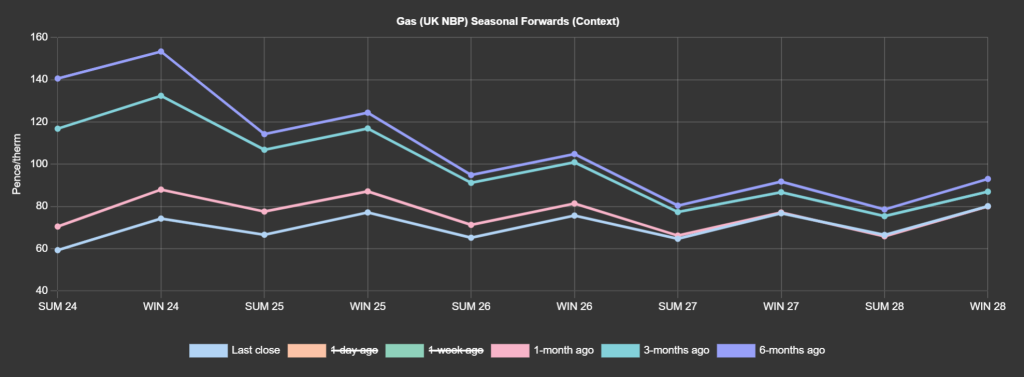

Summer-24 delivery is now at a 58% discount versus 6-months ago! (see chart)

Near-term delivery prices continue to soften amid overwhelmingly bearish fundamentals.

Day-Ahead fell as low as 55p/therm yesterday – its lowest level since 1 November 2022.

Notwithstanding any unforeseen geo-political impacts, expect more of the same this week before residential heating demand picks up due to colder temperatures by the weekend.

Until then, the UK’s Day-Ahead discount versus TTF (Europe’s benchmark gas exchange) is likely to remain wide enough to continue incentivizing IUK (interconnector) exports to the Continent.

Ample supply and historically high storage makes any potential upside risk to near-term delivery prices limited.

In short, the bear-trend that began in Q422 is still in place.

With Summer-24 only 40 days away, only geo-political unrest poses any risk to a continuation of the prevailing bear trend.

Monthly Day-Ahead averages are on target this month (so far) to achieve 65p/therm (or circa. 2.2p/kwh).

ELECTRICITY & CARBON ALLOWANCES

Looking to the continent, demand should remain contained over the next week as temperatures remain above long-term averages across Europe.

Thereafter, temperatures fall toward the end of the month and into early March potentially triggering a late rebound of winter demand before Summer-24 officially begins on 1st April.

On the supply side, strong wind outputs are forecast by Thursday of this week – limiting gas-for-power generation.

However, this wind event will quickly fade, and lower outputs are expected for the weekend and early next week.

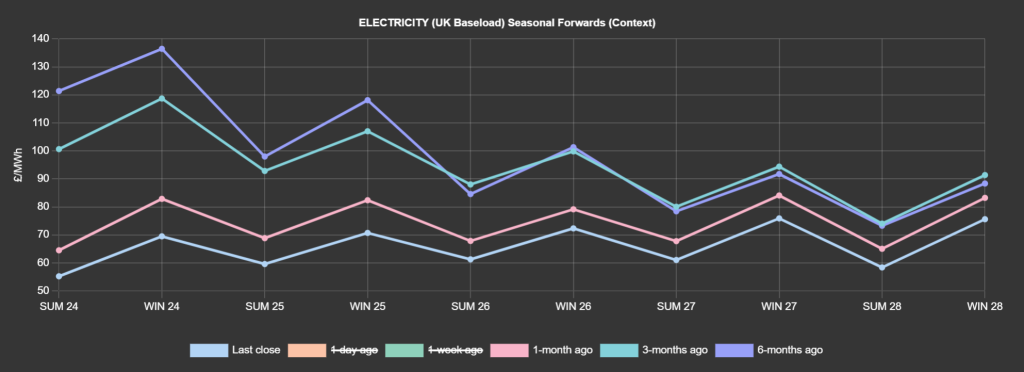

Down the curve, prices extend their slide, tracking falls in the fuel basket, primarily driven by falling carbon values.

EUAs have fallen to a 2-year low reaching €52.90/tonne before closing at €53.54/tonne.

UKAs followed suit dropping to £33/tonne, looking likely to test the lows of late Jan ’24 (£30/tonne).

These drops in UK/European carbon are being driven by warm weather (limiting thermal generation) and low gas to coal switching potential (due to declining gas forward prices).

Back in the UK, our generation mix is bearish with renewables contributing 46% and gas-for-power burn at 23%.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £60/mwh (or 6p/kwh).