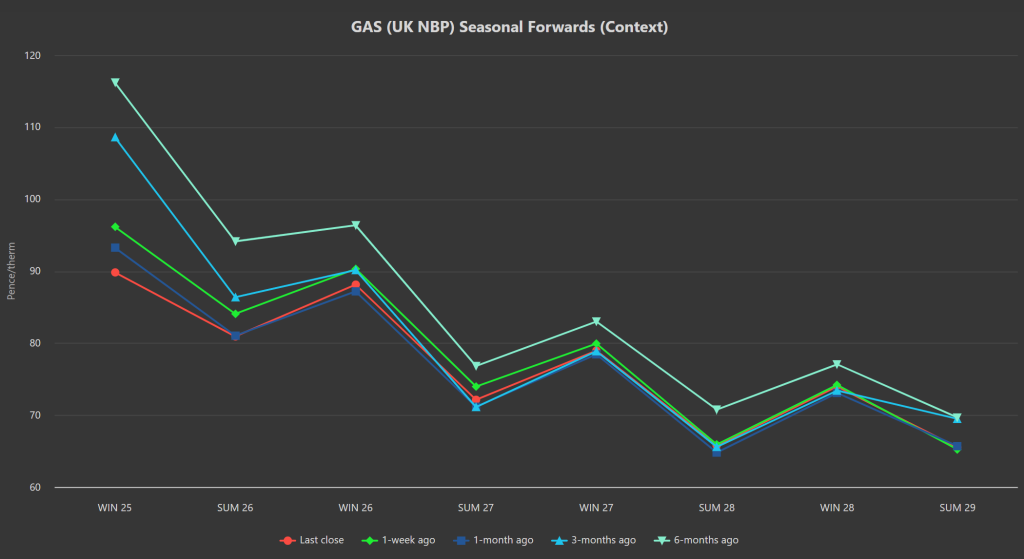

Winter-25 delivery is at 91p/therm (down 19% versus 110p/therm printed on 19th Jun).

Right now, markets are treading water amid poorer wind outputs and higher gas-for-power burn than we’ve seen so far this week – so we’re unlikely to see any more efforts by the bears to take the markets lower until maybe Thursday (when wind outputs are forecast to improve coinciding with falling temperatures across Europe, limiting cooling demand).

Nonetheless, for FLEX buyers out there, it’s worth noting we are in a dip and front-end Seasonal Forwards are down versus 1-week/1-month/3-months/6-months ago – so value is very much on offer (please see chart below).

Looking at the big picture, Asian demand remains subdued (limiting competition for cargoes); the first LNG Canada cargo is headed to South Korea (improving supply dynamics); oil prices continue to drift lower (limiting gas demand); and European storage fullness is at 59% versus the 5-year average of 65% (so only 10% off the pace).

June’s Monthly Day-Ahead average came in at 86.333p/therm (or approx 2.95p/kwh excluding non-gas).

ELECTRICITY & CARBON

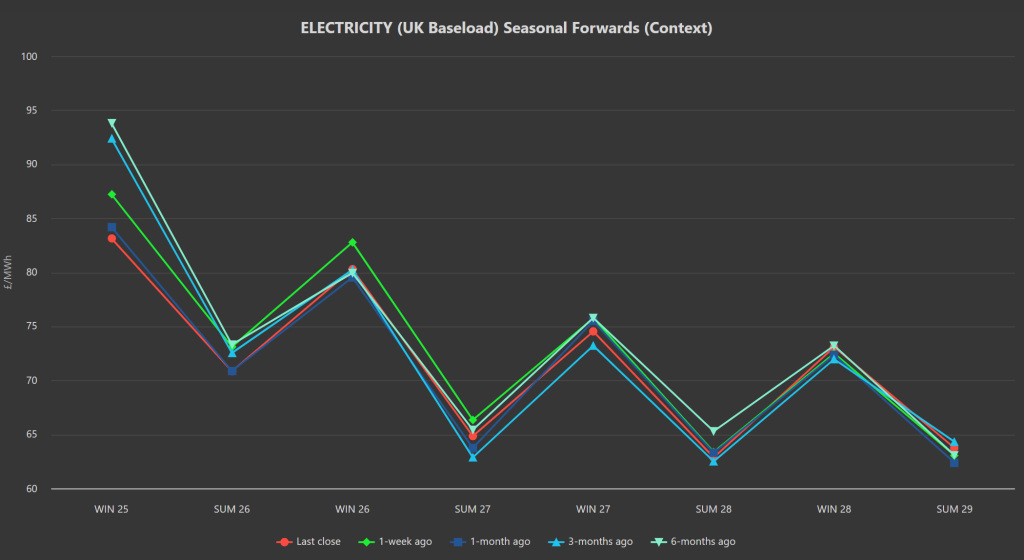

Electricity prices have also enjoyed a week of sliding prices.

Winter-25 is at £82/mwh (last printed 30th May) – so down 19% versus the highs of 19th Jun.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

As such, prices have dropped steeply in line with European/UK gas falls.

At the time of writing, Dec ’25 UKA benchmark prices are at £46.55/tn on the mid-price (a drop of 15% versus 13th Jun) – next meaningful area of support is £44/tn but rumour has it that significant BUY orders are building at £45/tn – so a prudent trade would be a BUY entry at £45.50/tn (so as to not miss the opportunity to get in).

Today’s UK electricity generation mix is neutral in nature reflecting benign ‘summery’ weather conditions, limiting gas-for-power burn – specifically, renewables are contributing 24%, thermal at 36% (gas and coal) and low carbon at 31% (nuclear and imports).

June’s Monthly Day-Ahead average came in at £66.963/mwh (or approx 6.7p/kwh excluding non-energy).