Today marks the last day of Russian gas flow transiting via Ukraine into Europe with Kyiv refusing to negotiate a new deal

Gazprom has now confirmed it will only pump reduced volumes today, bringing to a close a transit deal that had survived nearly three years of conflict.

Monetarily, Ukraine is giving up some $800 million a year in fees from Russia, whilst Gazprom will lose close to $5 billion in gas sales to Europe (via Ukraine).

Russia (and the Soviet Union) spent the best part of 50 years winning the lion’s share of the European gas market – which at its height stood at 35%.

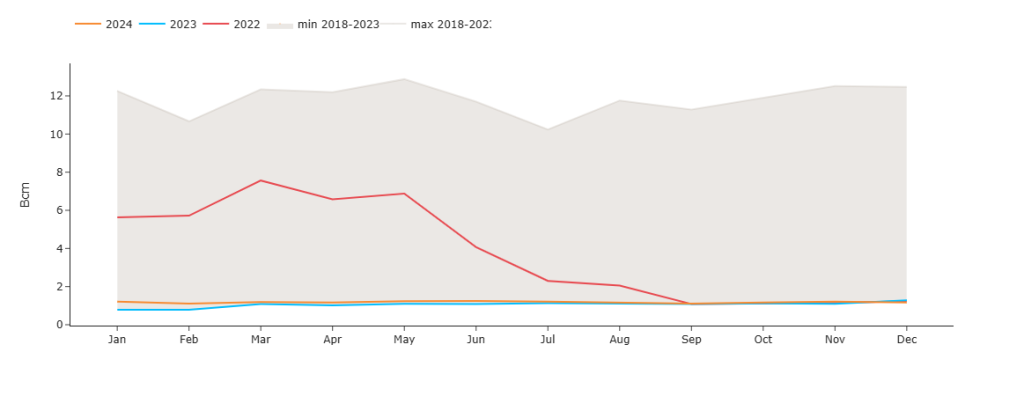

At the time of writing, most Russian gas routes to Europe have been halted, including Yamal-Europe via Belarus and Nord Stream under the Baltic (that was blown up under mysterious circumstances back in 2022) – please see chart below detailing Russian gas exports into Western Europe (via Velke/Nordstream/Yamal).

Other than Russian LNG, the end of the transit deal means Putin’s hold over Europe’s gas market is effectively no more – though prevailing inflated prices are evidence of the impact of the loss of Russia’s flows.

Slovakia, the Czech Republic, and Austria have negotiated replacement supplies – as such analyst consensus (noise aside) is that market impact should be minimal heading into the New Year.

Anticipation of the ending agreement (coupled with forecasts of lower temperatures for the start of ’25) has pushed near-term and front Season delivery prices higher over the Christmas break amid low volume/high volatility

So, what now?

Well, Russia’s exit undoubtedly has significant geopolitical ramifications.

Whereas Moscow has lost its dominant share of gas supplies to Europe (state-controlled Gazprom recorded a $7 billion loss in 2023 alone, its first annual loss since 1999), rivals such as the United States, Qatar and Norway have inevitably benefitted from increased revenues.

For Europe as a whole, the loss of comparatively inexpensive Russian gas supplies has contributed to an economic slowdown, demand destruction, higher inflation, and an associated cost-of-living problem.

Traders will return to their desks next week – let’s see how the market deals with key drivers once volume returns to the market.

As things stand, European storage is at 74%, in the middle of the 8-year range.

Today’s UK’s electricity generation mix is bearish (and price pressuring) in nature with renewables contributing 62%, thermal at 13% (gas and coal) and low carbon at 17% (nuclear and imports).