We’re now well into Winter-24, and front-end periods of delivery are starting to reflect the impacts of cold, low wind conditions.

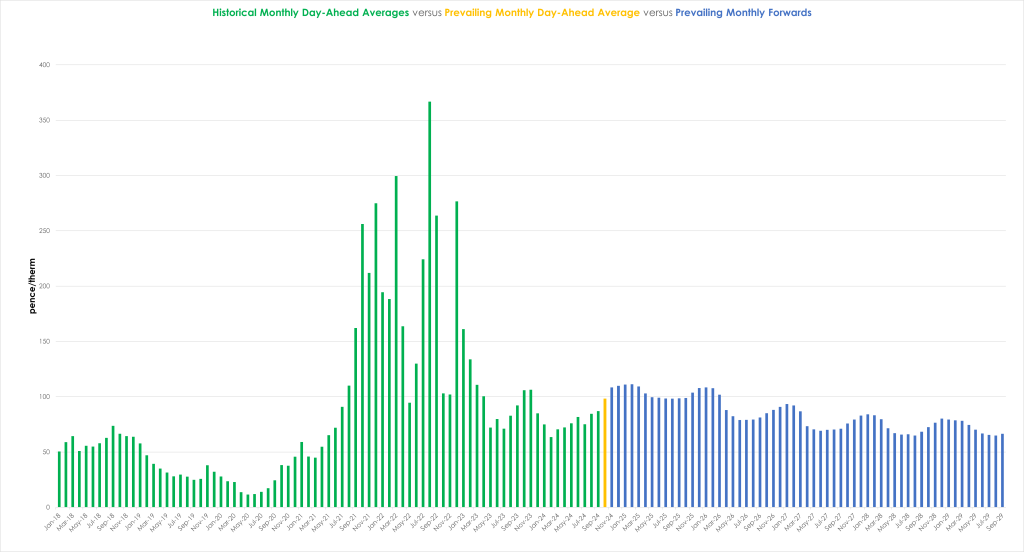

Whilst Monthly Forward prices (shown as blue bars in the chart below) are way below the highs printed in ’21 to ’23, it’s worth noting that, with the front-end lifting higher this last couple of weeks, prices at the back of the curve are circa. 40% discounted versus the coming winter months.

It’s also reflective of winter conditions that Day-Ahead is now at a premium to Season/Ahead and Year-Ahead (but discounted versus Month-Ahead/Quarter-Ahead).

Yesterday saw a volatile day of trading resulting in higher front-end prices.

Whilst Israel made good on its threats to retaliate, Iran has been muted in their response – which is taking some of the heat out of worries over supply security across the Middle East.

It’s helped no doubt that Israel opted to attack military targets as opposed to oil/gas infrastructure – accordingly, the oil markets saw a decent drop off yesterday.

The UK system was only marginally short at this morning’s open (demand forecast outstripping supply) – but it’s worth noting that demand remains below seasonal norms due to seasonally benign weather conditions.

As per expectations, the higher UK gas prices (Day-Ahead being at a premium to European benchmark spot gas prices) is beginning to encourage a few more LNG cargos in our direction – with 3 arrivals expected in the next fortnight.

Nonetheless, the lion’s share of global LNG is still headed to Asia where demand and high prices persist.

Thankfully, bullish fervour is being tempered by a de-escalation in Middle East tensions (for now) which lowers some supply uncertainty amid European storage levels at 96% fullness versus the 5-year average of 90%.

Monthly Day-Ahead averages so far this month are on target to achieve 98.323p/therm (or approx. 3.355p/kwh excluding non-gas).

ELECTRICITY & CARBON

On the carbon markets, UKAs remain in a longer term downtrend but have spent the last fortnight rangebound between £38 to £40/tn.

Prices look set to rest upside areas of resistance having broken below the internal bullish trend channel that was in play between 8th to 25th Oct (see chart below).

Looking down the electricity curve, FLEX buyers are eyeing up the comparative value on offer with Summer-30 at a 40% discount versus the balance of Winter-24!

Our electricity generation mix is bullish in nature today with renewables contributing 20%, thermal at 49% (gas and coal) and low carbon at 19% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £83.858/mwh (or approx. 8.3858p/kwh excluding non-energy).