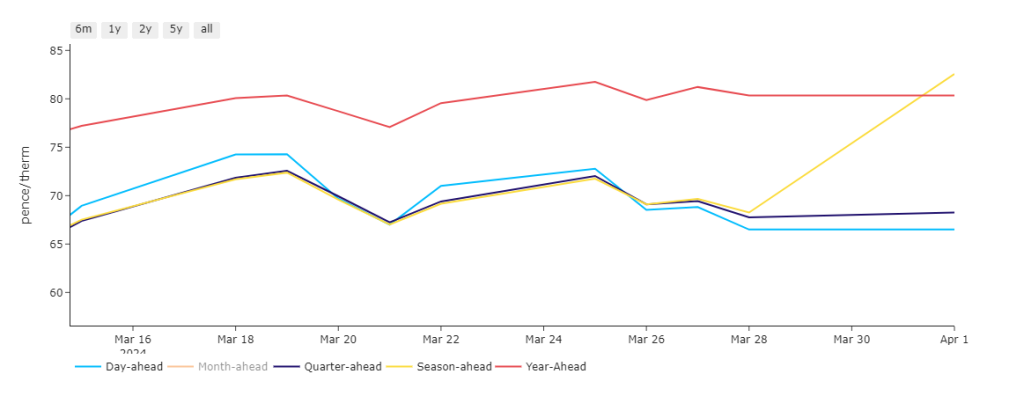

Summer-24 is upon us (beginning 1st April) – the Season-Ahead product is of course now Winter-24 (see chart).

Day-Ahead prices sit at a comfortable discount to Quarter-Ahead.

BOS-24 (Balance of Summer-24) prices are at parity with Day-Ahead.

All in all, prices have found equilibrium with 6-months of summer conditioning stretched out before us.

European storage closed out Winter-23 with 60% still left in the tank – so, not much to do over the coming months to replenish inventories (hopefully!)

UK temperatures are forecast to rise for the first half of April with the first weekend of the new season expected to sit a few degrees above seasonal norms.

Wind outputs are also forecast to generate at levels above seasonal norms until the middle of next week.

Norwegian flows are strong and steady with limited outages.

As you’d expect, given the favourable supply supply/demand dynamic, the UK system opened long this morning against a backdrop of above seasonal average temperatures and the associated low heating requirement.

Notably, LNG imports into Europe have fallen to their lowest level since 2021 – imports were down over 40% w-o-w.

Lower demand across domestic/Industrials coupled with higher Asian demand are driving the fall of LNG arriving at European/UK ports – though it’s worth pointing out that Asian countries (China and India primarily) will not continue to increase their LNG imports if gas prices increase too much, because they’re able to resort to cheaper alternatives – coal in particular.

Back in the UK, it’s sideways price-action so far today.

Monthly Day-Ahead averages achieved 64p/therm (or circa. 2.2p/kwh) for March-24.

ELECTRICITY

Looking to the continent, near-term delivery prices are pressured by forecasts of particularly strong renewables outputs this week.

Down the curve, prices look pressured by a significantly warmer and windier revision of weather forecasts for the coming days.

Delivery contracts for the coming weekend are already trading below 15€/MWh in France and Germany – so we may see very low Day-Ahead prices print in the next couple of weeks.

Not a lot else to report at this stage, our electricity generation mix is neutral in nature this afternoon with renewables contributing 29%, thermal at 31% (gas and coal) and low carbon at 24% (nuclear and imports).

Monthly Day-Ahead averages achieved £62/mwh (or circa. 6.2p/kwh) for March-24.