Despite temperatures rising as the week progresses (and demand falling), prices were marginally higher at this morning’s open – most likely off the back of renewed buying interest given recent drops in price.

Forecast demand into next week is slightly higher based on temperature drops below seasonal norms.

Feedgas into Freeport LNG (Texas) is gradually ramping up with Train 1 back online – offering a welcome boost to European LNG supplies (Train 2 has also been restarted – so just Train 3 remains offline).

As such, it’s likely the plant’s flows will rise steeply and and back to levels not seen for the last few weeks.

Norwegian flows into Europe/UK remain disrupted (and below the 5-day moving average) with major plants still subject to maintenance.

Nonetheless, European MRS (storage fullness) remains at historical highs – 62% versus the 5-year average of 46%.

There are only two LNG arrivals expected into UK ports to degasify at South Hook in the next two weeks (with “Energy Pacific” expected tomorrow from America).

Geopolitically, there’s very little noise out of the Middle East – be it news of escalation or peace negotiations – as such, risk of another flare up will continue to offer price support.

All in all, a mixed bag – hence the sideways price action.

Monthly Day-Ahead averages for April achieved 72p/therm (or 2.45p/kwh).

ELECTRICITY & CARBON

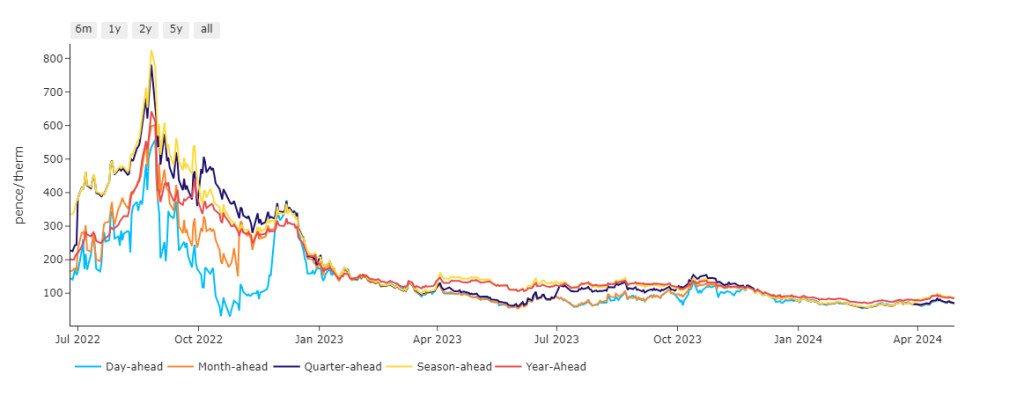

As you’d expect with the onset of summer conditioning, both Season-Ahead and 2-Seasons-Ahead are very gradually dropping off in-line with seasonal demand (see chart).

Looking to the continent, near-term delivery prices are softening due to warmer weather conditions.

Those warm conditions should persist over Europe, leading to lower power demand, while both wind and solar generation are expected to ramp up.

Another bearish driver is the decline in coal prices (reducing the cost of thermal generation) – API2 is now trading below $110/tn (Rotterdam Futures).

Higher temperatures across Europe should continue to pressure the fuel basket but news on the gas market and possible bottlenecks in the supply outlook still lend lingering support – despite the onset of summer conditioning.

On Carbon markets, the benchmark EUAs (European EU-ETS) Dec-24 benchmark contracts fell yesterday and broke below the 20-day moving average support level.

Holding or losing this support will be key over the coming days.

The fundamental picture remains bearish: low emissions from thermal power generators and lower production expected from energy-intensive industrials throughout May.

Back in the UK, Dec-24 contracts for UK ETS are circa. £35/tn.

Our electricity generation mix is very bearish in nature today with renewables contributing 56%, thermal at 7% (gas and coal) and low carbon at 27% (nuclear and imports).

Monthly Day-Ahead averages for April achieved £52/mwh (or 5.2p/kwh).