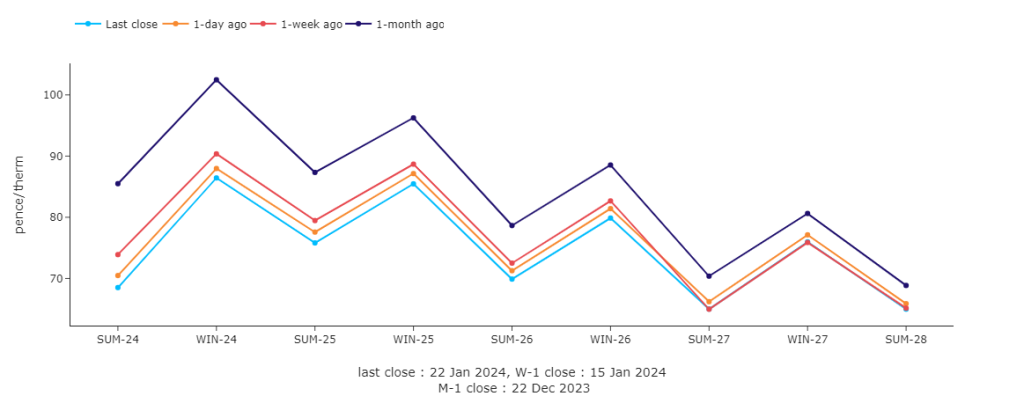

Seasonal Forwards are little changed versus 1-Day/1-Week ago (see chart).

Near-term delivery prices at this morning’s open were unchanged versus yesterday’s close with the market consolidating recent losses off the back of a long UK system (supply outstripping demand).

Prevailing storms (Isha and Jocelyn) are keeping wind outputs way above seasonal norms.

Temperatures are forecast to be 5 degrees on average above seasonal norms for the rest of the week.

Not surprisingly, LNG arrivals have been prevented from degasifying at UK ports due to high seas.

Geo-political risk persists in the form of Middle East escalations and lingering worries over supply disruption in the Red Sea/Suez Canal.

Monthly Day-Ahead averages are on target this month to achieve 79p/therm (or 2.7p/kwh

ELECTRICITY & CARBON ALLOWANCES

Looking to the continent, European near-term delivery prices are trading sideways – still heavily pressured by healthy wind outputs and temperatures above seasonal norms.

Down the curve, prices fell yesterday mirroring the gas and carbon markets driven down by anticipation of warmer and windier weather for the remainder of the month and likely over the beginning of February.

Temperatures are indeed expected to linger between 2 and 5°C above long-term averages in the upcoming two weeks, while another wind surge (although weaker than the current one) is forecasted for early-February.

The limited withdrawals from hydro ad gas stocks are reducing the risk of supply shortage for both this winter and the next one, fueling sustained bearish momentum.

The carbon prices continued to track the gas prices’ decline and hit an 18-month low mid-afternoon before slightly rebounding at the end of the session.

While the overall demand from the power generation and industrial sectors remain weak due to bearish weather prospects and bleak macroeconomic context, establishing a definitive floor for carbon prices is tricky.

However, a discernible sentiment is emerging, hinting at the likelihood of a forthcoming consolidation fueled by speculators nearing the peak of their short positions, the current low emissions prices enticing opportunistic buyers, and a collective perception within the industry that the worst of the crisis is now in the rearview mirror.

Back in the UK, consensus is building that UKAs (UK Carbon Allowances) may settle as low £30/tonne this week at tomorrow’s auction.

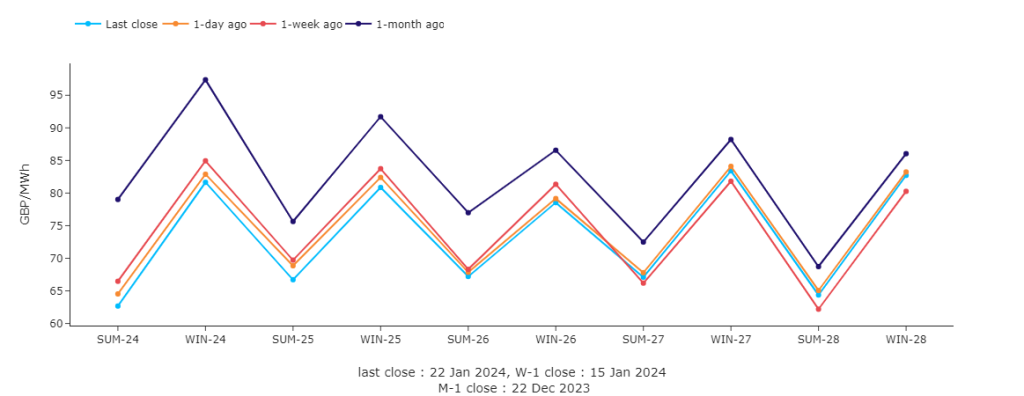

UK electricity monthly Day-Ahead averages are on target this month to achieve £75/mwh (or 7.5p/kwh).