As predicted toward the end of last week, prices are unwinding off the back of reduced posturing between Israel and Iran.

Both near- and far-term delivery contracts are down amid renewed confidence that Europe has ample storage fullness to withstand the rigours of geopolitical disquiet and the remnants of winter temperatures.

Despite cold temperatures last week, European inventories are still over 60% versus the 5-year average of 40%.

Following over a week of almost zero outputs, Freeport LNG’s production is now on the up – though still nowhere near normal levels.

Thankfully, Saturday saw the first arrival at Freeport for 11 days of an LNG vessel docking for liquefaction.

Whilst Norwegian flows are back near capacity following extended unscheduled maintenance over the past few weeks, several scheduled outages remain on the docket across Norwegian production fields – with the heavier impacts starting tomorrow.

Due to recent high demand (amid the cold spell), withdrawals from MRS (mid-range storage) will be needed this week – though LNG sendout is expected to ramp-up beginning today.

In short, whilst geopolitical tensions have subsided, fundamental key drivers are a little bullish today with forecasts looking chilly and Norwegian maintenances set to cause some tightness on the supply side.

The 15-day forecast is detailing colder temperatures from 23rd to 27th April.

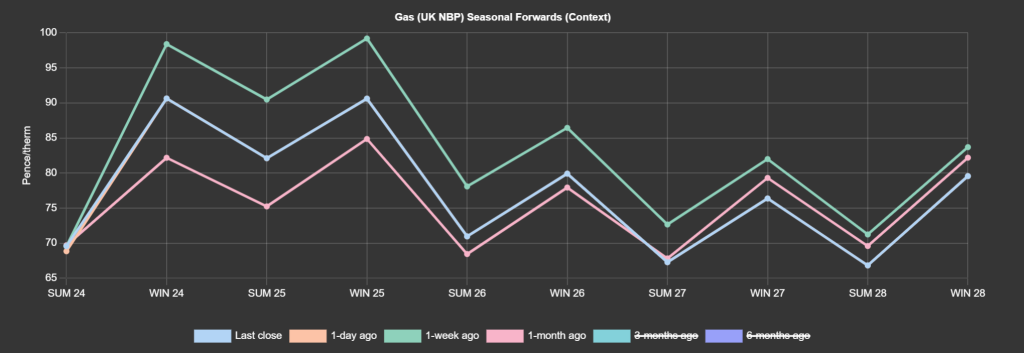

Monthly Day-Ahead averages are on target this month to achieve 72p/therm (or 2.4p/kwh).

ELECTRICITY & CARBON

Looking to the continent, European short-term delivery prices stayed bullish yesterday amid cold temperatures and anticipated shortage of wind outputs.

Prices may ease today as weather forecasts suggest a slight increase in temperatures and improved renewables outputs.

Carbon fell back yesterday, driven down by softening gas prices amid fading hysteria over Middle East sabre-rattling.

The bearish signal from the gas market is likely pushing speculators in the EU ETS to build back short positions – so expect more of the same so long as the heat stays out of gas contracts.

On the weather side, whilst the cold spell is offering support to prompt (near-term delivery) electricity prices, warmer temperatures combined with stronger solar generation are being forecast for next week – which will weigh on the energy complex and fuel the downtrend in Forward prices.

Back in the UK, Dec-24 contracts for UK ETS are circa. £36/tn.

Our electricity generation mix is a little bullish in nature today with renewables contributing 23%, thermal at 35% (gas and coal) and low carbon at 26% (nuclear and imports).

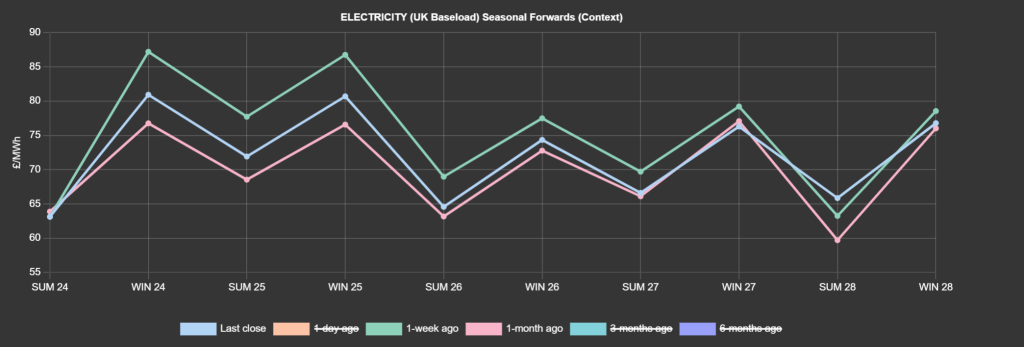

Monthly Day-Ahead averages are on target this month to achieve £51/mwh (or 5.1p/kwh).