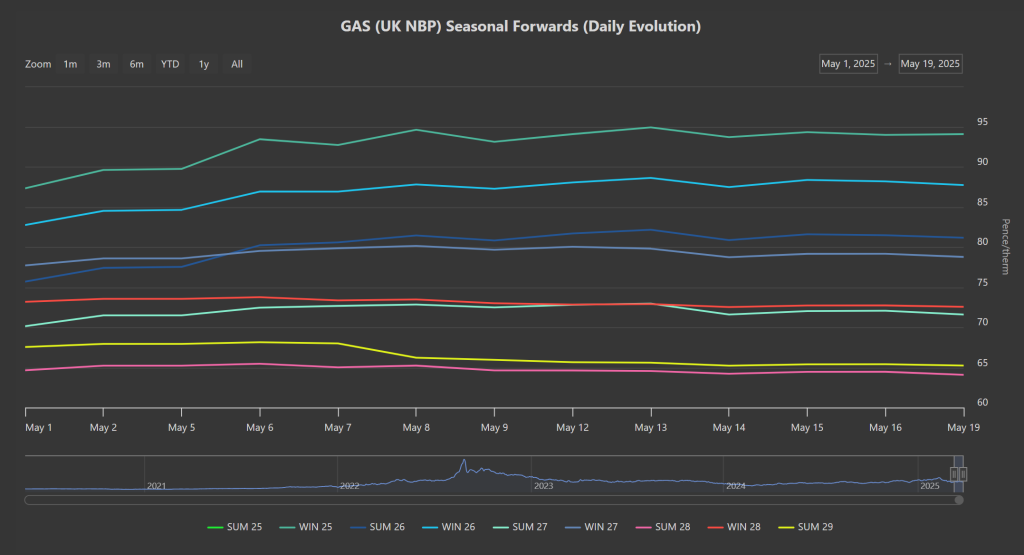

Markets have been trading water, with prices all the way down the curve little changed week-on-week (please see Seasonal Forwards chart below).

Nonetheless, from a risk-management POV, Trump’s announcement that the US is walking away from the Ukraine-Russia peace talks gives us cause for concern.

Having spoken with Putin yesterday, Trump declared that Ukraine (and Europe) will need to contend with Russia’s aggression on their own.

He then went on to say that Russia will likely be subject to further sanctions if they don’t play ball.

As such, the resumption of Russian flows back into the European system during 2025 looks off the table.

Today’s markets are slowly baking-in this realisation, with prices all the way down the curve firming as the afternoon progresses.

Norwegian flows have also fallen back below the 5-day moving average given unscheduled maintenance at Kollsnes taking much needed capacities offline.

US Treasury Secretary, Scott Besent, is quoted as having said that tariffs will likely to return to pre-pause levels if negotiating countries don’t act in good faith.

Accordingly, disquiet amongst market participants is contributing to volatility – though reduced global trade will likely have a bearish impact on gas prices (given the inevitable industrial demand destruction).

The storage injection season continues apace, with European levels now at 45% versus the 5-year average of 52%.

Thankfully, China (historically the world’s largest Asian LNG buyer by volume), is enduring sustained weak demand and so competition for cargoes is mitigated (on top of the fact that delivering to Europe/the UK is more profitable than delivering to Asia given comparative gas values).

It’s worth noting however, that the Indian government has now invoked emergency measures instructing companies to operate underutilized gas-fired power plants at higher capacity beginning 26th May to 30th June so as to meet forecasted electricity demand across the sub-continent.

By way of background, gas-fired Indian power plants have been more expensive to run than those generating off coal, solar and wind – the inevitable outcome being 60% of India’s gas-fired power stations sitting idle.

With India back in the LNG market, European gas prices will need to stay high to continue to attract cargoes (so as to achieve continued storage injections).

All in all, there’s an undeniably bullish tone to the markets today – whilst prices have yet to react too acutely, the prospect of zero resolution to the Ukraine-Russia conflcit will inevitably reintroduce risk-premium all the way down the curve.

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst the going’s good.

This month’s UK gas Day-Ahead averages are holding steady at 80p/therm (or approx. 2.7p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity remains tethered to gas movements (as you’d expect given the UK’s ongoing reliance on gas-for-power generation).

As such, Winter-25 is printing £88/mwh at the time of writing (up nearly 10% versus the recent lows on 1st May).

On the Carbon side of things, yesterday the UK and EU formally agreed to work towards linking their Emissions Trading Systems.

The accord was announced at the EU-UK summit in London, citing aims to “create a level playing field” and “improve energy security” (the link would also mean the UK will avoid being hit by the EU’s carbon tax due to come in next year, potentially saving £800 mn…).

Not surprisingly, given that EUAs remain at a premium to UKAs, this announcement has been price supportive of UKAs as the two markets approach price parity in anticipation of the market merge.

Heavy-emitters across the UK will be disappointed to see this tax back up above £50/tn – currently printing at £54.94, and most definitely back in a bull-run (please see chart below showing trend observing ascending price channel).

Nonetheless, today’s UK electricity generation mix is bearish in nature reflecting solid renewables outputs – specifically, renewables are contributing 38%, thermal at 18% (gas and coal) and low carbon at 17% (nuclear and imports).

So far this month, electricity Day-Ahead averages are back on the rise – currently at £75/mwh (or approx. 7.5p/kwh excluding non-energy).

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst the going’s good.