Prompt (near-term) delivery prices dropped off yesterday off the back of a loose balance (solid supply, weak demand).

Key fundamental drivers remain unchanged and the picture remains neutral to bearish.

Steady Norwegian flows coupled with 3-5mcm/d of Barron North coming back on line (notwithstanding the extended outage) is keeping a lid on any upside.

It’s worth noting however that any extension to the ongoing Teesside outages poses a marginal bullish risk.

Though were this to happen, we’d still be able to inject reduced volumes into storage whilst continuing to export to the Continent (via the Interconnector).

Temperatures have fallen to start the week and are keeping demand levels above forecast (due to an unexpected rise in heating demand).

The UK system opened marginally short this morning (demand outstripping supply) so prices got an early bullish nudge – though it’s small potatoes (barely altered versus yesterday’s close).

LNG prices could be subject to volatility by the weekend with the onset of tropical storms – Hurricane Beryl is heading toward Jamaica and looking set to make landfall at Category 4.

Terminals throughout the region (e.g. New Fortress LNG in Montego Bay) will likely be impacted by sustained disruption.

Cyclones along the Gulf Coast also pose a risk to US LNG exports.

Competition for LNG continues to be exacerbated by high temperatures across Asia (LNG needed for gas-for-power generation to sustain cooling demand).

Optimistic consensus is building across the energy industry that by the end of the decade, there’ll be more than a 10% surfeit of global LNG supply given all the production projects now underway (and of course the forecasted move away from fossil fuels in favour of cleaner renewables).

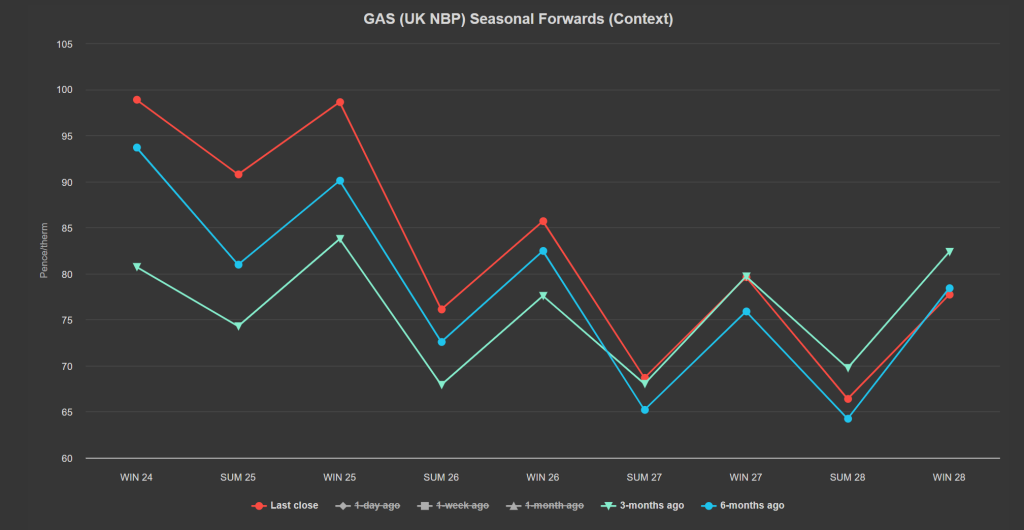

Seasonal Forwards remain stubbornly above those printed 3-months/6 months-ago (see chart).

Whilst prices fell circa. 50% between Dec ’23 to Feb ’24, they’ve since risen circa. 25% then meandered sideways since mid-May ’24.

Considering prevailing supportive drivers (primarily geopolitical disquiet and fears of supply tightness) it increasingly looks as though even warmer weather may not be enough to take the market lower in the coming weeks.

We’re 93 days into Summer-24 with the onset of Winter-24 now 91 days ahead.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24) – though LNG delivery remains tight against a backdrop of sustained high temperatures across Asia.

Monthly Day-Ahead averages for Jun ’24 achieved 82p/therm (or circa. 2.8p/kwh excluding non-gas).

Monthly Day-Ahead averages so far this month are on target to achieve 79p/therm (or circa. 2.7p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European prompt (near-term) delivery prices were marginally down yesterday.

In the main, temperatures will remain significantly below seasonal long-term averages for the days to come until this weekend.

Wind generation is strong, solar generation is limited due to unsettled conditions.

On the Carbon markets, the EUA Dec ’24 benchmark closed Monday’s session with a slight gain at €68.05/tonne.

Back in the UK, UKAs (UK Carbon Allowances) followed our prediction that prices were due to fall as indicated by RSI divergence – now trading at circa. £47/tonne.

Prices are now in a confirmed ascending trend channel testing the mid-line – congestion is building at £40/tn as a strong area of support – so a retest of this level will likely result in a bounce.

Our electricity generation mix is slightly bearish in nature today with renewables contributing 38%, thermal at 21% (gas and coal) and low carbon at 26% (nuclear and imports).

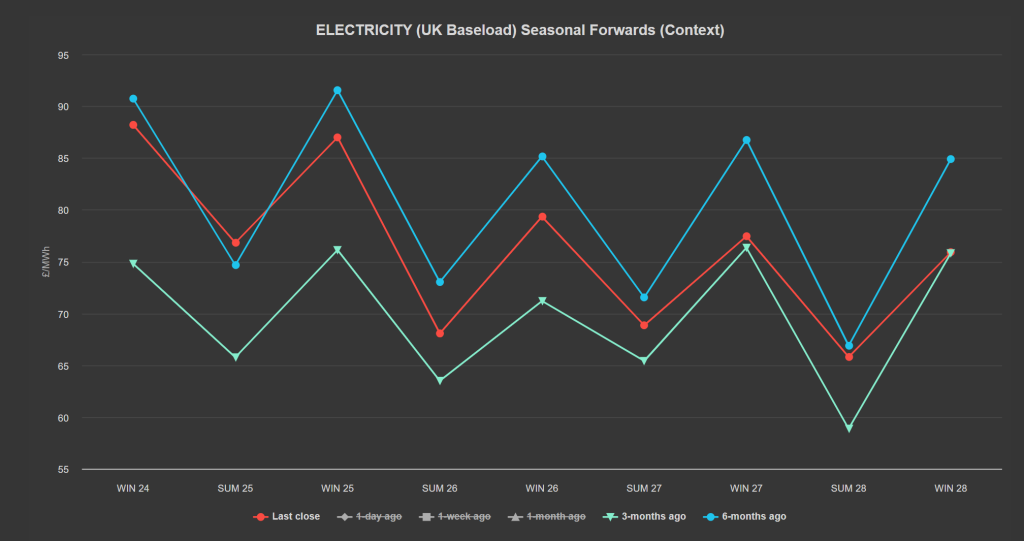

Seasonal Forwards remain stubbornly above those printed 3-months, but mostly below those printed 6 months-ago (see chart).

Monthly Day-Ahead averages for Jun ’24 achieved £71/mwh (or circa. 7.1p/kwh excluding non-energy).

Monthly Day-Ahead averages so far this month are on target to achieve £78/mwh (or circa. 7.8p/kwh excluding non-energy).