Bearish momentum persists amid comfortable fundamentals – ‘summery’ conditions, low demand, solid supply dynamics, subdued Asian demand, and optimism that Russian flows may return.

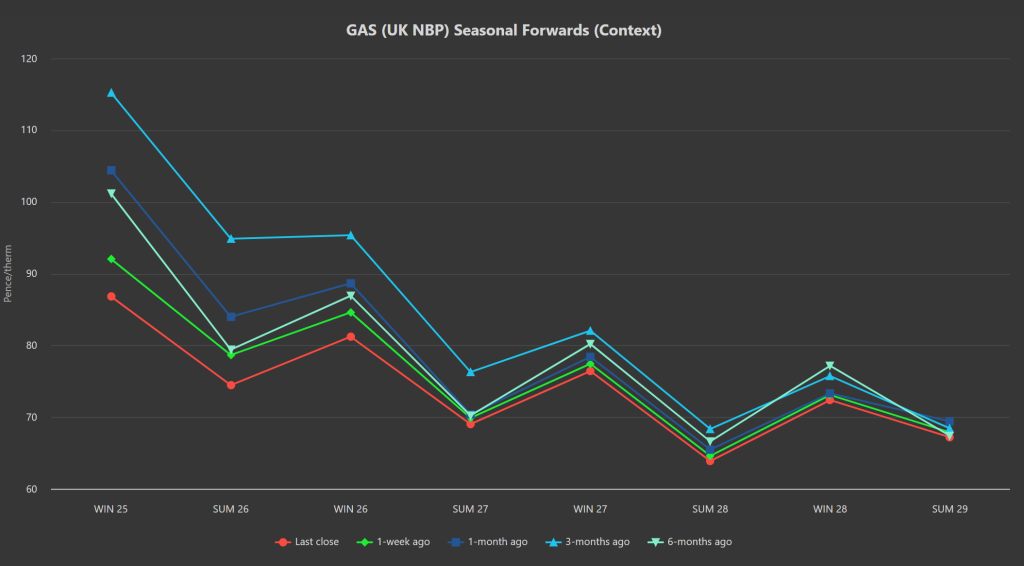

Seasonal Forwards are down all the way out to Summer-29 versus 1-week/1-month/3-months/6-months ago – please see chart below.

Near-term delivery prices (Day/Month/Quarter-Ahead) are down circa. 50% versus the most recent highs posted on 10th Feb ’25.

The doomsayers, opportunists, and bullish speculators have all gone very quiet about Europe not being able to replenish stocks in time for Winter-25.

European inventories continue to enjoy healthy injections with fullness now at 39% versus the 5-year average of 46%.

Notably, in light of the EU having loosened storage requirements for Winter-25, Bloomberg analysts have now revised storage predictions for Europe with fullness now forecasted to be at 88% by October – so well on track to hit even the old mandated number of 90% by 1st Nov.

Europe and the UK continue to enjoy the benefits of weakened Asian competition for LNG cargoes due to subdued Chinese demand.

China’s gas consumption is predicted to expand marginally in 2025 – though it’s worth pointing out that LNG represents its most expensive supply source.

For what it’s worth, we don’t agree with this prediction and believe instead that China’s gas consumption will fall y-o-y (assuming Trump’s tariffs hold steady).

Demand destruction is also forecast to increase across Europe as an impact of Trump’s tariff attack – so, of course, depressed demand will keep a lid on prices.

On the geopolitical side of things, Russia has announced another (very short) temporary ceasefire to coincide with their May public holiday – the move was welcomed by bears and a sell-off ensued yesterday afternoon.

Russian critics have pointed out that attacks seem to continue regardless during these short ceasefires, and suggest Putin is just playing for time.

Nonetheless, the Trump administration want it known that they’re still pushing for a full ceasefire (amid rumours that the long-touted minerals deal with Ukraine is close to completion).

Weather-wise, high temperatures abound and demand is below seasonal norms despite reduced flows out of Norway today (due to scheduled summer maintenance).

In short, summer is upon us, conditions are benign, and prices are falling – but how far will they fall, where is the bottom of this market?

