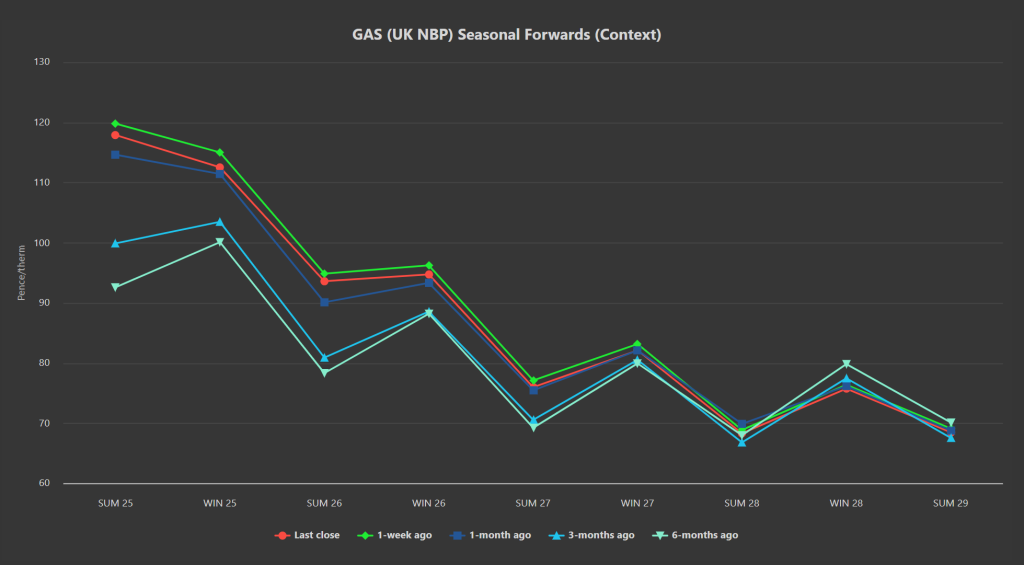

Whilst Day-Ahead remains at a premium to Month/Quarter-Ahead, Seasonal Forwards are down on the week but up on the month (please see chart below).

Comfortable LNG supply into Europe/the UK and stable Norwegian flows are keeping a lid on wintry bullish momentum – the UK system opened long today (supply outstripping demand forecast).

Asia’s prices remain at a discount to Europe’s, so cargoes from the US and Qatar continue to follow the money to our shores – easing the supply picture.

The actual send-out of LNG has been slowed by recent storms causing delays to unloading/degasification.

Despite the well-publicised end to the Russia/Ukraine transit deal, the European Commission has confirmed talks are ongoing with Ukraine – President Volodymyr Zelenskyis is apparently now considering a deal with Azerbaijan with a view to transiting through Ukraine to Slovakia.

On the weather side of things, the continent continues to enjoy temperatures above seasonal norms limiting heating demand – though we may see a colder spell for a few days heading into the weekend.

European storage fullness is now down to 56% versus the 5-year average of 58%, though withdrawals have slowed with the return of improved temperatures and renewables outputs.

Anomalously, Summer-25 delivery remains at a premium to Winter-25 reflecting fears over Europe’s ability to replenish inventories to the mandated target of 90% by 1st Nov ’25 (to ensure supply security in Winter-25).

Monthly Day-Ahead averages for this month so far are at 121.942p/therm (or approx. 4.161p/kwh excluding non-gas) – the average having remained consistently above 120p/therm for the whole month.

ELECTRICITY & CARBON

UKAs (UK Carbon Allowances) went to the moon this morning off the back of Keir Starmer’s suggestion in an FT article that he’s “looking to link the UK and EU emissions trading schemes” – please see chart below.

Of course, UKAs currently enjoy a significant discount versus EUAs, so not surprisingly, UKAs rocketed by as much as 13% on the mid-price to £40.91/tn, dropping back to close the session at £40.16/tn.

Ultimately, the bullish move was reactive, and no doubt linked to algorithmic traders and speculators jumping on a headline and spiking an illiquid market.

On reflection, there appears to be only limited substance to the story (citing reports that “the UK has requested that ETS linkage and CBAMs are included on the agenda for the spring summit, expected in March or April.”)

It would seem likely that prices will fall back once the headline fades, and fundamentals prevail (i.e., good supply, and free allocation not being reduced until 2027).

Today’s UK’s electricity generation mix has been neutral today with renewables contributing 31%, thermal at 34% (gas and coal) and low carbon at 20% (nuclear and imports).

Monthly Day-Ahead averages for this month so far are at £1118.116/mwh (or 11.81p/kwh excluding non-energy) – the average having fallen over the last week reflecting higher temperatures and improved wind outputs (limiting gas for power burn).