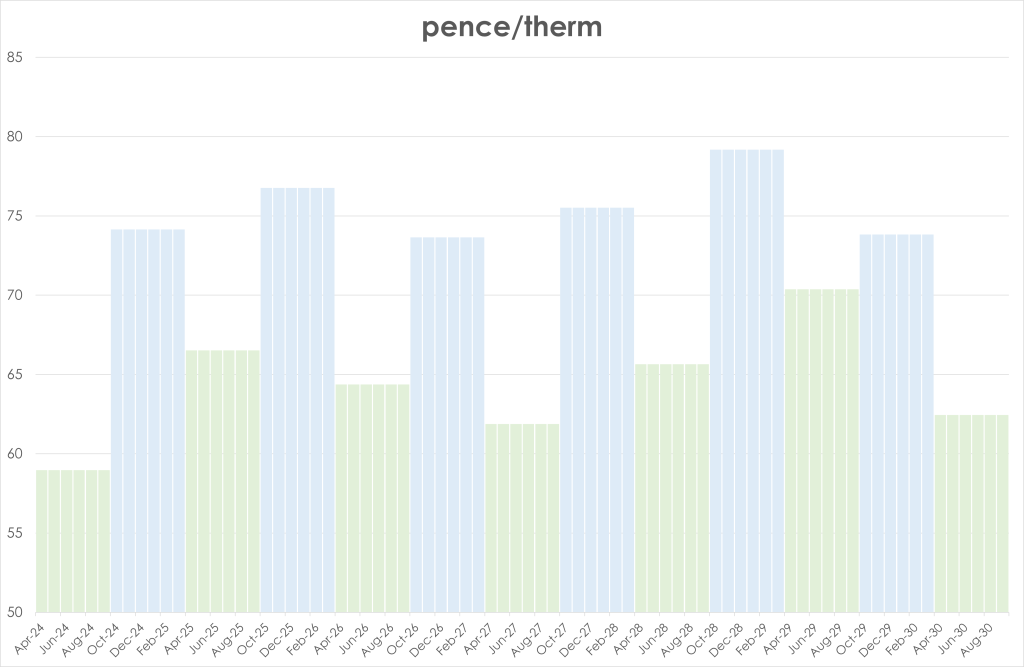

The UK gas curve is starting to resemble a Mongolian camel! (see chart)

Summer-24 delivery prices are at a 30% discount to Winter-24 delivery.

Clients are increasingly hedging the low seasons with a view to seeing how Summer-24 conditioning impacts on the high seasons.

Whilst markets have been backwardated for the last few years, the front seasons are now contango, then a mixed bag thereafter!

Market context remains overwhelmingly bearish.

Europe is still expected to end the winter with significant surplus still left in the tank (currently at 64% versus the 5-year average of 54%).

Across Europe, temperatures look set to warm-up and demand is likely to drop-off throughout the week.

In the UK, prices opened lower this morning despite a short system (demand outstripping supply).

At the time of writing, however, prices are marginally up off the back of lower temperatures, the associated higher heating demand and technical momentum indicators very much in oversold territory (meaning a retracement/correction may be in the offing whilst market participants take a breath).

In addition, increased storage withdrawals and forecasts of lower temperatures for early March are also lending support/limiting any further downside – at least in the short-term.

On the supply side, Qatar has announced plans to increase LNG production by 16 million tonnes per year (meaning a total annual capacity of 142 million tonnes).

The announcement came hot off the back of Biden’s decision to pause approvals for new US LNG export terminals citing environmental conerns (with the election looming).

With Summer-24 now 33 days away, surely only geo-political unrest poses any risk to a continuation of the prevailing long-term bear trend.

Monthly Day-Ahead averages are on target this month (so far) to achieve 64p/therm (or circa. 2.2p/kwh).

ELECTRICITY & CARBON ALLOWANCES

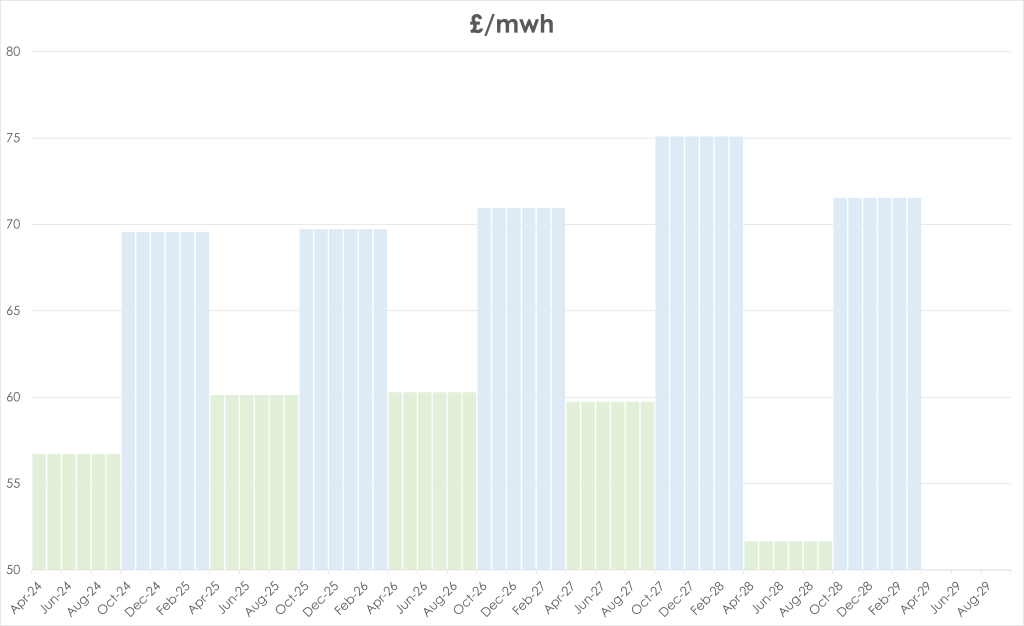

Compared to UK gas, UK electricity Seasonal Forwards are more orderly, with winters at least now very much in a contango state (future delivery prices higher than near term delivery prices) – see chart.

Summer-24 is at a 20% discount to Winter-24 prices.

Assessment prices for Summer-29 have dropped off the chart, printing at £49/mwh! (4.9p/kwh).

Looking to the continent, near-term delivery prices rose yesterday, buoyed by a drop in wind, lower temperatures and weak French nuclear availability against a backdrop of firmer fuels and emissions prices.

Down the curve, markets retraced from oversold conditions, with selling interest drying-up temporarily.

Forecasts of slightly lower wind output and temperatures for early-March supported the technical correction, but the fundamental picture remains overwhelmingly soft with a bleak demand outlook amid comfortable supply/demand dynamics.

On carbon markets, EUAs started the week with a noticeable 3.3% jump, likely triggered by some short-covering after 52 €/t proved strong support.

As allowances grow cheaper and more attractive for compliance (Industrial) players, it’s likely we’ll see some good buying interest at these low levels.

Most analysts have significantly revised downward their projections for carbon prices for 2024 over the past weeks, expecting a recovery at some point but seeing little reason for a renewed uptrend just yet due to the higher supply and lower demand anticipated in 2024.

UKAs finished the day at £35/tn for Dec-24 delivery.

Back in the UK, our generation mix bearish in nature with renewables contributing 44% and gas-for-power burn at 34%.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £59/mwh (or 5.9p/kwh).