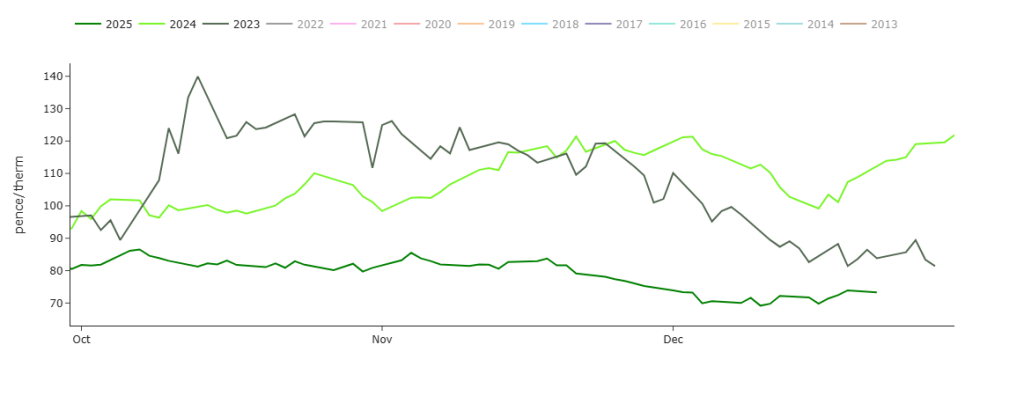

Whilst Month-Ahead delivery prices have found a little support this week, prices throughout ’25 have seen significantly lower volatility than ’23/’24 – please see chart below.

Yesterday, prices across Europe traded marginally down ahead of higher than expected temperatures easing demand forecasts, and mitigating the rate of withdrawals.

Meanwhile, in the UK, temperatures are forecast to drop back around 1°C – so around seasonal norms.

Looking ahead to the Christmas break, the continent will be chilly with temperatures dropping as far as 6°C below seasonal norms across certain parts.

As such, increased heating demand will inevitably support European prices, whilst UK prices should remain flat in-line with more stable temperatures.

On the LNG side of things, after what started as a cold winter in the US (which prompted premature concerns of LNG export levels and associated price spikes), we’ve now seen US temperatures turn mild resulting in near record levels of export!

This, of course, bodes well for continued strong supply to European markets as we navigate the winter months.

Continued US LNG supply is crucial to continued low prices as Europe slowly withdraws its storage levels which are now at 67% (versus the 5-year average of 74%).

In other news, China has announced a 143% y-o-y increase in Russian LNG imports.

Last month, Russian LNG made up 23.5% of China’s total LNG imports—this is more than double the 11% share seen this time last year.

Back in the UK, Monthly Day-Ahead averages for December are holding steady at 70p/therm (or 2.4p/kwh exc. non-gas).

ELECTRICITY & CARBON

Notably, Seasonal delivery prices all the way down the curve are up on the week, and the month.

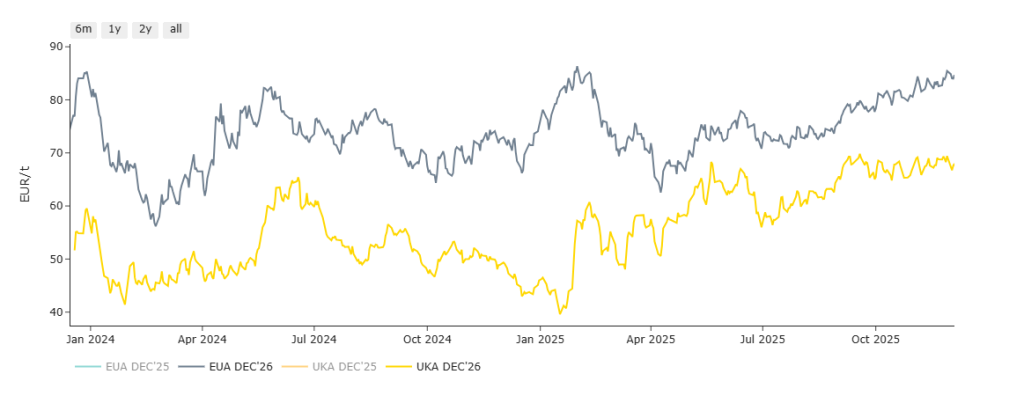

On the Carbon side of things, UKAs went as low as £55.10 on the mid-price on 10th Dec ’25 – their lowest level since late-Oct ’25 – however, last week marked the end of the Dec-25 delivery product and so traders managed to keep prices high until expiry on 15th.

Thereafter, markets have “gapped-up” to reflect the Dec-26 delivery product – though spot prices on the secondary market remain at a £2/tn discount.

UKAs remain at a 20% discount to EUAs – please see comparison chart below.

Today’s UK electricity generation mix is neutral in nature, so neither bullish nor bearish – specifically, renewables are contributing 36%, thermal at 30% (gas and coal) and low carbon at 20% (nuclear and imports).

Monthly Day-Ahead averages for December so far are holding steady at £73/mwh (or 7.3p/kwh exc. non-energy).