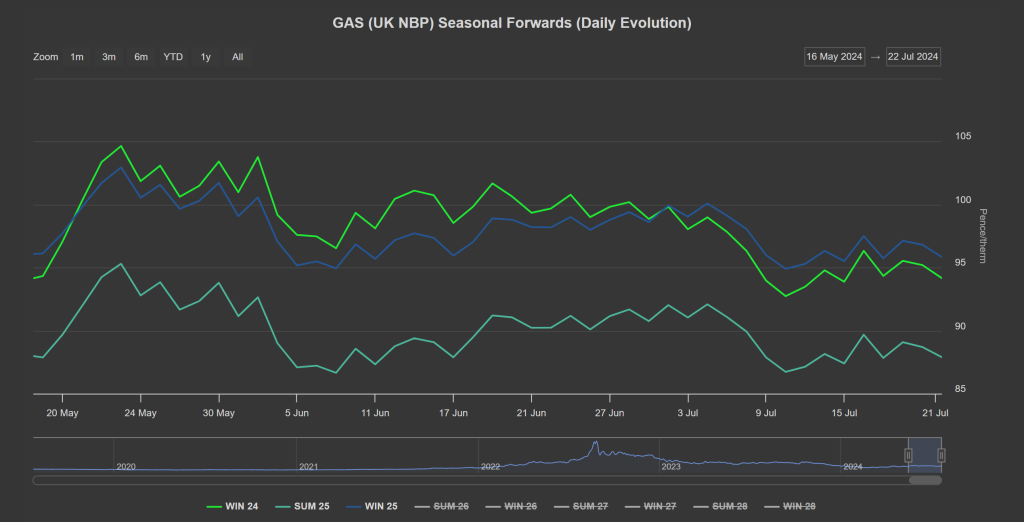

The front 3 seasons have dropped approx. 10p/therm over the last 2 months reflecting tight, neutral to bearish trading conditions – see chart below and at https://icdenergymanagers.com/charts/

Price action remains neutral to bearish off the back of high storage, solid supply, weak demand, and positive news that cargos out of Freeport LNG terminal are picking up after Hurricane Beryl forced a shut down earlier this month.

The UK system opened short today (demand forecast outstripping supply) – but only very marginally.

With a welcome hiatus in scheduled summer maintenance, Norwegian flows into the UK are sitting at capacity.

LNG send-out is on the floor, with only one arrival to the UK expected in the next couple of weeks.

Down the curve, longer term delivery contracts have been meandering sideways – with neither bulls nor bears having sufficient momentum to move the market.

Looking at the big picture, solid injections and high European storage (83% versus the 5-year average of 72%) coupled with steady Norwegian flows continues to apply bearish pressure to a market exhibiting mild summery qualities.

With demand low, and supply comfortable, replenishing gas stocks is not posing any problems.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24) – though LNG delivery remains tight against a backdrop of sustained high temperatures across Asia (and the associated cooling demand).

On the hedging side, we’re now on the other side of Summer-24 – with 114 days having elapsed, and 70 remaining.

Clients with open volumes for Winter-24 are increasingly scaling-in so as to avoid any loss of prevailing value.

Monthly Day-Ahead averages so far this month are on target to achieve 74p/therm (or circa. 2.5p/kwh excluding non-gas).

ELECTRICITY & CARBON

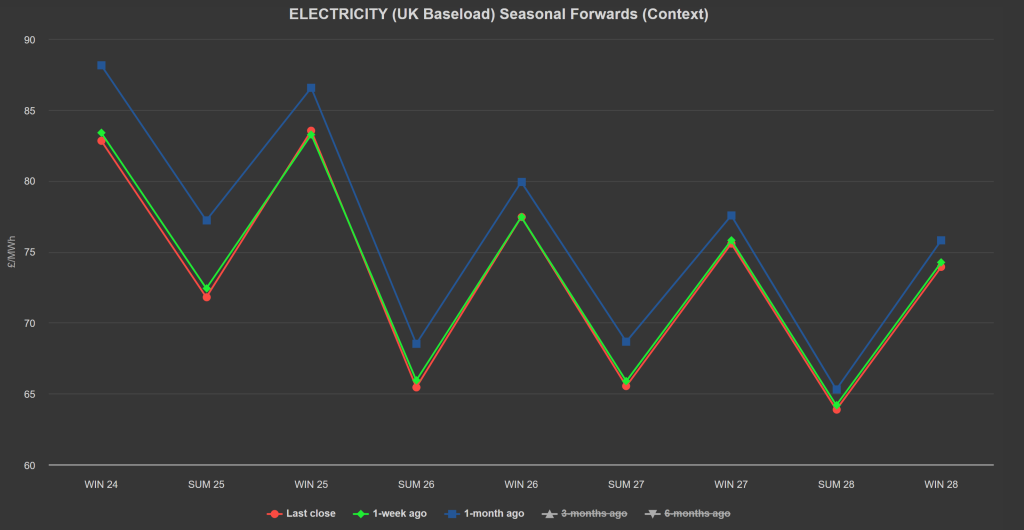

Seasonal Forwards are down on the month but almost unchanged on the week – reflecting last week’s very sideways price action! – see chart below and at https://icdenergymanagers.com/charts/

Looking to the continent, European near-term delivery prices started the week on a bearish note pressured by weaker gas and EUA (European Carbon) prices.

Fundamentally, key drivers are not supportive either – with no major heatwave forecasted in western Europe in the near future, comfortable hydro stocks in the Alps, and healthy French nuclear availability at the time of writing.

UKAs (UK Carbon Allowances) followed our prediction that prices were due to fall (as indicated by RSI divergence) – now trading at circa. £40.37/tn.

With Dec ’24 benchmark EUAs having broken temporarily below €65/tn yesterday, UKAs broke below £40/tn – though both have risen back up above these support levels this afternoon.

If gas prices continue to drift lower across Europe/UK, expect Carbon to do the same and for support levels to break with more conviction.

Our electricity generation mix is a little bullish in nature today with renewables contributing 26%, thermal at 35% (gas and coal) and low carbon at 26% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £68/mwh (or circa. 6.8p/kwh excluding non-energy).