Notably, Q125 is now offered over 120p/therm – thereafter, Summer-25 and Winter-25 quarters are offered over 100p/therm – very wintry Forward prices! (see chart below)

It is of course very likely that Summer-25/Winter-25 rates will improve significantly once Winter-24 is in the rearview mirror (come next Spring).

But, for now, value is deteriorating in the face of increased demand, colder forecasts and ongoing geopolitical turmoil (threatening supply security).

On the supply side, Australia’s Pluto LNG terminal went offline unexpectedly yesterday – the cause has yet to be confirmed.

Not surprisingly (given that Australian LNG provides for the Asian markets), this unscheduled outage has contributed to bullish momentum at the Prompt (near-term delivery) as LNG spot prices seek to balance value accordingly amid increased competion for fewer cargoes.

Looking at the wider economy, the consequences of Scott Bessent’s appointment as US Treasury Secretary were evident across markets yesterday.

His stated intention to reduce the US budget deficit to 3% of GDP has been widely welcomed by the bond market, with the 10-year treasury yield falling to 4.26% (i.e., reducing the cost of US borrowing).

Accordingly, the US dollar has pared back its gains of last week (reflecting an expectation that interest rates will not need to rise if bond yields are falling).

In other important macro-economic news, oil prices dropped off yesterday amid news that the US intends to increase domestic crude production (by 3mb/d).

In short, initial reactions to Scott Bessent’s appointment reflect that market participants believe he’ll bring moderation to Trump’s trade policy, particularly with regards tariff increases (which seem likely to be lower for China than was threatened on the campaign trail).

UK prices will likely remain at a premium versus Europe’s as the winter progresses – otherwise, we’ll be left high and dry where LNG arrivals are concerned.

This premium is always exacerbated by structural problems in the UK’s gas system resulting in high transmission costs and, of course, a lack of storage compared to Europe – meaning the UK needs to offer a much higher price to secure supply.

Monthly Day-Ahead averages so far this month are on target to achieve 109.967p/therm (or approx. 3.752p/kwh excluding non-gas).

ELECTRICITY & CARBON

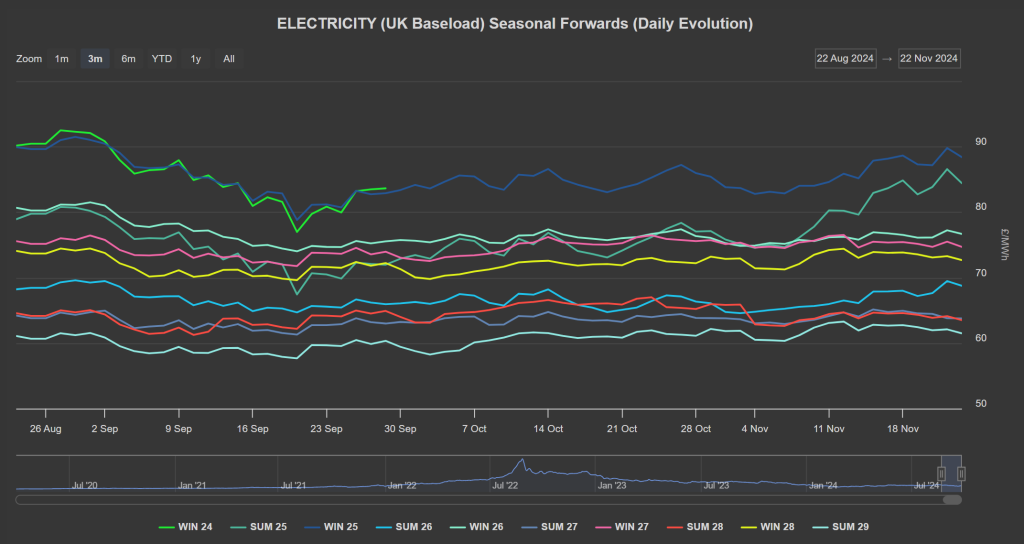

As further evidence that we’re in the wintry silly season, it’s worth noting that Winter-24 delivery prices closed at £83.64/mwh – but now both Summer-25 and Winter-25 delivery are being offered above that price!

Looking to the continent, EUAs (European Carbon) opened on a strong note yesterday off the back of surging gas prices in response to the news of possible sanctions on Gazprom (which would undoubtedly result in supply tightness).

The Dec’24 benchmark continued its uptrend, helped by the auction which cleared at €69.3/tn (on a 1:57 cover ratio) – in carbon markets, the cover ratio is a metric that measures the supply/demand dynamic (<1 reflects an oversupply; above 2 means bid volume is double available auction volume).

Prices then dropped off in late afternoon amid rumours that Israel and Lebanon were close to agreeing a ceasefire (mirroring oil prices).

UKAs (UK Carbon) remains technically bearish, despite Russia’s ICBM attack last week having instigated a significant bounce.

At the time of writing, UKAs are at £36.96/tn on the mid-price and look much heavier than their European counterpart – supply being less scarce (until 2027 when free allocations are likely to end).

The UK’s electricity generation mix is bullish in nature today with renewables contributing 30%, thermal at 42% (gas and coal) and low carbon at 14% (nuclear and imports).

Monthly Day-Ahead averages so far this month have fallen over the last few days and are on target to achieve £97.593/mwh (or 9.76p/kwh excluding non-energy).