European storage fullness has made it to 65% versus the 5-year average of 71% (with another 70-days to go before the onset of Winter-25).

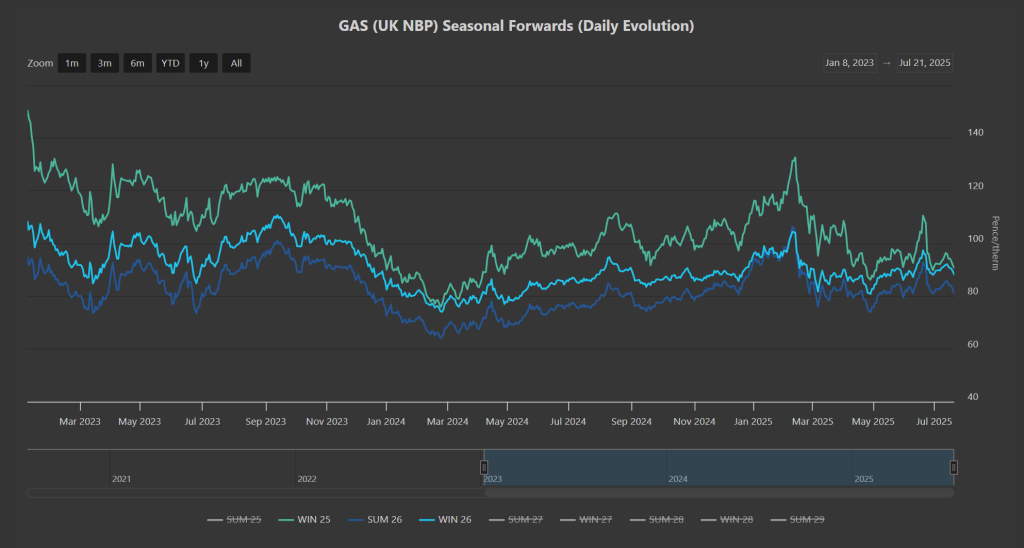

The front-seasons (Winter-25;Summer-26;Winter-26) are at the bottom of the trading range – so a nice dip for any Winter-25 buyers (please see chart below).

The tariff deadline of 1st August draws ever closer – rumours abound that the EU is planning retaliatory tariffs if the US plays hardball.

Gas traders will be eyeing the potential impacts of an impasse – Europe’s economic reliance on exports would surely mean that falling trade would result in demand destruction.

Whilst US LNG cargoes are still making more money by heading to Europe over Asia, market participants continue to eye cautiously the impacts of Asian temperatures (and the corresponding cooling demand).

Back in the UK, monthly Day-Ahead averages for the month so far are at 81p/therm (or approx 2.77p/kwh excluding non-gas).

ELECTRICITY & CARBON

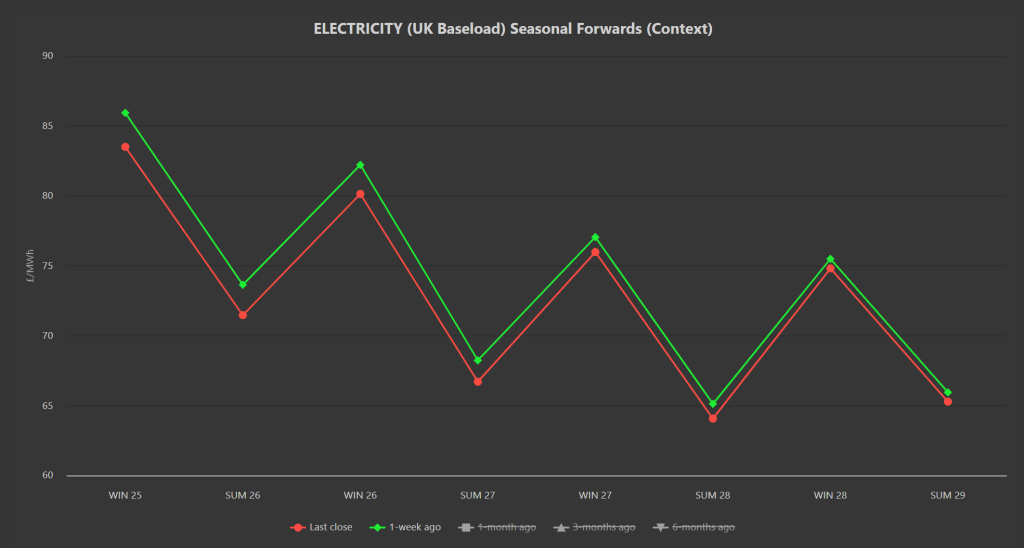

Seasonal Forward prices are down on the week all the way down the curve (please see chart below).

Winter-25 has drifted below £84/mwh at the time of writing.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are at £48.70/tn on the mid-price.

Today’s UK electricity generation mix is neutral in nature – specifically, renewables are contributing 29%, thermal at 27% (gas and coal) and low carbon at 30% (nuclear and imports).

Monthly Day-Ahead averages for the month are at £78/mwh (or approx 7.8p/kwh excluding non-energy).