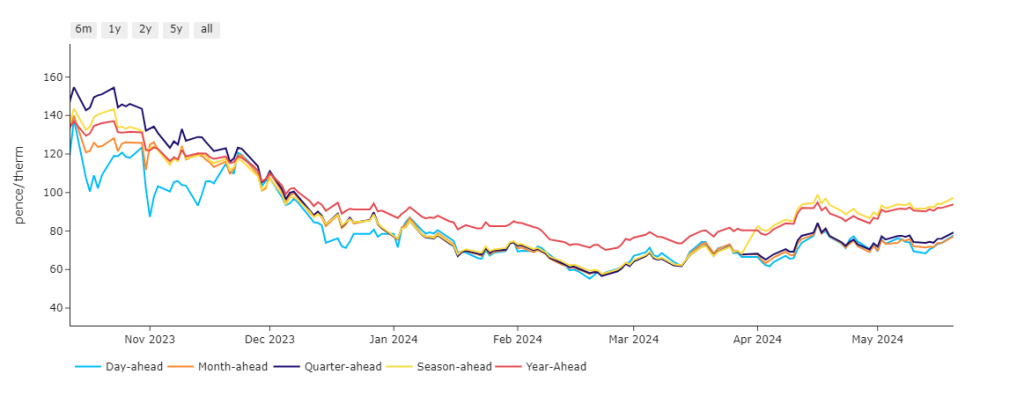

Following the unprecedented volatility of ’22/’23, all near-term delivery periods converged to parity in Dec ’23 (see chart).

Thereafter, beginning Jan ’24, Year-Ahead prices were at a premium until the onset of Summer-24 (beginning Apr ’24).

At which point, Season-Ahead (Winter-24) surpassed Year-Ahead prices, and remains at a premium to date.

Notably, the divergence between prompt delivery (Day/Month/Quarter-Ahead) and mid-term delivery (Season/Year-Ahead) yawns ever wider.

This of course reflects very low risk for delivery over the summer months, and an inflated risk-premium for delivery at and beyond Oct ’24.

It was a bullish open this morning, off the back of weak wind outputs and the market pricing-in the impacts of Norwegian outages.

Flows from Norway to the UK/Europe fell well below the 5-day moving average to 180 million cubic metres/day (with Langeled pipeline at only half of Monday’s volumes).

Temperatures are set to cool down at the back end of this week though longer term forecasts detail a more settled outlook.

Despite rumours of EU sanctions on Russian LNG, Russia’s gas production levels actually increased by 8% in the first 4 months of 2024!

According to some analysts, China will increase their gas imports to 50% of demand by 2035 – a 10% increase from current import levels.

This assumes of course that China’s exports continue to grow, which in turn relies on the West’s willingness to take Chinese output – not a foregone conclusion.

Consensus is mixed over where price is headed next, with many seeing the recent uptrend as repositioning rather than long-term trend impetus given the still comfortable fundamentals.

Markets are neutral to bullish – geopolitical support remains at odds with seasonal pressure (falling demand/solid supply/less reliance on withdrawals etc).

Monthly Day-Ahead averages are on target this month to achieve 72p/therm (or circa. 2.45p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices have been surging due to an acute rise in demand following Monday’s holiday coupled with a drop in solar outputs.

On the Carbon markets, emissions posted significant gains in the early part of the week buoyed by the rally in gas prices.

The recent strength of EUAs (European Carbon Allowances) is impressive but seemingly inconsistent with the fundamental picture considering the still low demand for allowances and high supply expected over the coming year.

As such, many market participants believe the market is in a “wait and see” mode, leaving daily trading to speculators with very short-term strategies.

Volatility is likely to continue over the coming weeks pending developments on the demand side.

Back in the UK, UKAs (UK Allowances) are trading at circa. £43/tn (Dec-24 benchmark) – having broken above the highs printed on 25th Mar ’24 and now challenging overhanging trend lines (see chart).

Our electricity generation mix was bullish in nature today with renewables contributing 9%, thermal at 43% (gas and coal) and low carbon at 28% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £71/mwh (or 7.1p/kwh excluding non-energy).