Well, if Russia and the US reach a ‘peace’ deal, and by some miracle Russian gas flows resume, prices will drop off a cliff.

If China stays out of the LNG contest, European prices can afford to stay low.

So, without any further major developments, it’s fair to say that further downside is limited, for now.

As such, buyers are encouraged to scale-in modest hedges over the coming days/weeks whilst the going’s good.

Whilst markets may fall further, it’s worth remembering that current pices for Winter-25 (for example) are at a 66% discount versus the highs of Aug ’22 – so prevailing comparative value is undeniable!

This month’s UK gas Day-Ahead averages are drifting incrementally lower, now at 85p/therm (or approx. 2.9p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity markets remain closely correlated to gas movements.

Winter-25 is knocking on the door of £80/mwh (to the downside) – if this level breaks, all Seasons down the curve will be sub-£80/mwh.

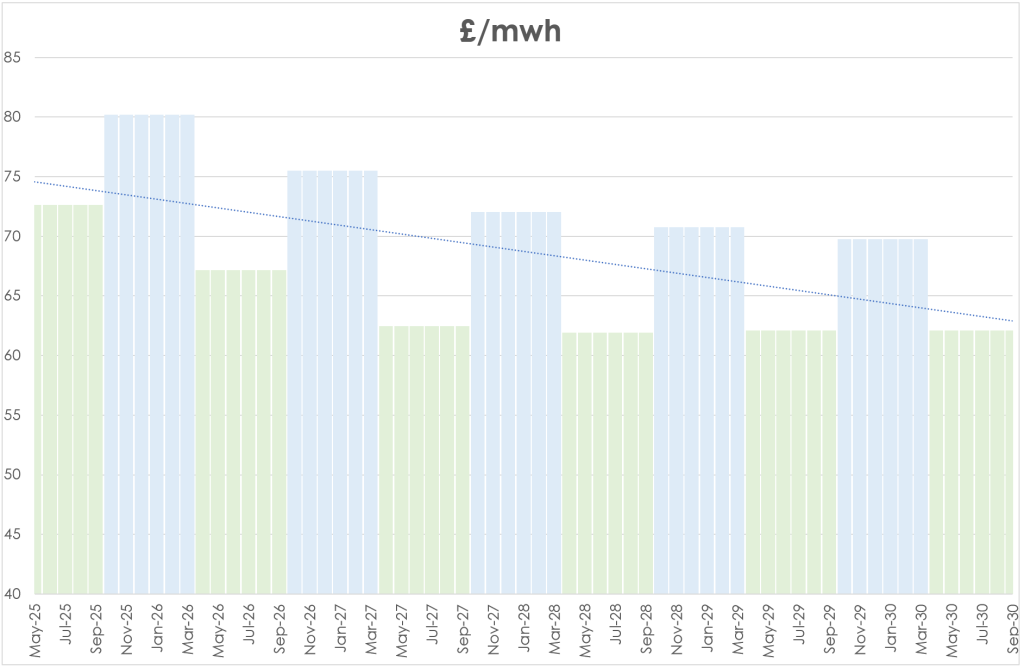

As further potential evidence that the market may be bottoming-out, it’s worth taking a look at Forward summer prices (S27/S28/S29/S30) – they’re all at basically the same price (reflecting an underlying sentiment that prevailing conditions don’t warrant a price below £60/mwh regardless of how far out the period of delivery may be) – please see chart below.

On the Carbon markets, UKAs reacted bullishly to Trump’s climb-down on reciprocal tariffs (with investment speculators still net long and emissions increasingly developing a correlation with equities).

Right now, Dec-24 UKAs are back up at £47.50/tn having broken above the upper extremity of a long term bearish trend channel – with confirmed (and holding) resistance at £48.80/tn.

However, as has been the case since the current rangebound trading began (back in early Feb’25), momentum indicators are divergent and reflective of trends with little conviction either way.

Today’s UK electricity generation mix is neutral in nature, with renewables contributing 36%, thermal at 26% (gas and coal) and low carbon at 20% (nuclear and imports).

So far this month, electricity Day-Ahead averages are holding steady at £79/mwh (or approx. 7.9p/kwh excluding non-energy).